Assessing the Impact of Monthly Fuel Price Review/Adjustment on Transporters as (Human Resource). A Case of Ndola Transporters

1Quintino Chembo, *2Dr. Saili Mathews, 3Dr. Sikalumbi Dewin

1phd Student – CHAU 2UNZA 3CHAU

Assessing the impact of monthly fuel price review/adjustment on transporters (Human Resource). Since the removal of subsidies from fuel, it has been increased 45 time and reduced only 3 times from 2022 to 2025. Transport system is the corner stone of every nation, the main modes of transport in Zambia are road, rail, air, and inland waterways. The machines which drive this system need fuel which is reviewed every month in terms of price. In the past, about 60% of petroleum products used in Zambia were produced by INDENI while 40% imported by road. Recently the company is not working and petroleum procured are now brought in by road which is the most expensive undertaking and also significantly reduces the lifespan of our roads.

Economic theory is used here, which states that the price for a specific good or service is determined by the relationship between its supply and demand at any given point (Adam Hayes 2024). From this theory that the hypothesis was developed as “Monthly fuel price adjustment does not cause increase in price of goods and does not impact on transporters (human resource) negatively.” It was discovered that it was a two-way thing that is, it can increase or reduce the financial capacity of the transporter depending on the situation. Figure B has shown that monthly fuel adjustment has an impact on transporters and the economy as a whole and chai square has rejected the null hypothesis. It is recommended that players must be given room for long term financial planning and that cheap source of fuel must be considered as they look at the pride of the tanker drivers in terms of allowances. Finally, but not the least the second refinery company must be constructed to reduce on the expenses incurred and improve the performance of the economy.

Key Words: Call Boy, Fuel supply chain, Idiosyncratic, Inflation rate, Pro-cyclical, Subsidies

Transport system is the corner stone of every nation, the main modes of transport in Zambia are rail, road, air, and inland waterways for this transport to be effective and in motion. The machines which drive this system need fuel which is reviewed every month in Zambia today. (Teed, 2015). This chapter will cover background, statement problem, objective, research questions.

The monthly review of domestic fuel prices means that domestic prices of petroleum products will heavily rely on the performance of international oil prices and the kwacha-dollar exchange rate which are highly volatile. Adopting a 30-day pricing cycle strategy by ERB entails difficulties in manufacturers’ planning decisions as domestic prices of petroleum products will be expected to follow the trend of international oil prices and the performance of the Kwacha against the US dollar. Prices will rise whenever a rise is recorded either in the international oil prices or when the Kwacha loses value against the US dollar. Likewise, domestic fuel prices will decline whenever international oil prices reduce or when the Kwacha gains value against the US dollar. Without prediction models, manufacturers will have to rely highly on ERB. (Janic, M., 2015).

Subjecting the transport sector to such an unpredictable policy adds inconvenience to the already existing inconsistencies. The transport sector has been grappling with supply chain disruptions triggered by the Covid-19 pandemic, where crude oil would move between a month and three months from the time of order to delivery. Furthermore, at INDEN electricity disruptions are usually unannounced and without schedule thus increasing down times for production together with hug expenditure and high cost of doing business has crippled the company leaving the responsibility in the hands of the private and public transporters. Additionally, consistent fluctuations in the depreciation of the Kwacha have made it difficult for transporters to effectively operate. (Forkenbrock, D. J., 2001: Patton 2024).

Post the August 2021 elections, the government embarked on sectoral economic reforms aimed at rebuilding the economy. Key reforms in the energy sector involved the removal of some fuel subsidies, placing of INDENI refinery on care and maintenance, and much more recently, the introduction of monthly reviews for setting pump prices of fuel whose pros and cons have been up for debate, especially when the resulting adjustment is upwards. (Hsu, and Tsai,2012). The overarching question is: are these monthly reviews inherently problematic? In our view, monthly reviews are neither the problem nor the solution, but necessary to get us close to an efficient energy market. Although Zambia has relied on anchored expectations to model gas prices in the past, nothing empirically stops us from trying out unmoored expectations something which the monthly reviews get us close to. It may take some time for us to get used to this and yet, that’s the efficient thing to do (World Bank, 2018).

Given an unstable currency like the Zambian Kwacha and volatility in the international oil prices which might exacerbate on account of the invasion of Ukraine on Russia, international fuel prices are likely to rise further, and regular fluctuations of higher domestic fuel pump prices should be anticipated. Consequently, other companies like manufacturing has faced with a problem of knowing how big a cost they should attach to fuel in the medium to long term, as fuel remains a key resource in the production process. With a rise in domestic fuel prices, increases in the cost of transportation of raw materials as well as distribution of final products for transporters will be likely and ultimately push the cost of production even further for all other companies which uses patrol, oil, diesels etc. for their operations. (Oum, T. H., A 2016).

In the recent past, despite observing a rise in cost of fuel early this year 2024, transporters tried to maintain running cost at competitive on the market as the result the price of the petroleum products was increased. This can be seen from the slower rise in prices or a reducing inflation rate which has been on a downward trend since August 2021. Fuel also drove total food inflation (60% of) unlike non-food inflation which has been seen to have risen in some periods. In January 2022, food inflation dropped to 16.9% from 19.9% which was recorded in December 2021 while non-food inflation rose to 12.7% from 12.1% in the same period. (Bulletin 2024) Increasing prices of fuel would have made local manufacturers increase prices of products and lose out on customers as it would have made domestic products expensive relative to imported products from the region.

Background of the Study

According to (McCann, P., 2002) Zambia’s total petroleum requirements are met through imports because the country does not have any proven reserves of crude oil. The petroleum industry in Zambia is made up of TAZAMA Pipelines Ltd, which is owned, by the Governments of Zambia and Tanzania, INDENI Refinery, Ndola Fuel Terminal, Bulk fuel storage depots and the Oil Marketing Companies (OMCs). The major activities that take place in the petroleum sector are; procurement, transportation, refining, distribution and supply petroleum products to various customers at a reasonable cost. Zambia imports a mixed petroleum feedstock consisting of crude oil, naphtha and diesel from the Middle East. This petroleum feedstock is processed at INDENI Petroleum Refinery and sold to OMCs as finished petroleum products. (Zambia Statistical Agency. 2022). On behalf of the OMCs, transporters distribute the petroleum products mainly by road to the service stations and commercial customers and Evaluation Division (2015) Policy Monitoring and Research Centre (PMRC).

A transport system is one of the components of urban and rural development which does not operate in the vacuum but it incorporates the drivers who are human resource, economic, social and environmental needs of society the tools which are available to the public to foster development. Urban and rural development and Public transport are two processes that influence each other and therefore they must be coordinated as both answer to the needs of humankind and affects economic activities both positively and negatively. It is through transportation that that fuel can be brought into the country and the price is not really determined by distance or the cost but the price of the fuel at the world market. (Cervero, 2013).

In Zambia, railways are not leading transportation mode for goods on the international and local routes. Total length of Zambian railway network is more than 2922 kilometers. 900 kilometers out of these are main lines while the rest of the network is branch line railway. Zambia Railways is the main railway line owned by government whereas the Tazania Zambia Railways (TAZARA) is owned by two governments and it is the largest consumer of petroleum products on the market of Zambia. The bus service runs seven days a week, with an hourly bus departure from either end (Livingstone, Lusaka and Kitwe). Minibuses are the common means of transport within the city. The minibuses have their main stage at City Market. Every mini-bus has a ‘Call Boy’ to attract passengers to the vehicles. This is another sector which consumes a lot of fuel from the oil petroleum companies. Being the biggest transport of passengers from one town to another on the hourly basis they badly get affected with the change in price of the fuel. (Noordin, N. S. 2019)

Internal fuel market is economically efficient if it fully internalizes new innovations which affect supply and/or demand. Supply which talks about the companies that produce the commodity while the demand side talks about the need of fuel in the county. In fact, the ‘first-best’ choice is given by a free market without intervention. (Hwang, & Ouyang, 2014). However, owing to the significance of energy prices for inflation outcomes and the political dynamics surrounding the sector, implementing a free-market equilibrium in the energy sector is evidently far-fetched. Sometimes, politically sensible decisions dictate market intervention to keep prices artificially low which, unfortunately, but often, is at odds with basic economic efficiency principles. (Ivy 2019)

Tracks are the major transporter of many products on the land including crude oil which is transported from Tanzania Dar-es-Salaam to Zambia, Ndola. Upon docked at INDENI where large storage tanks are then they start injecting it in the Distillation column which separate crude oil into various components including petrel, paraffin, deiseal and bituminous. Therefore, change in price will directly affect the performance of all these players the author has mentioned.

Taxes are also part of the transport system which are owned either privately or publicly they play significant role in helping to boost the economic activities of the country. Despite this importance all these tax use fuel which is reviewed every month end. Noordin, N. S (2019)

Petroleum is wholly imported and subject to ever increasing international prices and uncertain supply. To promote the participation of Zambians in the Petroleum Industry the country need to ensuring that Zambians hold shares in Oil Marketing Companies (OMCs) and given priority to participate in all stages of supply, transportation, storage and distribution. Initially Zambia relayed on Tazama pipe line for channeling fuel into Zambia and Indeni petroleum refinery tanks for storage of crude fuel and also for separation into different components of crude fuel to mention but a few some bye products are bitumen, diesel, Paraffin, Patrol and light gases. (Jong, et-al 2017).

Statement Problem

Many transporters (Drivers) depend on fuel to propel their machine in order for them to make up the necessary trips for the day, week, month and subsequently a year. Although Zambia has relied on anchored expectations to model gas prices in the past, nothing empirically stops government from trying out unmoored expectations – something which the monthly reviews get us close to. It may take some time for transporters to get used to this and yet, that is the efficient thing to do or most inefficient way of revamping the economy. After 2021 elections, the government embarked on sectoral economic reforms aimed at rebuilding the economy. Key reforms in the energy sector involved the removal of some fuel subsidies, placing of INDENI refinery on care and maintenance Previously fuel was heavily subsidized, today fuel price is reviewed every month end unfortunately this has brought about anxiety in the mind of the transporters especially bus drivers who make losses in their business when the price of the commodity goes up, their fair remains static. This same situation has put a number of transporters out of business and much more recently, the introduction of monthly reviews for setting pump prices of fuel whose pros and cons have been up for debate, especially when the resulting adjustment is upwards. Are these monthly reviews inherently problematic? In our view, monthly reviews are neither the problem nor the solution.

General objective

To assess the impact of monthly fuel price review/adjustment on transporters.

Specific objective

Research question

This chapter will cover both empirical and theoretical evidence. According to (Maxwell et-al 2015) it is worthwhile to examine if an empirical synthesis would lead to any new conclusions. Fuel is pivotal in the successful running of any business and especially in the transport industry like the airline industry, which is involved in massive transporting activities. There is no reasonable doubt therefore that high fuel costs have an adverse impact on the running of any organization. Thus, researchers conducted a meta-analysis of the empirical evidence on the impact of monthly price review on the transporters in Ndola Zambia.

Local Perspective

A market is economically efficient if it fully internalizes new innovations which affect supply and/or demand. In fact, the ‘first-best’ choice is given by a free market without intervention. However, owing to the significance of energy prices for inflation outcomes and the political dynamics surrounding the sector, implementing a free-market equilibrium in the energy sector is evidently far-fetched. Sometimes, politically sensible decisions dictate market intervention to keep prices artificially low which, unfortunately, but often, is at odds with basic economic efficiency principles. (World Bank, 2017).

As often in economics, we have a ‘second-best’ choice to fall back on. In this case, this is where the government intervenes to set the price but does so at a frequency that is underpinned by the frequency of shocks in the market. For a petroleum importing economy like Zambia, energy prices are expected to be pro-cyclical to exchange rate volatility overtime. The frequency of these exchange rate cycles (which depend mainly on the strength of the Kwacha) can be as high as daily. This alone, requires a high frequency of price reviews for the energy market to efficiently internalize new information from the FOREX market. (Janic, M., 2015).

On the flipside, the downside implication of monthly reviews has to do with increasing uncertainty not only in the energy market but in other markets which rely on energy as an input into production. This is bad for business and may negatively impact on production plans. However, one of the biggest challenges facing Zambia’s energy sector which also further necessitates high frequency price reviews is inadequate storage infrastructure. Most of our provincial depots are exclusively utilized as operational depots leaving us with no room to procure adequate strategic petroleum reserves. This makes us vulnerable to all shocks whether aggregate or idiosyncratic to the energy sector even when such shocks could be temporal. This also applies at individual level, consumers without the ability to buy in bulk will likely be more vulnerable even to temporary shocks.

In our view, these are the real factors that we should focus on to keep petroleum prices in check. We should prioritize capital investment towards infrastructure to ensure that; much of our petroleum imports are transported through TAZAMA and feedstock is efficiently refined at INDENI, and we have enough storage capacity for strategic reserves. Efforts to strengthen and stabilize the Kwacha should also take prominence. These factors matter more for stability of energy prices than the frequency of price reviews. (Russell, et-al 2014).

In the Zambian context, downstream and upstream, refers to the point of purchase of the crude in the Middle East to the refinery in Ndola while downstream refer all industries that start from the refinery to the service station. (Mwange, A., & Meyiwa, A. 2022).

The purpose of this article is to specifically discuss how monthly pricing of fuel in Zambia is conducted by the Energy Regulation Board (ERB) and the objective is to allow the reader to understand the guiding principles that affect pricing so that any future price adjustments are clearly put into perspective and analysed objectively. Situational Analysis Zambia’s average daily consumption in litres is as follows: Petrol (1,006,000 litres), Diesel (2,204,000 litres) and Kerosene (42,000 litres). Zambia does not have any known confirmed reserves of crude oil and therefore imports all its fuel requirements. (Salomey et al. 2013)

The importation of crude oil is done in two modes: through the 1,706 km long TAZAMA Pipeline from the port of Dar-es-Salaam in Tanzania to Ndola for refining at INDENI Refinery Limited and; importation of finished petroleum products by road and/rail. The composition of the crude oil or petroleum feedstock that is imported is adapted to meet the configuration of the Refinery and is best suited to meet the requirements of the market. (Salomey et al. 2013)

Prior to this, in 1998, setting of prices was done through the Government owned Zambia National Oil Company (ZNOC). After 1998, ERB took over the pricing function and (in 1999) introduced price caps on petroleum products. (Salomey et al. 2013)

This model of pricing was used until 2001 when Government liberalised pump prices. In 2004, ERB started using the Import Parity Pricing (IPP) model for pricing until 2008. The ERB migrated from IPP model because it required frequent changes to the prices of fuel on the market.

Use of the IPP methodology presented challenges in forecasting and budgeting of fuel prices for business entities and the general public. In response to this and in order to promote price stability on the market, in the near future, the ERB adopted the CPM for pricing of petroleum products. This is the model being used to date. Determinants of fuel prices. The domestic prices of petroleum products are mainly affected by international oil prices and the exchange rate of the United States dollar to the Zambian Kwacha. Zambia imports a commingled feedstock consisting of crude oil, naphtha and diesel from the Middle East. (World Bank, 2017)

This oil is refined at INDENI Petroleum Refinery Limited and sold to oil marketing companies (OMCs) who transport it by road to the service stations. Any significant changes in the structure and conduct of these two factors will trigger a price adjustment.

Since ERB price determination is driven by the principle of Cost Plus, it basically means that the final price of petroleum products should cover all the costs along the supply chain. In the case of Zambia, the costs that need to be covered are those on the upstream and downstream.

This means that each time a procurement of feedstock is made a process of adjustment in price is automatically triggered. On average, procurement of feedstock is done such that we receive a new shipment every six weeks. (Lieberherr, E., Klinke, A., & Finger, M. 2012).

However, in recommending price adjustments, ERB has set up a threshold of 2.5 per cent of the wholesale price, that is, for each cargo, if the required change in the wholesale price is more than 2.5 per cent then the ERB will recommend a price adjustment. However, if the required change in the wholesale price is less than 2.5 per cent, then no adjustment is made to the pump prices. In this case, the Government carries the burden of the cost that could have been passed on to the consumers. This is inherently a Government subsidy on fuel. The advantage inherent in this threshold system is that it helps to keep the prices stable and predictable, unlike in the IPP model which would allow prices to change almost on daily basis whenever the exchange rate or international oil prices change. (McCann, 2002: Calm 2017)

In the case of the Cost per Mile (CPM), the exchange rate and the international oil prices that are used hold until the cargo is exhausted, after about six weeks. This means that any benefit, such as price reduction, resulting from a positive change in the two key fundamental determinants of pricing is only passed on to consumers on cargo basis.

The CPM takes into account the following elements in arriving at the wholesale price on the upstream: cost of petroleum feedstock; cost of freight from place of sale to Dar-es-Salaam (C&F); insurance; ocean losses; wharfage (harbour charges); financing charges; and collateral manager fees. (Russell, D., Coyle, J. J., Ruamsook, K., Evelyn, A, 2014: Chunga 2024).

Derived from the price buildup is the wholesale price to OMCs that is further expanded to get the pump prices at retail sites. On the downstream; the price builds up to the retail level involves covering operational costs of Ndola Fuel Terminal (NFT); processing fees; taxation; OMC, transporters and retail dealer profit margins and some levies and fees such as the Strategic Reserve Fee (SRF) of particular interest is the SRF which was created to contribute towards the development of the petroleum infrastructure, such as the new oil depots in Lusaka and Mpika, and price stabilization in the country. (Chuhan-Pole, Punam. 2012: Oscar 2023).

Since 2000, the prices of fuel have risen steadily in tandem with mostly the movement in international oil prices and later in response to the volatility of the Kwacha. Petrol has continued to be priced more than diesel and kerosene. (Russell, D., Coyle, J. J., Ruamsook, K., Evelyn, 2014).

The pump prices of petrol, diesel and kerosene have remained stable since May 2010. Between this date and the 17th of April 2014, only one adjustment was made, that is on April 30, 2013, but this was mainly on account of removal of fuel subsidies as a Government policy and was not solely driven by change in the principle fundamentals, i.e. the exchange rate and international crude oil prices. Fuel price changes 2000 to 2013 With regard to the most recent fuel price increase, ERB announced the increment of fuel prices by an average of 8.3 per cent effective midnight April 17 2014. ERB increased the pump price of petroleum products by 7.22 per cent for petrol, 8.75 per cent for diesel and 9.54 per cent for kerosene, while wholesale prices were adjusted by 11.15 per cent. During this period, the exchange rate of the Kwacha against the US Dollar had depreciated significantly from K5.40 at the last price review in April 2013 to a level of K6.20 to the US Dollar, that is, by 14.8 per cent cumulatively. This cumulative depreciation of the Kwacha against the US Dollar was therefore, the major trigger for this fuel price increase.

The behaviour of the Kwacha around this period was partially as a result of a global phenomenon which had seen the US dollar gain significantly against other major currencies. This was principally driven by the world-wide reduction in US dollar domestic liquidity by the Federal Reserve Bank of the United States.

On a positive note, in the recent past, the price of international oil prices has remained fairly stable and has averaged US$110 per barrel (Business new 2018). Unless something unforeseen happens on the global supply side, the forecast is that these prices will hold for some time especially that new producers in oil such as Libya have now come back on the market. Of the two principle price determinants, the oil price has been less volatile. U.S. (2017). Energy Information Administration, Factors Affecting Diesel Prices.

With regard to the recent adjustment in fuel prices, the Government had procured about 90,000 tonnes of feedstock at a cost about US$94 million. Using the Cost Plus principle, the required price adjustment in wholesale prices, in order to attain full cost recovery, was 11.15 per cent.

This was well above the price adjustment threshold of 2.5 per cent. For this particular cargo, the associated loss was estimated at US$9.5 million (or K56.5 million) meaning that this is the “subsidy” that Government would have carried on this cargo if the cost was not passed on to consumers via a price increase. Without full cost recovery or losses on a feedstock cargo, the immediate implication is that in order to purchase the next oil tanker of feedstock, the Government would have to source more funds to add to the funds received from the sale of the previous cargo.

Therefore, in order to avert further losses and provide for adequate financial resources to sustain the continued purchase and supply of petroleum products, it becomes necessary to review prices at the pump so as to attain full cost recovery. Suffice to state that, an economic rationale decision has to be made on whether to have guarantee of fuel at a sustainable and economic price or to have no fuel at all. Uniform pump price regime ERB implemented Uniform Pump Pricing (UPP) in September 2010 following a Government policy directive.

Regional Perspective

Local factors such as inflation and tax may increase the fuel price at any given time. The international oil price also affects the entire globe and South Africa is certainly not excluded. Fortunately, SAPRA currently fills a gap in this area by saying they receive early notification of fuel price changes and notify our members ahead of time. (Akinboade, O. A., Ziramba, E., & Kumo, W. L. 2008).

In Burundi, drivers are so desperate for fuel that they sleep on forecourts of petrol stations. Senegal has so little jet fuel that Air France’s flight from the capital, Dakar, to Paris has been stopping in the Canary Islands to fill up. Johannesburg has the same problem, which has caused United Airlines to cancel some flights from New York. From Kenya, which recently suffered its worst petrol shortage in a decade, to Lagos, where queues outside petrol stations backed onto motorways, and Cameroon, where thousands of lorries have been stranded without diesel, Africa has been short of the lifeblood of modern economies. “Everywhere, everyone is scrambling for diesel,” laments Anibor Kragha of the African Refiners and Distributors Association. (Economics weekly 2022)

The economic costs of shortages are huge. they bring commerce to a grinding halt, shut the millions of businesses that have to generate their own electricity and force holidaymakers to cancel trips for lack of flights. this is a blow to tourism, a large contributor to GDP in many African countries. the social impact is large, too. hospitals cannot get drugs and ambulances are immobilised all this makes politicians jumpy anger at shortages to avoid quickly erupt in the streets. (De Jong, 2017)

Fuel theft is a serious issue in South Africa. Some Tips on prevention and monitoring as the fuel price steadily increases, the rise in fuel theft and fraud poses a serious threat to transporters and their operating profits. (Russell, D., Coyle, J. J., Ruamsook, K., Evelyn, A, 2014).

Edmeston (2018) states that, “As fuel costs continue to rise, illegal diesel skimming is going to take on new proportions. The reality is that rising transport and fuel costs, toll fees, vehicle maintenance costs, hijackings, fuel theft and the challenges around managing driver behavior and collusion are all placing enormous pressure on fleet owners and companies to find effective and sustainable ways of managing fleets and drivers.

“The popularity surrounding diesel derivatives in the passenger and LDV market, with the perceived saving in fuel consumption, has caused a big demand on diesel engines and has directly impacted the supply of diesel.”

A litre of petrol costs Sh234.72 on average in Kenya, compared to Sh152.95 in Tanzania and Sh165. 45 in Uganda. •Fuel prices in Kenya have always been the highest compared to the two countries. (Business new 2018) Fuel prices have become a challenge in the recent past because they are usually increasing at a speedy and sudden rate. Most often, much focus is placed on the effect of fuel prices on the lives of people. In such a case, people are advised on unnecessary spending by cutting down on fuel costs. Less attention however is placed on the effect of the high fuel prices on organisations, which cannot run without fuel since it facilitates almost all of the operations in any organisation. The airline industry precisely is overly reliant on fuel and as a result is deemed to be most affected by the high fuel prices. One such airline is the Dnata Company, whose survival is hanging on a thin thread given its current financial crisis. (Ivy Panda. 2019).

International Perspective

Intermodal transport network of peninsular Malaysia includes networks of single-mode transport networks such as highway, township roads, railways line and airways are the major consumer of petroleum in the country. The cost of fuel is determined by the demand and supply forces of the country compiled with new technology which helps the country to stock fuels in large quantity thus reviewing take time and people plain and prepare for the all year round on how much fuel they may need for certain activities and the profit they are likely to generate.

According to (Paul Kosakowski, Chip Stapleton and Yarilet Perez 2022) Oil still plays an important role in the global economy despite the continued efforts to reduce its use and to find alternative green energy sources still petrol is at high demand and usage. In USA Gasoline Prices Petroleum prices are determined by market forces of supply and demand, not individual companies, and the price of crude oil is the primary determinant of the price we pay at the pump. The price of crude oil is the main determinant of the price of gasoline, but refining costs, federal, state and local taxes, as well as marketing and distribution costs also affect gasoline prices.

The price of gas is also influenced by oil in its most natural state: crude oil. The type of crude oil that is available affects how much gas costs, and when desirable crude oil is less plentiful, prices go up. Oil is described as light or heavy, and sweet or sour. Though consumers buy gasoline locally, prices for the fuel are largely determined by the global market for crude oil from which it is made. When the price of crude oil in the global market changes whether due to geopolitical events, fluctuations in crude supply or gasoline demand prices that consumers pay at the pump change, too. the price of crude oil accounted for 53 percent of the price of gasoline. Local, state and federal taxes made up another 18 percent, while the cost to refine crude oil into gasoline accounted for 17 percent, and the cost to market and distribute gasoline to retail outlets made up 12 percent, according to the (U.S. EIA 2017). This breakdown can shift as crude prices change, and it can vary by region depending on taxes, manufacturing, marketing and distribution costs. In recent months, despite increasing U.S. crude oil production, global crude oil prices have climbed, reaching a three-year high in 2017, largely because of reduced crude oil supplies from OPEC and some non-OPEC countries. Gasoline prices have increased along with the price of crude. (AFPM Communications 2018)

The study adopted a deductive research approach and used a descriptive research design. Questionnaire and interviews were used to collect data. The study used purposive and snowball sampling technique to select respondents from the transporters that is bus drivers, tanker drivers, taxi drivers, private drivers and some selected companies that use crude fuel as their input. Simple survey was done and selected respondents were also interviewed. Statistical methods and excel analysis was used to interpret data collected during the research.

Target population

The research was conducted around industrial area, town center of Ndola and target some tax drivers. According to RATSA there only 102 registered taxis in Ndola thus, Ten (10) tax drivers were targeted and there about 298 tankers which are registered in Ndola thus, twenty (20) tanker drivers as well as some organisations which depend on fuel as their input into their products. According to Martinez J. Mesa (2014) one third of the population is good enough to represent the entire study in a qualitative study.

Sampling frame

The study is going to used purposive sampling technique to select respondents comprised of business men and women in Ndola town center they would best provide the information necessary to answer the research questions and some selected employees and household will not be left out. 1/3 * 400 = 133 respondents. The sample size identified and used by the study was 130 employees.

Data collection instruments and procedures

The data collection instruments that the study was used to gather the desired information and results for this research were Questionnaires, which enabled the researcher to clarify the intention of the research to the sample respondents. The researcher interviewed and observed the respondents face to face, allocating ten to fifteen minutes’ duration to ask the necessary questions.

Data Analysis

The study used statistical methods to analyze quantitative data in the relationship between the dependent variable which is financial capacity of transporters, depress supply of other goods, high inflation and speculation. On the independent variable which is monthly fuel price review. The formulated hypothesis wound be tested using Pearson correlations generated by SPSS software at 95 percent confidence interval.

Study Limitations

The other challenge was the limitation in the area of study, the research permission was only limited to one province that is Copperbelt and only 130 respondents were approached in the Copperbelt provinces which was a challenge to the research to get a clear picture on the review of the effect of monthly fuel adjustment and how it can be improved with justifiable findings and recommendations. Another notable challenge was on the confidentiality of data which affected data collection as some respondents were not comfortable to release information having the organisation’s approval to conduct the study.

The limitations of the study bordered on the research instruments. The researcher used a questionnaire to gather the data and most of the participants did not answer all the questions accurately. The researcher also used interview guides to collect data and the respondents did not answer sensitive questions of the study. However, the researcher addressed these limitations by using instrumental triangulation that is questionnaires, interviews and focus group discussion to collect data. A gap in one research instrument was supplemented by the other research instruments. The researcher also addressed these limitations by assuring the respondents of anonymity and confidentiality.

Ethical Consideration

Consent was asked from all the respondents. Ethical researchers do not present the work of others as their own. Ethical researchers do not fabricate or falsify data in their publications. If the experimenter discovers that the data published are erroneous, it is the experimenter’s responsibility to correct the error through retraction or other appropriate means. During data collections and data analysis ethical issues was put into consideration, this simply means that any material taken from other sources was cited. No one was force to give information of any sort. Also the request from the researcher to distribute questionnaires to participants was on a voluntary basis, participants were allowed to withdraw in the participation at any time and there were no rewards or any payments to participants it was hundred percent voluntary.

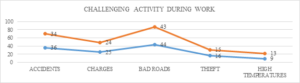

There various challenges faced by truck drivers as they go and come back from getting fuel from Dare-es-Salaam Fuel carrying vehicles (FCVs) are currently more expensive than conventional vehicles and hybrids. However, costs have decreased significantly because of good technology. Car makers must continue to lower costs, especially for the fuel cell stack and hydrogen storage, for FCVs to compete with conventional vehicles. Challenges among Zambian tank drivers are as shown below.

Figure A (Source: authors’ data 2025)

The most occurring challenge that influence Tanker drivers to be effective in their duty was according to how they have appeared on the graph. For instance, interviews were conducted twice on some question so as to be sure of what challenges bombard the drivers, it was discovered that the first challenge they all talked about was bad roads on both sides, that is Zambian side and Tanzanian sides. This challenge was accorded 90% in the first interview while on the second interview it was rated 45%. This was followed by road accidents which was rated as 70% and 38% in the second interview. The third challenge was that drivers complain of too much charges which rangers from toll fees, packing fees and weight fees this was rated at 70% in the first interview and 38% the other challenge was theft which the rated as 30% in the first interview and 16% in the second interview. Going by the result it was clear that truck drivers are faced with a lot of challenges to bring fuel into Zambia thus they play a role in determining the price of fuel because companies look at all the cost they incur in bringing the commodity into the country and they also look at other challenges before they can charge how much it is to bring fuel into Zambia.

Therefore, the challenges are itemized according to how they affect the drivers the first one being bad road which leads to accidents, followed by charges that drivers pay a lot of unexpected money in some potion of Tanzania and Zambia where drivers are charged sometimes for packing at some place when the driver what to refresh up. Some charges they complained about were country entry fee which they feel is the duplicate of the fees they pay at the toll gates and weigh bridge.

Does monthly fuel price review affect transporters (HR)

Tanker drivers are greatly impacted when it comes to monthly fuel review in that some respondents said that in some instance drivers load their commodity that is fuel and as they return back home unfortunately if they delay by a day or two only to hear that the fuel price has been increased or reduced without taking into consideration how much the product which is on the way was purchased thus they transporter are made to contribute to the loss in the quantity of fuel in case the price they purchased it was higher than what the government announce in the new month.

To avoid this loss or gain most of the transporters are not sending their trucks to go and get fuel in the last week of the month so that they are not caught in the web. Subsequently there is artificial shortage of fuel in the last week of the month which also cause the shortage of other commodities in the country.

Availability Of Fuel Along The Line Of Rail?

Table four (1)

| ALTERNATIVE | RESPONDENTS | PERCENTAGE |

| Very available | 70 | 53.8 |

| Available | 44 | 33.8 |

| Not available | 9 | 6.9 |

| Situation not good | 02 | 1.5 |

| Same situation | 05 | 3.9 |

| Total | 130 | 100 |

(Source: Author’s Field Survey, 2025)

The question was posed to find out the availability of fuel along the line of rail, 53.8% of the respondents said that fuel is very available to all the places not only along the line of rail this was attributed to that fact that the fuel transporters bring in the country is more than enough to cater for the entire country. While 33.8% also agreed to the assertion that fuel is available to places along the line of rail they further said that this was so because of private player on the market which help in ensuring that more littles of fuel is brought into the country while they are also benefiting in the way.

6.9% of the respondents said that fuel is not available especially on the outskate of the country, they further said that fuel is available in the first two weeks of the month but in the last one week their hiccups here and there. Some respondents said that situation is not good especially in some interior part of the rural areas which run dry of fuel completely while some respondents said that the situation is the same when fuel price is reviewed monthly and when fuel price was reviewed yearly.

A researcher did some mathematics by adding the figures 53.8% and 33.8% which gave 87.6% of the respondents who said that fuel supply is more than enough or fuel is available along the line of rail or generally in the country. While the addition 6.9% and 1.5% will only give 8.4% of the respondents who said that fuel was not available along the line of rail and in some parts of the country. Comparing the two figure that is 87.6% and 8.4% the researcher acknowledged that fuel is truly available along the line of rail because the figure 87.6% is very significant compared to 8.4% which is insignificant. Therefore, monthly fuel adjustment is seen to be problematic not only to transporters but the surrounding places this is so because not everyone agreed on availability of fuel 8.4% refused about the availability of the fuel.

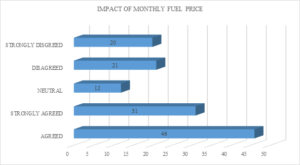

Do you agree that monthly fuel price review or adjustment impact on the performance of transporters and the economy in general?

Figure B (Source: Author’s Field Survey, 2025)

The respondents were asked a question to find out if monthly fuel adjustment has an impact on transporters and the economy as a whole. 46 respondents which translate to 35.4% agreed that monthly price adjustment has an effect on the transporters as well as the performance of the economy as whole. Another 31 respondents which also translates to 23.9% strongly agreed that monthly fuel price review impact mostly negatively on the transporters as well on the performance of the economy. Twelve (12) which translates to 9.2% of respondents who were neutral on this matter they did not agree nor disagree that monthly fuel price adjustment has an impact on the performance of the track or tanker drivers but they opted to remain quite on the subject matter. Some respondents in this category justified their answer by saying that they have never seen how the fuel price impact on the drivers and they have never seen or heard that the economy is not performing because of the fuel importation.

The other 21 respondents which is equivalent to 16.2% disagreed that monthly fuel price review has no impact on the transporters and the economy as a whole. Another 20 respondents which is 15.4% strongly disagreed that monthly price review has no impact on the transporters.

Table 2 data collected from the field

| VARIABLES | FUEL C1 | FUEL C2 | FUEL C3 | FUEL C4 | FUEL C5 | TOTALS |

| Strongly Agreed | 12 | 11 | 9 | 10 | 6 | 48 |

| Agreed | 18 | 15 | 7 | 2 | 8 | 50 |

| Neutral | 1 | 6 | 2 | 4 | 2 | 15 |

| Strongly Disagreed | 0 | 1 | 3 | 5 | 7 | 16 |

| Disagreed | 0 | 1 | 0 | 2 | 1 | 4 |

TOTALS |

31 | 34 | 21 | 23 | 24 | 133 |

(Source: Author’s data Set 2025)

Information from the table was feed into SPSS and it generated the information shown on table 3 below and some calculations were done by the software Statistical program for Social science.

Table 3: Chi-square table.

| Respondents’ View | Observed (Oi) | Expected (Ei) | Oi – Ei | (Oi – Ei)² | (Oi – Ei)² / Ei |

|---|---|---|---|---|---|

| Strongly Agreed | 48 | 11.29 | 36.71 | 1347.6 | 10.1 |

| Agreed | 50 | 8.65 | 41.35 | 1709.8 | 12.9 |

| Neutral | 15 | 2.25 | 12.75 | 162.6 | 1.2 |

| Strongly Disagreed | 16 | 4.09 | 11.91 | 141.8 | 1.1 |

| Disagreed | 4 | 0.72 | 3.28 | 10.8 | 0.08 |

| Totals | 133 | 27.03 | 106 | 3372.6 | 25.4 |

Oi is the observable frequency of cases in each while Ei the expected frequency of cases in each category. The table has 5 columns and 5 rows, therefore the degree of freedom (df) for this data is rows 5-1= 4. There 5 columns as well which give 5-1 = 4 therefore degree of freedom is (5-1) *(5-1) = 16 which translate to 0.16 as a point of reference or P-Value or as P-value picker. The chi-square statistical and the hypothesis are:

H1o. Monthly fuel price adjustment causes increase in prices of goods which impact transporters as human resource negatively. (alternative hypothesis)

H1i. Monthly fuel price adjustment does not cause increase in price of goods and does not impact on transporters as human resource negatively (null hypothesis)

<p>

\( (x)^n = \sum \dfrac{(O_i – E_i)^2}{E_i} \) <br>

\( 10.1 + 12.9 + 1.2 + 1.1 + 0.08 = 25.4 \approx 25 \text{ or } 0.25 \)

</p>

Using Chai Square distribution table or calculator, It was found that for df = 16 and Chai Square 25.4, the p-value is approximately 0.012

The chai-square statistical is significant in that 0.012 ˂ 0.16. Therefore, the null hypothesis is rejected or not accepted. In this research it was true that monthly fuel adjustment has a negative impact on the transporters i.e. human resource e.g. drivers and their families.

Importation of fuel is now done on probability that suppose they buy fuel from dar-es-salaam which take about two weeks to arrive if we purchase a week before month end then, it means that they may make a loss when the commodity is reduced thus they are calculating the importation to avoid a situation where price of the fuel is reduced than the amount the bout it at. This has created shortage of fuel especially in the last week of the month. Therefore, if fuel in the last week of the month become static it simply means that transporters are avoiding to go and get the commodity in that week. For example ( energy regulation board …March 2025 announced the drop in fuel prices at international market which will cause the decrease of fuel prices in Zambia too, but filling stations will make sure that they sell out their old stock before the new ones come in. they would also buy the cheap fuel within this month and sell it at higher price for profitability but if it was increase on the world market they would rather hold on to what they have in stock create artificial shortage only to sell when the new increased price is announced.

It has been observed that more drivers and petrol tanker operators have passed through grade seven and nine and grade twelve and not college and or University. This category of respondents are very good at acquiring skills and they are good at doing what they do best at the right time when the instructions are straight forward they follow them to the later until they achieve the given objective. When it comes to driving they know the roots very well from Zambia up to the point of loading in Dar-es-Salaam, in other word education level of these employees has nothing to do with their skills of driving and paying attention to details. Thus they know that fuel prices change every month of the year and they also wonder whether this has effect on the performance of the economy or not or whether it impacted on them as transporters.

There various challenges faced by Fuel Carrying Vehicles (FCVs) drivers as they carry out their duties of transporting fuel from Dare-es-Salaam, one of the challenges is that it is currently more expensive to drive such a vehicle to a far place like Tanzania than conventional vehicles and hybrids. Secondly the respondents itemised the challenges as according to how they affect the drivers the first one being bad road which leads to accidents, followed by charges that drivers pay a lot of unexpected money in some potion of Tanzania and Zambia where drivers are charged sometimes for packing at some place when the driver want to refresh up, they are charged they complained about the country entry fee which they feel is the duplicate of the fees they pay at the toll gates and weigh bridge. Because of so many point of paying they sometimes ends up using their own money instead of the company money. Fuel cell systems are not yet as durable as internal combustion engines, especially in some temperature and humidity ranges. On-road fuel cell stack durability is currently about half of what is needed for commercialization. Drivers are advocating for this device so that their vehicles can be as efficient as possible and reduce on the cost of transportation of fuel.

Sometimes drivers load their fuel say a week before month end unfortunately if the price is adjusted before they arrive without taking into consideration how much the product which is on the way was purchased thus they transporter are made to contribute to the loss in the quantity of fuel in case the price they purchased it was higher than what the government announce in the new month. To avoid this loss or gain most of the transporters are not sending their trucks to go and get fuel in the last week of the month so that they are not found in that situation. For example filling station which are along Kwacha road in Ndola like Engine filling station, Lake Petroleum, Puma and Total Filling stations did not have fuel on 2nd and 3rd of March 2025

According to table 1 it was discovered that 87.6% of the respondents who said that fuel supply is more than enough or fuel is available along the line of rail or generally in the country. While the 8.4% of the respondents said that fuel was not available along the line of rail and in some parts of the country. Comparing the two figure that is 87.6% and 8.4% the researcher acknowledged that fuel is truly available along the line of rail because the figure 87.6% is very significant compared to 8.4% which is insignificant. Therefore, monthly fuel adjustment is seen to be problematic in that it impacted greatly on the transporters as well as the economy of the country.

According to figure B. 46 respondents and 31 respondents agreed and strongly agreed respectively that monthly price adjustment has the impact on the transporters as well as the performance of the economy as whole. The question asked here was to find out if monthly fuel adjustment has an impact on transporters and the economy as a whole. Figure B give 77 respondents who agreed and strongly agreed respectively that monthly fuel price adjustment has negative impact on the transporters. In august 2022 the price of petrol and diesel was reduced by K 2.40 and K1.90 respectively and some tankers for Karim were stack at Mbeya in Tazania before a reduction, when the product arrived in the country it was sold at a loss thus the company is clipping with financial problem. In 2023 Zambia experienced substantial reduction in fuel prices for example petro reduced from K27.59 to K24.45 per litter, thereafter the prices have been going up today 18/03/2025 petrol is costing K35 per liter.

The monthly review of domestic fuel prices means that domestic prices of petroleum products will heavily rely on the performance of international oil prices and the kwacha-dollar exchange rate which are highly volatile. The adopting a 30-day pricing cycle strategy by Energy Regulation Board simply means that players have to make domestic prices of petroleum products which must follow the trend of international oil prices and the performance of the Kwacha against the US dollar. Prices will rise whenever a rise is recorded either in the international oil prices or when the environment allows an increase in the commodity.

Although Zambia has rail line and airline to transport goods and other services but all the goods and petroleum products are transported through roads which calls for more fuel consumption. These fuel in question was initially jets in the country through Tazama pipe line thus supply was constant and the price was reviewed when the international market adjust either upwards or downward. Previously fuel heavily subsidized today fuel price is reviewed every month end unfortunately this has brought about anxiety in the mind of bus drivers who make losses in their business when the price of fuel goes up, bus fair remains static. This same situation has put a number of transporters out of business. Today fuel is brought in the country by road with the help of tanker drivers which entails that the products to reach Zambia depends on how careful and accurate the driver may be, any slight mistake in driving the commodity may put the driver and other motorist at risk. Therefore, monthly price review of fuel impacts the drivers greatly.

Fuel is one of Zambia’s largest import products. The fuel supply chain and pricing are sensitive subjects that cause a lot of anxiety among different economic agents. Fuel pricing and the cost of fuel is, thus, among the most contentious issues on which a lot of dissimilar views are aired. A section of the Zambian society has the view that our fuel costs are comparatively high, in the region and the world, largely due to inefficiencies in the way fuel is imported. The government-led procurement system is said to be inefficient and protects the institutions involved from competition by setting high tariffs on finished products. This section of society argues that removing tariff protection and liberalising imports of finished products would reduce costs both by promoting competition and by allowing different regions to obtain supplies from the cheapest port.

Commodity prices: If fuel prices increase, you will have to pay more for the commodity as the input cost of companies would go up this would trigger an increase in the price of commodities. This is couple with the theory chosen for this research work which is the Economic theory and it states that the price for a specific good or service is determined by the relationship between its supply and demand at any given point. Prices should rise if demand exceeds supply and fall if supply exceeds demand. (Marshal G. 2014). The hypothesis which states that monthly fuel price adjustment reduces the financial capacity of transporters it was discovered that it was twofold it can either reduce or increase the financial capacity of the transporter depending on the circumstance prevailing at a time. Generally monthly fuel price review has a bearing on transporters.

Nonetheless, manufacturers can no longer bear the pressure from increased costs of fuel. Inevitably passing on increased costs of production emanating from increases in domestic fuel prices will have significant negative effects on the economy. This may result into higher inflation, increased levels of poverty and an increase in job losses from the transport sector. Lessons can be learnt from countries like Sri Lanka which suffered greatly from high oil prices before administering massive subsidies to cushion the negative effects of oil price increases.