Determinants and Impact of Credit Utilization among Rural Cocoa Farmers: Evidence from Ondo State, Nigeria

Olanrewaju Peter Oladoyin1, Oluwatosin Omotola Ajayi2, Ajolola Taibat Ibrahim3, Emmanuel Adesina Borokini4,

1Department of Agricultural Economics, Adekunle Ajasin University, P. M. B.001, Akungba-Akoko, Ondo State, Nigeria.

2Department of Economics and Finance for Development, The University of Bradford, Bradford, West Yorkshire. BD7 1DP. United Kingdom.

3Department of Agricultural Economics, Ekiti State University, Ado-Ekiti, Ekiti State, Nigeria

4Department of Agricultural Extension and Management, Rufus Giwa Polytechnic, P.M.B 1017, Owo, Ondo State, Nigeria.

Access to agricultural credit remains a pivotal driver of productivity and income growth among smallholder farmers in Sub-Saharan Africa. This study investigates the determinants and impact of credit utilization among cocoa farmers in the Akoko Southwest Local Government Area, Ondo State, Nigeria. Using primary data from 150 respondents selected through a multistage sampling technique, the analysis employed descriptive statistics, cost-return analysis, and binary logistic regression to evaluate credit access, usage patterns, and profitability outcomes between credit users and non-users. Results reveal that access to credit is strongly influenced by household size and marital status, with smaller households and unmarried farmers demonstrating more efficient credit use. While both formal and informal sources of credit exist, local savings mechanisms remain the predominant source due to the perceived complexity and high interest rates associated with institutional loans. Credit utilization was found to significantly enhance cocoa productivity by facilitating access to farm inputs such as fertilizers, pesticides, and improved seedlings. Furthermore, credit users exhibited higher gross margins, net farm incomes, and return on investment compared to non-users, indicating a positive financial impact. The study concludes that access to credit is a critical determinant of both input adoption and profitability in cocoa production. It recommends the strengthening of farmer cooperatives and the simplification of credit procedures to improve access and utilization. Targeted policy interventions that address constraints related to collateral, interest rates, and loan recovery protocols are also essential for boosting rural financial inclusion and agricultural performance.

Keywords: Agricultural credit, Cocoa production, Credit utilization, Farm profitability, Rural finance, Nigeria

Cocoa (Theobroma cacao) is a globally significant cash crop, contributing substantially to household incomes, national economies, and international trade, particularly in tropical regions. Nutritionally, cocoa beans are dense in essential macronutrients, containing approximately 20% protein, 40% carbohydrates, and 40% fat (Microsoft Encarta, 2019). Its high demand in global confectionery and cosmetic industries has positioned cocoa as a valuable export commodity. Sub-Saharan Africa remains the global epicenter of cocoa production, accounting for nearly 70% of the total world output (ICCO, 2020). Among the leading producers, Nigeria ranks third in Africa, contributing approximately 12% of the global cocoa supply, following Côte d’Ivoire (35%) and Ghana (13%) (Wilcox & Abbott, 2021). Since its introduction to Nigeria in 1874 (Oyedele, 2017), cocoa has become a critical livelihood asset for smallholder farmers, particularly in the southwest region.

Despite its economic relevance, cocoa productivity in Nigeria has been on a sharp decline. The Food and Agriculture Organization (FAO, 2020) reports that national yields have dropped by 0.8 tons per hectare annually over the past five years. The current average productivity stands at approximately 0.5 tons per hectare, which is significantly lower than the 1.5–2.0 tons attainable through improved hybrid varieties (FAOSTAT, 2018). This widening productivity gap is attributed to multiple structural constraints: poor soil fertility, outdated farming practices, pest and disease infestations, limited use of yield-enhancing technologies, and inadequate rural infrastructure (Suh & Molua, 2022).

To address this decline, several studies have recommended the adoption of improved agricultural technologies and capital-intensive practices such as mechanization, high-yielding seed varieties, fertilizer use, and irrigation (Adeleke et al., 2018). However, these solutions remain largely unaffordable for smallholder farmers due to persistent capital limitations (Liverpool-Tasie et al., 2011). As a result, the capacity of cocoa farmers to invest in productivity-enhancing inputs is severely constrained. This challenge underscores the critical role of agricultural credit in enhancing farm productivity and rural livelihoods. Credit serves as a vital input, enabling farmers to purchase inputs, hire labour, and expand cultivation. However, access to credit among cocoa farmers remains insufficient and inequitable. Most smallholders rely on informal credit mechanisms, such as local cooperatives or savings groups, which provide limited funds and often lack structured repayment systems (Kehinde & Ogundeji, 2022).

Formal credit institutions—including commercial banks and microfinance organizations—offer more substantial financing but are hindered by high interest rates, collateral requirements, and bureaucratic complexities (Oke et al., 2019; Joshi et al., 2021). These barriers discourage participation and perpetuate a cycle of low investment, low productivity, and entrenched poverty in rural areas (Mukasa et al., 2019; Ige & Adeyemo, 2019). Although various credit schemes have been introduced by government and development partners, their impacts have been limited due to poor implementation, low awareness, and farmer distrust of formal institutions (Alao et al., 2020). Consequently, cocoa farmers remain marginalized from formal financial systems, reducing their ability to scale production and improve livelihood outcomes.

In light of these challenges, this study investigates the determinants and implications of credit utilization among cocoa farmers in the Akoko Southwest Local Government Area of Ondo State, Nigeria. Specifically, the study aims to:

By shedding light on the financial behaviours of cocoa farmers, this study contributes to evidence-based policymaking for enhancing rural credit access, agricultural productivity, and poverty alleviation in Nigeria.

This study was conducted in the Akoko South-West Local Government Area (LGA) of Ondo State, Nigeria. Established in 1996 with its headquarters in Oka-Akoko, the LGA spans approximately 226 km² and lies within the tropical savannah climate zone. It experiences average temperatures of 28°C and humidity around 60%. According to the 2006 census, the population stands at 239,486, predominantly comprised of Yoruba-speaking people. Islam and Christianity are the major religions, and both Yoruba and English are widely spoken.

Akoko South-West comprises several towns and villages, including Ayegunle, Iwaro, Oka-Akoko, Iboropa, and Ikakumo. The area’s economy is primarily agrarian, with notable cultivation of oil palm and local engagement in crafts such as pottery, weaving, and carving. Key markets like Aluta and Ibaka support active trade and commerce. Cultural festivals such as Odun Ijesu and Egungun remain integral to community life. Landmarks include Oke Maria and the Central Mosque in Akoko. According to Deji et al. (2013), over half (52.7%) of youth are engaged in crop and livestock production, though relatively few participate in value addition. The region reflects a blend of agricultural vibrancy, cultural heritage, and untapped youth potential for agribusiness development.

Figure 1: Map of Ondo State indicating Akoko Southwest LGA

Source: Adopted from Adetoro et al (2015).

The data used for this study were primary. Data were collected from the field using a well-structured questionnaire with open and closed-ended questions. The questionnaire was designed to get required information from the respondents, asking their source of credit, what the credit institution required before giving out loans, the problem faced by the cocoa farmers in sourcing for loans, and how effective the utilization of credit by cocoa farmers in the study area.

In carrying out this study, a multi-stage sampling technique was used for the study. At the first stage, 5 communities were purposively selected based on the preponderance of the cocoa farmers. The second stage involved the random selection of 3 villages in each of the selected 5 communities. In the last stage, 5 users and non-users of credit for cocoa farmers were selected from each of the 3 villages using the snowball sampling technique, thus giving a sample size of one hundred and fifty respondents for the study.

Data were analyzed using descriptive statistics, binary logistics regression and budgeting techniques. Descriptive was used to describe the socio-economic characteristics of the respondents and identify the various sources of agricultural credit available to cocoa farmers in the study area and the problems encountered by the farmers in sourcing for credit.

Descriptive Statistics

Descriptive statistics such as mean and frequency table were used to analyze the socio-economic characteristics of the respondents, percentages were used to describe various sources of agricultural credit available in the study area.

Budgetary Analysis

This was used to determine the costs and returns of the credit users and non-users in the area.

The equations are specified as:

Total revenue (TR) = P * Q, where P is price per kg and Q is quantity sold in bags or kg.

Total cost (TC) = Total Variable Cost (TVC) + Total Fixed Cost (TFC)

Profit (π) = TR- TC

Return on Investment (ROI) = TR/TC

Where ROI is greater than 1, the enterprise is profitable. Otherwise, it is not.

Binary Logistics Regression

Some of the factors that influence the credit utilization of cocoa farmers were determined quantitatively using binary logistics regression. The Binary Logistics function postulates for cocoa farmers in the study area is explicitly presented by the following equation:

<!DOCTYPE html>

<html>

<head>

<script src=”https://polyfill.io/v3/polyfill.min.js?features=es6″></script>

<script id=”MathJax-script” async src=”https://cdn.jsdelivr.net/npm/mathjax@3/es5/tex-mml-chtml.js”></script>

</head>

<body>

<p>

The quadratic formula is: <br>

\( x = \frac{-b \pm \sqrt{b^2 – 4ac}}{2a} \)

</p>

</body>

</html>

where;

Li = Dependent variable

Pi = User of credit = 1

1-Pi = Non-User of credit = 0

X1 = Age (years)

X2 = Sex (male = 1 and female = 0)

X3 = Educational level (years spent in schooling)

X4 = Marital status (married = 1 and 0, otherwise)

X5 = Years of farming experience (years)

X6 = Household size (numbers)

X7 =Total farm size (ha)

µ = Error term.

Socio-Economic Characteristics of Respondents in the Study Area

This section presents the socio-economic attributes of cocoa farmers surveyed in the area. Key variables include age, gender, marital status, educational level, household size, years of farming experience, and enterprise characteristics. These factors are critical in understanding credit access and utilization behaviour among rural farmers. Table 1 highlights distinct characteristics between credit users and non-credit users. The age distribution indicates that most respondents were within the 51–60-year age bracket, comprising 48.8% of credit users and 45.7% of non-credit users. The average ages were 45.5 and 45.2 years for credit users and non-users, respectively. These findings are consistent with Wole-Alo et al. (2022), who reported similar age profiles among cocoa farmers in Ondo State, emphasizing that middle-aged farmers remain highly active in cocoa production. Gender analysis reveals that cocoa farming in the study area is male-dominated. Among credit users, 80% were male, compared to 90% among non-credit users. This trend mirrors findings by Kehinde & Ogundeji (2022), who observed that men are more likely to access agricultural credit and participate in commercial cocoa farming due to sociocultural norms and land tenure structures that favour male ownership and mobility.

Marital status also emerged as a key demographic factor. A majority of the respondents—95% of credit users and 84.3% of non-credit users—were married, while none were single. This suggests that married individuals, often with family responsibilities, are more engaged in cocoa production, potentially due to the stability and labour support that family units provide. This observation aligns with the findings of Adebayo et al. (2022), who noted that marital status positively correlates with credit access and farm productivity. Regarding education, the majority of respondents had formal education, with only 18.3% lacking any formal schooling. Notably, credit users were more educated overall—5% held tertiary education—compared to non-users. Educational attainment is critical as it enhances farmers’ capacity to understand credit terms, adopt new technologies, and navigate institutional processes. This supports Chekol et al. (2022), who emphasized the pivotal role of education in improving agricultural decision-making and credit uptake among rural households.

Farming experience also differed between groups. A substantial proportion of credit users (63.7%) and 40% of non-credit users had between 7 and 12 years of farming experience. This reinforces the assertion by Bukhari (2016) that experience enhances farmers’ efficiency in managing resources, assessing risk, and accessing institutional support. Experienced farmers are also more likely to have built creditworthiness and trust with lenders over time. Household size was another distinguishing factor. Credit users reported smaller household sizes (mean = 1.53) compared to non-credit users (mean = 1.93). This finding may imply that farmers with fewer dependents allocate resources more efficiently, allowing greater focus on credit repayment and farm investment. It echoes the conclusions of Wole-Alo et al. (2022), who noted that smaller households often exhibit better credit utilization behaviour due to reduced consumption pressure.

Table 1: Socio-Economic Characteristics of the Respondents

| Variable | Users | Non-users | ||

| Gender | Frequency | Percentage | Frequency | Percentage |

| Male | 64 | 80 | 63 | 90.0 |

| Female | 16 | 20 | 7 | 10.0 |

| Marital Status | ||||

| Single | – | – | – | – |

| Married | 76 | 95.0 | 59 | 84.3 |

| Widowed | – | – | 11 | 15.7 |

| Divorced | 4 | 5.0 | – | – |

| Age | ||||

| 21-30 | 1 | 1.3 | 1 | 1.4 |

| 31-40 | 11 | 13.8 | 19 | 27.1 |

| 41-50 | 29 | 36.3 | 18 | 25.7 |

| 51-60 | 39 | 48.8 | 32 | 45.7 |

| Educational Level | ||||

| No formal education | 13 | 16.3 | – | – |

| Primary school education | 30 | 37.5 | 14 | 20.0 |

| Secondary school education | 33 | 41.3 | 56 | 80.0 |

| Tertiary school education | 4 | 5.0 | – | – |

| Household Size | ||||

| 1-6 | 38 | 47.5 | 35 | 50.0 |

| 7-12 | 42 | 52.5 | 18 | 25.7 |

| 13-18 | – | – | 6 | 8.6 |

| 19-24 | – | – | 9 | 12.9 |

| 25-30 | – | – | 2 | 2.9 |

| Experience | ||||

| >13 | 51 | 63.7 | 28 | 40.0 |

| 13-18 | 9 | 11.3 | 23 | 32.9 |

| 19-24 | 7 | 8.8 | 19 | 27.1 |

| 25-30 | 7 | 8.8 | – | – |

| 30 and above | 6 | 7.5 | – | – |

| Farm Size | ||||

| 1-5 | 41 | 51.2 | 23 | 32.7 |

| 6-10 | 28 | 35.0 | 47 | 67.1 |

| 11-15 | 11 | 13.8 | – | – |

| Total | 80 | 100.0 | 70 | 100.0 |

Utilization of Credit Funds by Cocoa Farmers

Understanding how farmers utilize credit provides insight into their financial behaviour, priorities, and the potential impact of credit on welfare and agricultural productivity. Table 2 summarizes the distribution of responses regarding the use of secured loans among credit users in the study area. The findings reveal that the most frequently cited use of credit was as a strategy to address poverty-related challenges. Specifically, 23.8% of respondents reported often using loans as a “blueprint to solve poverty”, with this use ranked highest (mean = 2.39). This suggests that many cocoa farmers perceive credit not only as a production input but also as a means of coping with household-level deprivation. This aligns with the findings of Faloni et al. (2022), who observed that cocoa farmers in Nigeria often allocate credit to both economic and welfare-enhancing activities.

The second-ranked use of funds was reinvestment into farming operations. Approximately 47.5% of respondents often diverted loan resources into cocoa farming, with a mean score of 2.17. This indicates a productive use of credit for input purchases, labour hire, and other farm-related expenditures, consistent with earlier observations in rural agricultural finance literature (Kehinde, 2022). Promoting saving habits ranked third (mean = 2.11), with over half (53.8%) of the respondents indicating that credit enabled them to initiate or strengthen savings behaviour. This reflects a growing financial consciousness among rural farmers, where borrowed capital is used not only for immediate consumption but also to buffer against future shocks.

Other uses of funds included social functions (mean = 1.84), home purchases (mean = 1.61), and lending to other farmers (mean = 1.55), indicating informal intra-community credit sharing networks. Credit was also employed for children’s education (mean = 1.53), reflecting households’ commitment to long-term human capital development. Less frequent uses of credit included luxury expenditures such as buying cars (mean = 1.44), investment in non-agricultural businesses (mean = 1.37), holiday trips (mean = 1.33), and family ceremonies like weddings (mean = 1.40). These uses, although ranked lower, suggest that a fraction of the loans may be diverted to non-productive or consumption-driven purposes, potentially undermining repayment capacity.

Overall, the findings indicate a multifaceted utilization of credit—balancing agricultural reinvestment, welfare improvement, and occasional non-farm expenses. The trend underscores the importance of financial literacy and credit monitoring mechanisms to ensure the productive deployment of borrowed capital.

Table 2: Distribution of Respondents by Use of Funds after Securing Loans

| Use of Funds | Often | Not often | ||||

| Frequency | Percentage | Frequency | Percentage | Mean | Rank | |

| Blueprint to solve poverty | 19 | 23.8 | 46 | 57.5 | 2.39 | 1st |

| Diverting into my farming | 38 | 47.5 | 28 | 35.0 | 2.17 | 2nd |

| Promote saving habits | 43 | 53.8 | 23 | 28.7 | 2.11 | 3rd |

| Other social functions | 35 | 43.8 | 16 | 20.0 | 1.84 | 4th |

| Purchase of a home | 9 | 11.3 | 20 | 25.0 | 1.61 | 5th |

| Lending out to other farmers | 44 | 55.0 | – | – | 1.55 | 6th |

| For children’s education | 42 | 52.5 | – | – | 1.53 | 7th |

| Buying of luxurious cars | 7 | 8.8 | 14 | 17.5 | 1.44 | 8th |

| To undertake long investment | 33 | 41.3 | – | – | 1.41 | 9th |

| For children’s wedding | – | – | 16 | 20.0 | 1.40 | |

| Business outside farming | 30 | 37.5 | – | – | 1.37 | 10th |

| Provide better standard of living | 18 | 22.5 | 5 | 6.3 | 1.35 | 11th |

| Holiday trips | 14 | 17.5 | 6 | 7.5 | 1.33 | 12th |

Mean response ≥ 1.5

Contribution of Credit Facilities to the Quality and Quantity of Cocoa Production

Credit availability plays a vital role in enhancing both the quality and quantity of agricultural output. In this study, credit users were asked to evaluate the impact of credit facilities on various dimensions of cocoa production. Table 3 presents the distribution of responses across six key production parameters. The findings reveal that the most significant contribution of credit facilities was enhanced access to farm inputs, particularly pesticides and fertilizers. With a mean response score of 2.35, 55% of respondents rated this contribution as “average,” 25% as “above average,” and 20% as “very high.” This suggests that credit plays a critical role in improving input intensity, a key determinant of farm productivity. This result supports earlier findings by Wole-Alo et al. (2022), who reported that timely credit access facilitated better pest and weed control, contributing to improved cocoa yield in Ondo State.

Increased yield was the second-highest ranked contribution of credit facilities (mean = 1.94), with 86.3% of respondents rating the contribution as “above average.” Although only 10% considered the yield impact to be “very high,” the data indicates that most farmers recognize the productivity-enhancing potential of credit-facilitated input usage. Access to improved seedlings was also positively associated with credit usage, achieving a mean score of 1.63. Approximately 67.5% of respondents indicated that credit significantly improved their ability to obtain quality planting materials. This aligns with the broader literature on agricultural finance, which underscores the importance of credit in enabling the adoption of improved technologies and inputs (Kehinde, 2022).

On the other hand, contributions such as hiring of competent labour (mean = 1.49), adoption of modern farm machinery (mean = 1.45), and expansion of farm size (mean = 1.25) were rated lower by respondents. This implies that while credit access is pivotal for input procurement and yield improvement, it is less commonly used to scale production through mechanization or land acquisition—possibly due to limited loan sizes or short repayment periods, which may discourage long-term investment. These findings highlight the central role of credit in intensifying cocoa production, particularly through access to inputs and productivity-enhancing resources. However, the relatively limited application of credit toward mechanization and farm expansion indicates a need for longer-term and higher-value credit facilities to support structural transformation in smallholder cocoa farming.

Table 3: Distribution of Respondents by Contribution of Credit Facilities to the Quality and Quantity of Cocoa Production

| Contribution | Very high | Above average | Average | ||||||||

| Freq | Percent | Freq | Percent | Freq | Percent | Mean | Rank | ||||

| Access to the use of farm input (Pesticides and fertilizers) | 16 | 20.0 | 20 | 25.0 | 44 | 55.0 | 2.35 | 1st | |||

| Increase in yield | 8 | 10.0 | 69 | 86.3 | 3 | 3.8 | 1.94 | 2nd | |||

| Access to improved seedlings | 54 | 67.5 | 2 | 2.5 | 24 | 30.0 | 1.63 | 3rd | |||

| Hiring competent labour | 59 | 73.8 | 3 | 3.8 | 18 | 22.5 | 1.49 | 4th | |||

| Increase in the use of modern farm machinery | 44 | 55.0 | 36 | 45.0 | – | – | 1.45 | 5th | |||

| Increase in farm size | 60 | 75.0 | 20 | 25.0 | – | – | 1.25 | 6th | |||

Mean response ≥1.5

Cost and Return Analysis of Cocoa Farmers

This section presents the cost structure, revenue performance, and profitability differentials between credit users and non-credit users among cocoa farmers in the study area. Access to credit is hypothesized to enhance investment capacity, input intensity, and, ultimately, farm profitability. The results indicate a significant difference in revenue generation between the two groups. Credit users recorded a total revenue of ₦13,000,200, while non-credit users earned ₦5,607,200, suggesting that access to credit enables farmers to expand operations and improve output. Labor and input costs—particularly for pesticides, herbicides, and seedlings—were substantial components of the production budget for both groups, emphasizing their critical role in cocoa farming.

Moreover, the net farm income of credit users (₦8,850,850) was more than triple that of non-credit users (₦2,776,850). Similarly, the gross margin—which reflects returns before fixed costs—was significantly higher among credit users (₦10,270,850) compared to non-users (₦4,196,850). This outcome reinforces the assertion by Wole-Alo et al. (2022) that access to credit significantly boosts farm-level income among cocoa growers in Nigeria. In terms of efficiency, the Return on Investment (ROI) was 3.1 for credit users and 2.0 for non-credit users, indicating that every ₦1 invested by credit users returned ₦3.10, while non-credit users generated ₦2.00. This clear profitability differential underscores the transformative potential of financial access in smallholder agriculture. In summary, the cost and return analysis confirms that credit access facilitates the acquisition of yield-enhancing inputs, expansion of farm size, and ultimately improved profitability. This finding highlights the importance of inclusive financial systems tailored to small-scale cocoa producers.

Table 4: Comparative Cost and Return Analysis of Credit and Non-Credit Users

| Item | Credit Users (₦) | % of Total Cost | Non-Credit Users (₦) | % of Total Cost |

| Revenue | 13,000,200 | — | 5,607,200 | — |

| Variable Costs | ||||

| Cocoa seedlings | 80,000 | 1.9 | 200,000 | 8.4 |

| Fertilizer | 48,850 | 1.2 | 10,350 | 4.5 |

| Labour | 1,600,000 | 38.6 | 500,000 | 43.6 |

| Herbicides | 240,500 | 5.8 | 100,000 | 3.0 |

| Pesticides | 520,000 | 12.5 | 100,000 | 3.5 |

| Transportation | 240,000 | 5.8 | 500,000 | 17.6 |

| Total Variable Cost (TVC) | 2,729,350 | 65.8 | 1,410,350 | 80.6 |

| Fixed Costs | ||||

| Cutlass | 152,000 | 3.7 | 152,000 | 0.2 |

| File | 68,000 | 1.6 | 68,000 | 0.2 |

| Knapsack sprayer | 800,000 | 19.3 | 800,000 | 1.7 |

| Wheelbarrow | 400,000 | 9.6 | 400,000 | 17.3 |

| Total Fixed Cost (TFC) | 1,420,000 | 34.2 | 1,420,000 | 19.4 |

| Total Cost (TC) | 4,149,350 | 100.0 | 2,830,350 | 100.0 |

| Net Farm Income (TR–TC) | 8,850,850 | — | 2,776,850 | — |

| Gross Margin (TR–TVC) | 10,270,850 | — | 4,196,850 | — |

| Return on Investment (ROI) | 3.1 | — | 2.0 | — |

Gross Margin Comparison Between Credit Users and Non-Credit Users

To further underscore the profitability differences between cocoa farmers with and without access to credit, a gross margin analysis was conducted. The gross margin represents the difference between gross revenue and variable cost and provides a key indicator of short-term profitability and operational efficiency, excluding fixed costs. As presented in Table 5, credit users significantly outperformed non-credit users across all profitability indicators. Credit users incurred a total production cost of ₦4,149,350 and generated a gross revenue of ₦13,000,200, resulting in a gross margin of ₦10,270,850 and a net farm income of ₦8,850,850. In contrast, non-credit users spent ₦2,830,350 to generate ₦5,607,200 in gross revenue, yielding a gross margin of ₦4,196,850 and a net farm income of ₦2,776,850.

The higher financial returns for credit users demonstrate the instrumental role of credit in improving access to farm inputs, labour, and operational resources that enhance productivity. These findings are consistent with Wole-Alo et al. (2022), who noted that cocoa farmers in Ondo State with access to credit exhibited significantly better profitability margins than their non-credit counterparts. This analysis reinforces the argument that expanding access to affordable agricultural credit is not only a pathway to higher yields but also a critical strategy for improving rural incomes and promoting sustainable cocoa production.

Table 5: Gross Margin and Profitability Comparison for Cocoa Farmers

| Category | Total Cost (₦) | Gross Revenue (₦) | Gross Margin (₦) | Net Farm Income (₦) |

| Credit Users | 4,149,350 | 13,000,200 | 10,270,850 | 8,850,850 |

| Non-Credit Users | 2,830,350 | 5,607,200 | 4,196,850 | 2,776,850 |

Factors Influencing Credit Utilization Among Cocoa Farmers

To identify the socio-economic variables influencing credit utilization among cocoa farmers in the area, a binary logistic regression model was employed. In the model, credit utilization was defined as a binary dependent variable, with “1” representing users of credit and “0” for non-users. The model exhibited strong explanatory power, with a Nagelkerke R-square value of 0.956 and a Cox & Snell R-square of 0.428. The -2 Log Likelihood value of 2.773 further confirmed the model’s robustness and suitability for analysis.

The regression results revealed that six variables significantly influenced credit utilization at the 5% level: education level, marital status, years of farming experience, household size, and total farm size. Marital status had a negative and highly significant coefficient (β = -0.552, p < 0.01), indicating that unmarried cocoa farmers were more likely to utilize credit compared to their married counterparts. This could be due to fewer household responsibilities and greater financial flexibility among unmarried individuals, making them more efficient in directing credit toward productive purposes. Household size was also negatively associated with credit utilization (β = -0.357, p = 0.001). This suggests that farmers with smaller household sizes were more efficient and judicious in their use of credit. Smaller households may have fewer dependents and, consequently, less financial pressure, allowing them to allocate credit more effectively toward agricultural investments rather than consumption.

Education level exhibited a positive and statistically significant effect on credit utilization (β = 0.175, p = 0.027). Educated farmers are more likely to understand loan terms, fulfill institutional requirements, and access credit opportunities, thereby increasing their chances of utilizing formal or informal credit services effectively. This aligns with existing literature that highlights the role of education in enhancing farmers’ financial decision-making capabilities. Similarly, years of farming experience showed a positive and significant relationship with credit utilization (β = 0.174, p = 0.005). Experienced farmers are more familiar with farming cycles, input use, and credit mechanisms, and they are often perceived by lenders as more reliable borrowers due to their track record and knowledge of agricultural practices.

Total farm size also had a positive and significant influence on credit utilization (β = 0.185, p = 0.037). Larger farm sizes may improve farmers’ access to credit by increasing their potential for higher returns, and in some cases, serving as collateral for loan applications. This relationship suggests that farmers with more extensive landholdings are more inclined to use credit for the expansion and intensification of their operations.

In contrast, the coefficients for age and gender were statistically insignificant, with p-values of 0.996 in both cases. These results suggest that neither variable had a meaningful influence on credit utilization in the study area. Although commonly associated with agricultural participation, in this context, neither age nor gender significantly affected whether a farmer accessed or utilized credit.

Table 6: Logistic Regression Results – Determinants of Credit Utilization

| Variable | Coefficient (β) | Standard Error | Significance (p-value) |

| Age | -0.177 | 0.401 | 0.996 |

| Gender | 0.892 | 1.737 | 0.996 |

| Education Level | 0.175* | 0.081 | 0.027 |

| Marital Status | -0.552* | 0.112 | 0.000 |

| Years of Farming Experience | 0.174* | 0.039 | 0.005 |

| Household Size | -0.357* | 0.065 | 0.001 |

| Total Farm Size | 0.185* | 0.084 | 0.037 |

| Constant | -3.178 | 0.529 | 0.000 |

*Significant at the 5% level

Constraints Associated with Obtaining Credit

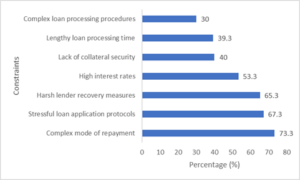

Understanding the barriers that hinder cocoa farmers from accessing credit is essential for developing inclusive financial policies. Findings from the study reveal that several institutional and procedural constraints significantly affect farmers’ ability to secure credit. These constraints, as summarized in Figure 2, were ranked by frequency and perceived severity based on respondents’ experiences.

The most widely reported constraint was the complexity of the loan repayment process, cited by 73.3% of respondents. Many farmers viewed existing repayment structures as inflexible, difficult to comply with, or misaligned with the seasonal nature of cocoa farming incomes. The rigidity of repayment schedules may deter farmers from applying for credit, even when the funds are needed for productive investments. The second most prevalent constraint, reported by 67.3% of farmers, was stressful and time-consuming protocols in obtaining loans. These include excessive documentation, bureaucratic bottlenecks, long processing periods, and general procedural inefficiencies within formal financial institutions. Such administrative burdens discourage especially smallholder farmers who may lack the formal records or literacy required to navigate the process efficiently.

A further 65.3% of respondents identified harsh recovery measures by lenders as a major concern. Many farmers expressed fear over aggressive loan recovery practices that may involve public shaming, asset seizure, or legal threats, all of which contribute to mistrust in formal credit systems. This fear of punitive consequences, particularly in the event of crop failure or delayed returns, discourages loan uptake. High interest rates were cited by 53.3% of respondents as another constraint. For many smallholder farmers, the cost of borrowing is prohibitive, especially when credit is sourced from formal institutions. High interest rates not only reduce the attractiveness of credit but also increase the risk of default, especially under fluctuating commodity price conditions.

Other notable constraints include lack of collateral security, reported by 40% of respondents, and lengthy loan processing time, noted by 39.3%. Many cocoa farmers, especially those operating at a subsistence or semi-commercial level, lack the legal land titles or tangible assets typically required by financial institutions to secure loans. Similarly, the extended duration it takes to approve and disburse loans reduces their relevance during critical farming periods, such as planting or input procurement seasons. Lastly, complex loan processing procedures were highlighted by 30% of respondents. This constraint overlaps with previously mentioned issues but emphasizes the cumulative burden of paperwork, institutional red tape, and low transparency in credit terms.

Figure 2: Constraints Associated with Obtaining Credit Among Cocoa Farmers

This study investigated the socio-economic characteristics, credit utilization patterns, profitability, and institutional constraints faced by cocoa farmers in the Akoko Southwest Local Government Area, Ondo State, Nigeria. The cost and return analysis revealed that access to credit had a significant positive impact on farm performance. Credit users achieved substantially higher revenues and profitability compared to non-users, confirming that access to financial capital enhances the acquisition of critical inputs and expansion of farm operations. Specifically, credit users generated a gross revenue of ₦13,000,200 and a net farm income of ₦8,850,850, while non-credit users recorded ₦5,607,200 and ₦2,776,850, respectively.

Further analysis of the determinants of credit utilization showed that marital status, household size, education level, farming experience, and total farm size were statistically significant predictors. Unmarried farmers and those with smaller household sizes demonstrated more efficient use of credit. These results suggest that social and economic household dynamics, as well as human capital, play a critical role in shaping credit access and utilization outcomes.

The study also identified key institutional barriers limiting access to credit. A majority of respondents (73.3%) cited complex repayment procedures as a major constraint, while 67.3% and 65.3% indicated that stressful application protocols and harsh recovery methods, respectively, discouraged them from seeking formal credit. Additionally, 53.3% of farmers highlighted high interest rates as a significant disincentive. These findings reflect a deep-seated distrust in formal financial systems and emphasize the need for reforms that align financial services with the realities of rural agriculture.

Based on the findings, several recommendations are proposed. First, rural cocoa farmers should be encouraged to mobilize into well-structured cooperative societies. Such collectives can serve as platforms for pooled savings, group lending, and collective bargaining, thereby improving their access to credit and agricultural inputs. Second, commercial banks and microfinance institutions must streamline their loan application and disbursement processes. Simplifying documentation requirements, introducing flexible repayment plans, and ensuring transparency will enhance farmer confidence and participation. Lastly, government intervention is crucial. Increased public investment in cocoa production, especially through budgetary allocations, extension services, and rural infrastructure, will strengthen the cocoa sector and uplift the livelihoods of smallholder farmers.

In conclusion, expanding access to affordable and farmer-friendly credit is essential for enhancing cocoa productivity, profitability, and rural development. Addressing the institutional and structural constraints identified in this study can lead to more inclusive financial systems that support sustainable agricultural growth in Nigeria.