An Investigation on Constituency Development Funds (CDF) and Citizens Economic Empowerment Commission (CEEC) Loan Compliance by Medium Small and Micro Enterprises (MSMEs): A Case Study of Chinsali District (Zambia)

Kataba Cornelious

The University of Zambia, School of Business and Graduate Studies

DR. RAMEEZ HASSAN

GHSS, Silmoo Kargil Jammu & Kashmir, India.

Temwani Zulu (MSc)

Ministry of Education, Zimba. Zambia.

This study investigated Constituency Development Funds (CDF) and Citizens Economic Empowerment Commission (CEEC) Loan Compliance by Medium Small and Micro Enterprises (MSMEs) In Chinsali. The study was done to further comprehend the factors that limit CDF/CEEC loan compliance by MSMEs. The study intended to attain the following objectives: examine the level of compliance of CDF/CEEC loan requirement, evaluate different factors that influence compliance with loan Conditions by MSMEs, Assess the economic impact of CDF and CEEC loans on the growth and sustainability of MSMEs. The study applied Quantitative research methods to drive the findings where a total of 201 MSMEs in Chinsali participated indicative of 99% participation rate. Questionnaires were administered randomly to participants, where data analysis was done through SPSS V26 presented by means of descriptive and inferential statistic. Th study revealed that most MSEMs have business income that is > ZMK 5000, and obtain both long- and short-term loans ranging from ZMK 5000 to < 40000. The study reveals a positive correlation between loan Range and Compliance (p=0.00, sig at 0.01), Business Income and Compliance (p= 0.00, sig at 0.01). The study recommends that MSMEs, should increase income through projective planning and effective management, they should also be improvement of financial education through capacity building meeting, to enhance business expansion and loan compliance. In addition to the above MSMEs should apply for loans that are attainable and fit their business models.

Keywords: Compliance, Empowerment, Financial literacy, profitability, CDF, CEEC.

Medium, Small, and Micro Enterprises (MSMEs) are an important factor to economic growth of any economy, this is so as they contribute significantly to job creation, poverty alleviation, and overall economic development. In spite of their importance, MSMEs face many challenges, which include limited access to finance, inadequate business management skills, and lack of formalization (Casey, et al., 2021). Realizing these challenges, the government of the Republic of Zambia has implemented various initiatives to support MSMEs, some of which include the Constituency Development Fund (CDF) and the Citizens Economic Empowerment Commission (CEEC) Loans (Citizens Economic Empowerment Commission, 2023), (Likando, et al., 2023) with both intended to provide financial support to grassroots businesses which fosters entrepreneurship across the country. Despite the availability of these initiatives which aim to support local businesses, through a revolving fund mechanism, there are significant concerns that have been raised with regards to loan compliance, little is unknown of the compliance status of MSMEs in Chinsali Zambia.

Many studies have been conducted on MSMEs in relations to Loans and their impact to Business performance Globally, Regionally and Locally, some of which includes (Kerimkulova, et al., 2021) in Ukraine, (Dominic, 2019), (James & William, 2018) both of Uganda. In Zambia studies by (Chilembo, 2021) (Saidi, 2024) and (Hapompwe, et al., 2021) have investigated loans’ impact to business. However, limited studies have been conducted pertaining to government support like CDF/CEEC, of the few includes; (Bango & Mugobo, 2023) in South Africa (Maunganidze, 2013) in Zimbabwe (Chibomba., 2013), (Likando, et al., 2023), , (Micheal & Chanda, 2021), (Phiri, 2016). According to the best of the authors’ knowledge, there is no study in Zambia that has been conducted to ascertain Constituency Development Funds (CDF) and Citizens Economic Empowerment Commission (CEEC) Loan Compliance by Medium Small and Micro Enterprises (MSMEs) in the context of Chinsali, consequently the present study will attempt to the seal the gap that has not been studied.

The Statement of the problem is that, despite the accessibility of CDF and CEEC loans which aim to improve economic activities, there have been reports by (Ministry of Local Government and Rural Development, 2022) and (Citizens Economic Empowerment Commission, 2023), which show that many micro-enterprises especially in rural districts, are facing adverse difficulties in loan compliance and utilization of funds. This lack of compliance has extremely weakened the effectiveness of these government initiatives in promoting sustained economic development. Additionally, little is known on how the two Government initiatives CEEC and CDF loans for MSEMs have contributed to business performance. Therefore, the study seeks to examine the factors which have contributed to CDF and CEEC loan compliance by MSMEs and the assessment on the impact of CDF and CEEC loans on business performance in the context of Chinsali District.

The study contributed to Sustainable Development Goal Number Eight (1) (No Poverty), 2 (Zero Hunger). The study found that SDGs 1 and 2 are have been accomplished through government initiatives of CEEC and CDF, which have supported SMEs, through boosting their business by provision of leverage for business continuity and going concern in line with Sustainable Development Theory, Through the two government initiatives the study has established that MSMEs business have been improved which has reduced poverty levels attaining SDG (1) No Poverty, also as the improvement of MSMEs business has increased investments, leading to employment creation which has aided the reduction in hunger, consequently contributing to SDG (2) Zero Hunger.

The parts of the study comprise of the following: Section One contains the introduction, Section two comprises review of literature, section three covers the theoretical and conceptual framework whereas Section four covers the research methods, with section Five and Six presenting the results and discussion of the research findings. To end, section eight concludes and suggests recommendations grounded on the discussions.

General overview of MSMEs In Zambia

Small, Medium and Micro enterprises (SMMES) are defined as a separate and distinct business entity, including co-operative enterprises and non-governmental organizations (NGOs), managed by either an individual owner or a group of individuals, (Bango & Mugobo, 2023).

In Zambia MSMEs are classified in different categories such as Micro Enterprises , these are business enterprise, who have an yearly turnover of One Million Kwacha (K1000,000.00), and is capable of Employing up to ten (10) persons (Ministry of Commerce, 2022); A small enterprise are businesses who have an annual turnover of between One Million and One Kwacha (K1,000,001) but not exceeding Ten Million Kwacha (K10,000,000), and are capable of employing between 11 and 50 employees (Ministry of Small and Medium Enterprice Development, 2023 ); A medium enterprise on the other hand is a businesses who have an annual turnover of between Ten Million and One Kwacha (K10, 000, 001.00) to Fifty Million Kwacha (K50, 000, 000.00), and who are capable of employing between 51 to 100 people (Ministry of Commerce, 2022).

Historical Overview of SME Development in Zambia

Post-Independence, the economy of Zambia was saturated by international investment largely in the mining industry. In 1965, the Government of Republic of Zambia initiated the Pioneer Industries Act of 1965, which was aimed at relief from Income Tax, with the objective of promoting import replacement in light industry (Ministry of Small and Medium Enterprice Development, 2023 ). As a result, during the period 1966 to 1972, the ownership form was changed from private to public sector proprietorship. The government thus made additional efforts to strengthen local entrepreneurs, with a measure of limiting local trade, transport, supplying of Government contracts and other building materials to citizens. However, these attractive efforts were unsuccessful because of inadequate entrepreneurial capacity for Locals (Zambians) (Ministry of Commerce, 2022). To curb this situation, the government of the Republic of Zambia passed the Small Industries Development (SID) Act, which resulted in the formation of Small Industries Development Organization (SIDO) in 1981, with the ultimate view of enhancing the effectiveness of the MSMEs involvement to the national economy (Zambia Development Agency, 2021). So as to support the Act (SIDA), provisions were included in the Fourth National Development Plan of 1989, which massively provided for infrastructure which promoted the operations of MSMEs, the massive promotion of access to credit by MSMEs with the development possibility and the improvement of production capacities of MSMEs so as to increase incomes, employment and consequently contribute to national development (Ministry of Small and Medium Enterprice Development, 2023 ). Nevertheless, the major shift of MSMEs in Zambia was in 1992 when the Government liberalized the Zambian economy and emphasized the development of private enterprise, which was massively reinforced in December 1994 by the formulation of the Commercial Trade and Industrial Policy in December 1994 (Ministry of Commerce, 2022).

Additionally, in 1996 the Government revoked the SID Act No. 18 of 1981 and substituted it with the Small Enterprises Development (SED) Act No. 29 of 1996. The act thus provided a number of inducements to spur the expansion and development of MSMES into feasible entities. Though, most of the inducements were not executed partially because there were no systems to support their implementation. Thus, the 1996 Small Enterprise Development Act, SIDO was converted into Small Enterprises Development Board (SEDB). As a result, the Small Enterprises Development Board (SEDB) was amongst the establishments that were merged to form the Zambia Development Agency (Ministry of Small and Medium Enterprice Development, 2023 ). Additionally, in the absence of a MSMED Policy, growth for the MSME landscape and synchronization of development intrusions continued to be a major challenge in the country. As a result, in 2009 the Government put in a place the MSMED Policy and its Implementation Plan. As such during the process of executing the Policy, new advances arose which have imposed reviewing the Policy. These changes included Rapid changes in ICT which brought about outstanding use of e-commerce platforms by MSMEs which improved ways of conducting business. Furthermore, the formation of the Africa Continental Free Trade Area (AfCTA), also meant the modern way of doing business as raising need of elimination of tariff and non-tariff barriers, so as to completely liberalize MSMEs and services which create competition to goods and services produced by MSMEs. Additionally, global shifts such as COVID-19, disrupted supply chains and caused in the closure of markets which meant that MSMEs where to come up with alternate methods of business distribution and trading (Common Market for Eastern and Southern Africa, 2020). As a result, these progresses have demanded for policy vicissitudes that have put MSMEs on a competitive level for both Africa and local markets.

Community Development Fund (CDF)

The Constituency Development Fund is intended at providing local authorities with discretionary financing that can be decided upon and utilized at the discretion of the communities under the auspices of the Council with the representation of the Member of Parliament (MP) and the Councilors within a particular constituency (Phiri, 2016).

The CDF in Zambia is a government initiative which is aimed at decentralizing resources for local development, enacted by an act of parliament (Government Republic of Zambia, 2018). It allows communities to prioritize and implement projects that address their needs, from infrastructure development to economic empowerment programs (Casey, et al., 2021). In the recent years there has been a significant rise in CDF allocation in the 2022 budget, with a further rise in 2023. Additionally in 2024 alone the budget increased CDF expenditure to K30.8 million Kwacha per constituency, the CDF apportionment for Small and Medium Enterprises (MSMEs), has also increased over the past years from 1.6 million kwacha previously to 25.7 million Kwacha per constituency in 2022, with a further increase of 28.3 million Kwacha in 2023; (Presidential Delivery Unit, 2024 ). The increase in SMEs fund allocation has enabled support to MSMEs investment through loans. However, despite the increase there has been major challenges in accessing these resources as of vast complexities in application procedures and inadequate awareness about the program. Additionally, local authorities are having challenges in ensuring that CDF loan beneficiaries comply with funding requirements and loan repayment , (Ministry of Local Government and Rural Development, 2022).

The Citizens’ Economic Empowerment Commissions

The Citizens’ Economic Empowerment Commission was established in accordance with section 4 (1) 4 of CEEC Act of 2006. Their main objective includes enabling and increasing the levels of citizen participation in all facets of the Zambian economy so as to improve their own lives (Phiri, 2016) . The preamble of the act states:

“The functions of the Commission shall be to promote the empowerment of citizens that are or have been marginalized or disadvantaged and whose access to economic resources and development capacity has been constrained due to various factors including race, sex, educational background, status and disability”

Targeted Citizens as a person who is historically marginalized or disadvantaged and whose access to economic resources and development capabilities have been constrained due to various factors including race, sex, educational background, status and disabilities.

The category of CEEC loans includes, Marketeer Booster Loan, which are interest free and vary between K500–K5,000 available to marketeers with viable businesses, Busulu Loans which vary between K5,000–K50,000 available for start-ups and existing enterprises, Fingerlings Production Plant, has available for K930,000 funding for a Fingerlings Production Plant (Citizen Economic Empowerment Commision, 2024). The government has made efforts in the nation disbursements of CEEC loans with the loan compliance rate standing at 71% as shown in the table 1 below.

Table 1 Cumulative status of Disbursement (August 2022- January 2024)

| Product | Number Funded | Amount Funded (K) |

| Marketeer Booster Loans | 74,630 | 158,899,88 |

| Busulu | 7,067 | 72,508,356 |

| Project Finance | 445 | 465, 040,999 |

| Trade Finance | 185 | 148,246,486 |

| Grand Total | 82,327 | 844,695,029 |

Source: (The CEEC Review, 2024).

Loan compliance by MSEMs in Zambia

The present level of loan compliance among micro-enterprise entrepreneurs in Zambia has been a challenging roadmap, (Musthusamy, 2022) which has reflected the challenges in the microfinance sector. A recent survey by (Mumba, 2019) show that many Micro, Small, and Medium Enterprises (MSMEs) in Zambia have difficulties in fully repaying their loans, with about 14% of MSMEs defaulting on their loan repayments, with higher default rates found in rural areas and informal sectors (Chilembo, 2021). The primary reasons for non-compliance comprise limited financial literacy, erratic cash flows, and challenges in market access. As such, many struggle to manage their finances effectively due to inadequate record-keeping and lack of financial management skills. With these factors, it has made it rather difficult for MSMEs to stay on track with loan repayments (Bango & Mugobo, 2023), (Dominic, 2019), (Hapompwe, et al., 2021) (Chilembo, 2021) and (Mumba, 2019).

The current level of loan compliance among micro-enterprise entrepreneurs varies from region to region, economy to economy, as evidenced by various studies (James & William, 2018), (Olusansenu, 2013), (Leseyio, 2014), (Chilembo, 2021), (Economic Association of Zambia, 2021), (Dominic, 2019), (Citizens Economic Empowerment Commission, 2023). In Zambia particularly Loan compliance is significantly high in rural areas and informal businesses, (Shah, 2012), (Mumba, 2019) which may be as a result of insufficient financial management skills, lack of structured record-keeping, misappropriation of loan funds, lack of business experience, external and internal factors (Duscha, 2009), (Hapompwe, et al., 2021), (Chilembo, 2021) (Likando, et al., 2023), (Mumba, 2019), (Saidi, 2024), and (Sichamba & Siwila, 2019 ). However, there are efforts being made to improve compliance through education support programs, capacity-building programs, better access to credit services and improved financial literacy, (Saidi, 2024). On the other hand, two comparative studies show that Loan compliance for private and state owned MSMEs is better (Chilembo, 2021) (Mumba, 2019) as opposed to Government related initiatives, (Citizens Economic Empowerment Commission, 2023).

Factors influencing compliance or non-compliance with loan conditions

Various scholars have studied, different factors that influence compliance and non-compliance of loans, among MSMEs of which they are reviewed below.

A study by (Saidi, 2024) found that the terms and conditions of credit such as interest rate, payment schedule, loan sum, collateral requirements, dues, and penalties for late payments or default, have a bearing on loan compliance as they have the capability of either enhancing compliance and or non-compliance. A study by (Mumba, 2019) shows that rigid terms and conditions of credit produces a high compliance rate as opposed to flexible terms and conditions of credit.

Most business in Africa operate in informal sectors (Africa Economic Outlook (AEO), 2021) as a result many do not have adequate Financial Literacy, a study by (Dominic, 2019) found that many micro-entrepreneurs lack basic financial management skills, which affects their capability of managing cash flows which impacts allocation of funds for loan repayments, Consequently the low level of financial literacy contributes to poor budgeting, planning, and record-keeping, thus making it difficult for businesses to meet their repayment obligations (Mumba, 2019).

Many businesses that operate in informal sectors are very much fought with irregular income streams, this is so as their revenues may be dependent on seasonal demand, market fluctuations, or other external factors like agricultural output, which can disrupt consistent loan repayment, (Maunganidze, 2013). As a result, this led to cash flow volatility, which has the impact of reducing cash flow thus limiting loan repayment thus triggering non-Loan compliance.

It is evident that Formalized businesses tend to have better compliance rates than informal businesses (James & William, 2018), (Leseyio, 2014), (Shah, 2012), (Saidi, 2024), the reason behind is that formal businesses have structured operations, maintain records, and have access to support systems, which makes them more compliant. On the other hand, informal businesses are unstructured and lack proper record management, this affects their loan compliance.

Lack of Capacity Building and Training equally impact loan compliance/ noncompliance, studies by (James & William, 2018), and (Mumba, 2019) found evidence to suggest that businesses that have undergone financial management training and capacity-building programs tend to be profitable, well-structured with viable investments and compliant to legal, statutory and loan requirements, in contrast to businesses which do not.

MSMEs may be affected by external factors beyond their control such as (Pandemics, Climate Change), economic downturns, pandemics (e.g., COVID-19). Climate-related events such as drought and floods can disrupt business operations, thus leading to loss of income. As a result these factors may weaken the level of compliance for MSMEs (Micheal & Chanda, 2021). Additionally, lack of collateral impacts loan compliance. Studies show that MSMEs that could provide collateral were more probable to repay loans because they have a stronger commitment to safeguarding their assets from been forfeited (Hapompwe, et al., 2021), (Leseyio, 2014), (Kerimkulova, et al., 2021) and (Mumba, 2019). On the other hand, unsecured loans (With no collateral) have a higher default rates, as the perceived consequences of non-repayment were lower (James & William, 2018), (Saidi, 2024).

Another factor which determines loan compliance/noncompliance is financial literacy. Some studies reveal that SME managers with a high level of financial literacy were more likely to comply with loan terms and conditions, as opposed to those without financial literacy. This is so because financial literacy influences the ability to manage cash flows, track expenses, and ensure timely repayments (Mumba, 2019).

Economic impact of Government support initiatives on the Growth and Sustainability of micro-Enterprises MSMEs

Globally, the support of the governments is considered to have a substantial impact on the performance of MSMEs,

(Africa Economic Outlook (AEO), 2021), government intervention by governments in MSMEs has been noted in China (Minghu, 2013), Ukraine (Kerimkulova, et al., 2021) Ghana, (Bank of Ghana, 2013), Malawi , (Campos, et al., 2019) South Africa (Bango & Mugobo, 2023) Zimbabwe (Maunganidze, 2013) in Uganda (James & William, 2018), in Nigeria (Olusansenu, 2013). In Zambia (Economic Association of Zambia, 2021), (Presidential Delivery Unit, 2024 ), (Ministry of Small and Medium Enterprice Development, 2023 ), (Citizen Economic Empowerment Commision, 2024), which have all yielded fruitful results in Job creation and economic sustainability. In Zambia particularly other government intervention is MSMEs such as training, tax relaxations, funding and allied business support facilitating, has supported SMEs to engage in business-level innovations, acquire resources necessary to execute the business ideas, increased MSMEs liquidity and business expansion, and promotion of innovativeness and creativity of MSMES (Phiri, 2016), (Likando, et al., 2023) (Bank of Zambia, 2022), (Economic Association of Zambia, 2021).

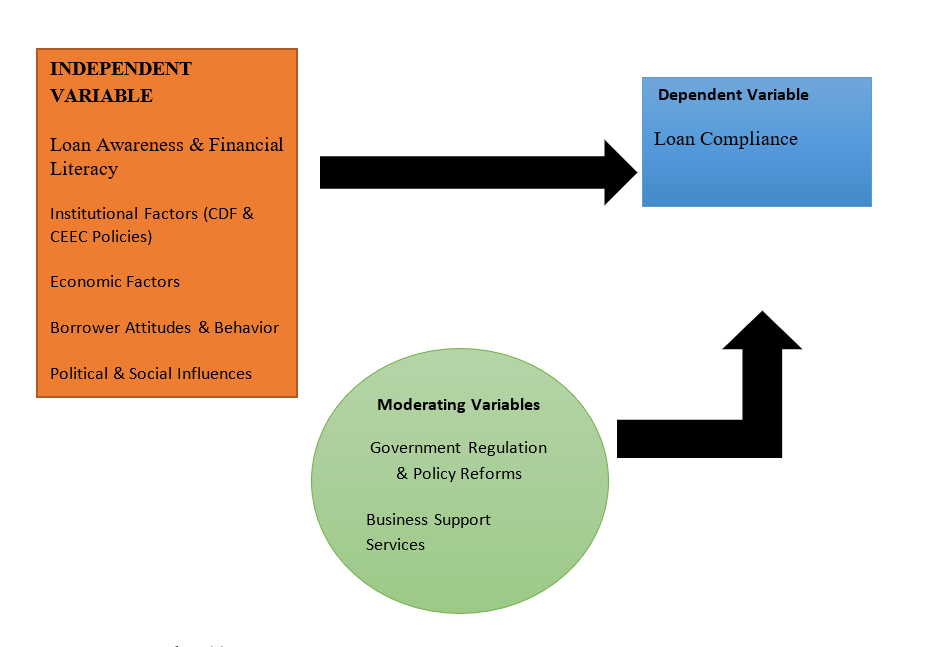

Conceptual And Theoretical Framework

Conceptual framework

Introduction to the Conceptual Framework

The conceptual framework of the study represents the understanding of the factors that influences loan compliance among MSMEs in Chinsali District in the context of Constituency Development Fund (CDF) and Citizens Economic Empowerment Commission (CEEC) loan programs. The conceptual framework constitutes of: Independent Variables, which includes Factors Affecting Compliance, such as Loan Awareness and Financial Literacy; Institutional Factors, which include polices that have been set up by CDF and CEEC policies; Economic Factors include Business Profitability and Revenue Stability; Market conditions that affect MSME growth; Borrower Attitudes & Behaviour, includes the awareness of loans as grants vs. Obligations; Risk aversion and readiness to comply; Political & Social Influences, which includes Political patronage and favouritism in loan allocation, together with Peer influence and cultural attitudes toward borrowing. Dependent Variables, comprises of Loan Compliance which is determined by timely repayment, partial repayment, default. Moderating Variables, include Government Regulation & Policy Reforms (Stronger enforcement mechanisms, legal actions for defaulters) and Business Support Services (Training, mentorship, market linkages)

Source Author (s) 2024

Figure 1 The Theoretical Framework

The study applied the following theories in the investigation on CDF and CEEC loan compliance by MSMEs

Principal-Agent Theory

The principle-Agent Theory was developed by Michael Jensen and William Meckling, in the 1970s. The theory adopts its roots from agency theory, it classically describes the relationship that may exist between funding institutions in this case CEEC, CDF as principals and MSMEs as agents (Jensen & Meckling, 1976). The theory is applicable in the current study because it describes that non-compliance of MSMEs may arise as a result of information asymmetry, where MSMEs do not fully disclose their financial standing despite been fully aware, as a result noncompliance (i.e., misuse funds or default) May be done intentionally. The weakness of this theory is that despite information asymmetry between the principal and agent, there is no moderating factor that is proposed to regulate information asymmetry between the two.

Public Choice Theory.

The Public Choice Theory was propounded by James M. Buchanan. The theory clearly analyses political processes through the lens of individual self-interest. The major argument of this theory is that politicians and bureaucrats are driven by their individual personal gains, as opposed to public good (Buchanan & Tullock, 1962). The theory is important in the study as it clearly examines how government programs such as CDF and CEEC function in a political environment (Mueller, 2003). The theory is applicable in the study as it typically scrutinizes on how political influence, preference, or poor oversight may lead to misallocation of funds or lack of enforcement of loan repayment policies. The weakness of the theory is that it only concentrates on political factors that may stimulate noncompliance and ignores that economic factors that contribute to non-compliance.

Pecking Order Theory (Financial Management)

The Pecking Order Theory is a theory of capital structure that was developed by Myers in 1984 (Myers & Majluf, 1984). The theory explains why businesses prefer internal financing over external options (Myers & Majluf, 1984). The theory suggests that, firms that first use retained earnings for financing, resort to debt if internal funds are insufficient. The theory is important to the study because it highlights that MSEMs been small in size may opt first for internal source of financing its business, because of lack of borrowing capacity, as such because of their size debt is considered least. The theory is applicable in the present study because it shows that noncompliance may result from MSMEs prioritizing other financial obligations over loan repayment. The weakness of the theory is that it discourages debt as a method of finance.

Institutional Theory

The Institutional Theory was propounded by Meyer and Rowan, which basically analyzes how organizations adapt to societal norms, with the objective of gaining legitimacy and enhance survival in their business environment (DiMaggio & Powell, 1983). The major emphasis of the theory is the adoption of formal structures in the organization that are not fundamentally effective but are seen as genuine by their environment, (North, 1990). The theory is important to the study because it explains how MSMEs’ behaviour is shaped by regulations, norms, and institutional structures. The theory is applicable to the present study because it demonstrates how weak enforcement mechanisms or lack of institutional trust may led to non-compliance of low loan repayment rates. The weakness of the theory is that it concentrates on institutional factors as the major cause of non-compliance it does not fully pin point, why some institutions do not oblige to institutional norms and ethics.

Behavioural Economics (Prospect Theory)

This is a theory that was propounded by Kahneman and Tversky, it is also known as Prospective Theory as it shows how people choose among substitutes that comprise risk and uncertainty (Barberis, 2013). The theory clearly demonstrates that people think in relation to expected utility as opposed to relative to reference point rather than absolute outcomes. The theory also assumes that people are loss averse as prefer equivalent gains as opposed to losses, as a result they are more eager to take risks to avoid a loss (Kahneman, 2011). The theory is important as it shows that decision-making on loan related issues is largely influenced by risk perception and biases. The Theory is applicable because it shows that MSMEs may underestimate loan repayment risks as a result of overconfidence or short-term thinking. The weakness of the theory is that it does not account for factors that contribute to variation of behaviours

Stakeholder Theory

The Stakeholder Theory was propounded by R. Edward Freeman. It evidently shows that the all stakeholders should be given equal treatment, (Donaldson & Preston, 1995), it also emphasis that the fruitiness of a company is on value delivery as such contribute to building the image of a business. In the context of the study the theory is important as it identifies numerous stakeholders (government, financial institutions, MSMEs, communities), who are all involved in CDF and CEEC. The Theory can be applied to the study as it scrutinizes how diverse interests affect compliance, it also shows how MSMEs view of government loans as grants rather than obligations.

Economic Development Theory

Economic Development Theory provides an all-inclusive framework for understanding the broader socio-economic context in which youth-owned businesses operate. The Economic theories that will be studied includes:

Modernization Theory of Economic Development

The proponent of Modernization Theory is Walt Whitman Rostow, who contended that societies progress through a linear order of stages, transitioning from traditional to modern economies (Rostow, 1960). In relation our present study, the theory is important because it shows how CDF/CEEC loan can trigger economic growth where societies evolve into modern economies through investment, education, and infrastructure development. The theory is important to the study because it shows how CDF and CEEC loans are expected to empower MSMEs through providing capital required for growth and modernization. The weakness of this theory in the study shows how poor training and lack of financial literacy may trigger noncompliance consequently limiting the modernization theory.

Dependency Theory of Economic Development

The proponent of the Dependency Theory is Andre Gunder Frank, who reasoned that, developing economies are largely reliant on external forces such as government spending (Frank, 1967), the theory assumes that poor institutional guidelines on government loan recovery MSMEs in Zambia may become reliant on government loans (CDF, CEEC), as opposed to developing sustainable financial strategies. As a consequence, if there is weak compliance loan programs may not achieve long-term economic empowerment, therefore forming a cycle of dependence.

Schumpeter’s Innovation Theory of Economic Development

The proponent of Schumpeter’s Innovation Theory of Economic Development is Joseph Alois Schumpeter, who coined the term creative destruction to define how innovations substitutes out-of-date systems, leading to both economic progress and structural transformation (Schumpeter, 1934). The major advocacy of this theory is that Economic growth is determined by entrepreneurs who modernise, create, take risks and penetrate new markets. The theory is applicable to the present study because it helps to emphasis how CDF and CEEC loans should inspire entrepreneurship and innovation amongst MSMEs. Additionally, Non-compliance is more probable to effect where businesses are not innovative , fail to grow, or struggle to compete in the market. On the other hand, compliance progresses where entrepreneurs use loans for innovation.

Endogenous Growth Economic Theory

The proponent of Endogenous Growth Theory is Paul Romer, the theory argues against neoclassical growth models by stressing that economic growth is driven by factors within the economy. The basic idea of the theory is that Economic development is fueled by human capital, knowledge, and technology investment, and not only external funding (Romer, 1986). The theory is applicable to the study because it argues that if MSMEs are trained skilled and competent, they are more probable to use loans effectively, thus become more compliant. Furthermore, Lack of business training and innovation could possibly cause mismanagement of loans and defaulting.

Sustainable Development Theory

The theory of sustainable development theory was propounded by different scholars, organizations and policymakers. The major ideal of this theory is that Economic growth must be inclusive, long-term, and environmentally sustainable (Brundtland, 1987). The theory is applicable to the present study because it stresses that small loans such as CDF and CEEC loans should not only boost short-term profits but also promote sustainable business models. Additionally, a high level of loan non-compliance might designate those businesses are failing to build pliability against economic shocks.

Research Type

The research used Likert scale questionnaire for data collection. Quantitative data was collected through physical methods, the researcher interacted with the participants.

Study area

The study was conducted in Chinsali District, located in the Muchinga Province of Zambia. The main aim of the study was to investigate Constituency Development Funds (CDF) and Citizens Economic Empowerment Commission (CEEC) Loan Compliance by Medium Small and Micro Enterprises (MSMEs). The map shows that Chinsali is a relatively rural and underdeveloped area, implying that MSMEs in this district, like in many other parts of Zambia, face considerable challenges related to access to finance, market opportunities, and business development.

Source https://rsisinternational.org/journals/ijriss/wp-content/uploads/2023/11/Figur-1-1.png

Target Population / Study Frame

The target population of the study were Micro Small and Medium (MSMEs) businesses in Chinsali who benefited from either CDF and or CEEC loans for the past two years and are in active business.

Research Design

The study used descriptive research design, with the objective of enriching the outcome of the study. Quantitative technique was applied.

Sampling Techniques

The research used the simple random sampling techniques to collect data. Who were drawn from the beneficiary list of CDF and or CEEC loans for the past two years To better get quality responses only MSMEs who have been in active business, and benefited from the loan program were targeted.

Sample Selection and Procedure

The Researcher used CDF and CEEC obtained from the two authorities Chinsali Council, and CEEC Chinsali office after which simple Random sampling was used.

Sample Size Estimation

According to CEEC in Chinsali there are about 256 beneficiaries and 150 CDF beneficiaries as at 2024, thus the population is 406, using the formula the population is

Data collection Instruments

The study used physical questionnaires that were randomly distributed to MSMEs in Chinsali

Data Collection Procedures

The study used simple Random sampling where CDF and CEEC were selected because they are the mediums used by the government to dispense loans to MSMEs, the data collection stage took a total of 56 days, out of the 201 participants representing 99% responded to the questionnaires.

Validity and Reliability Test

Cronbach Alpha test using SPSS V26 was used to determine the reliability of data, of which the approximate results showed a scale reliability coefficient of 0.647, and an average interim covariance of 0.352. The test indicates that Cronbach’s alpha coefficient composite score (survey) is reliable, and the chosen items of the study best describes the targeted concept.

Data Analysis

Primary data was gathered using questionnaires which were analyzed using IBM’s SPSS V26. The results were presented using descriptive and inferential statistics, presented in form of mean scores, percentages, graphs and illustrations, and non-parametric tests. Pretesting of 20 questionnaires was done.

The data presented comprises of information for the participants and a presentation of the findings. Table 1 Below presents the background characteristics of the participants that responded to the questionnaire. The table shows that the larger number of participants were between the age of 25-35 (33.3%, n=67). Further The table also shows that the majority of the participants were male (51.2%, n=103) with a variance of (2.4%, n=5) of which the most were married at the time of the study (65.7%, n=131). Lastly, the table shows that most participants (41.3%, n=83) accomplished at least primary education.

Table 1

| AGE | F(n) | % |

| <25 | 21 | 10.4 |

| 25 – 35 | 67 | 33.3 |

| 36- 45 | 50 | 24.9 |

| >46 | 63 | 31.3 |

| >39 | 10 | 3.3 |

| GENDER | ||

| Male | 103 | 51.2 |

| Female | 98 | 48.8 |

| MARITAL STATUS | ||

| Single | 38 | 18.9 |

| Married | 131 | 65.7 |

| Divorced | 12 | 6.0 |

| Widowed | 15 | 7.5 |

| Separated | 05 | 2.5 |

| LEVEL OF EDUCATION | ||

| No Education Level | 16 | 8.0 |

| Primary Education | 83 | 41.3 |

| Senior Secondary School | 68 | 33.8 |

| Certificate/Diploma | 26 | 12.6 |

| Degree | 01 | 0.5 |

| Total | 201 | 100 |

Business Profile of MSMEs

The study also collected information regarding business profiles of MSMEs that were sampled in the present study. Included are the types of business that the SMEs participate in, the size of the business, the nature of the business, and the income of the business. According to table 2 the majority of the sampled participants are Sole traders (84.6%, n= 170), with the most been Micro, Small and Medium Enterprise (MSMEs) sized business (99.0%, n=199). Whereas the majority participated in Retail Trade (57.2%, n= 115). Furthermore, most sampled participants have a monthly income range of > ZMK 5000 (70.6%, n= 154).

Table 2

| TYPE OF BUSINESS | F(n) | % |

| Sole Trader | 170 | 84.6 |

| Cooperative | 16 | 8.0 |

| Partnership | 6 | 3.0 |

| Company | 9 | 4.5 |

| BUSINESS SIZE | 23 | 7.7 |

| Micro MSMEs | 199 | 99.0 |

| Medium MSMEs | 2 | 1.0 |

| NATURE OF BUSINESS | ||

| Retail Trade | 115 | 57.2 |

| Education | 1 | 0.5 |

| Manufacturing | 2 | 1.0 |

| Catering | 5 | 2.5 |

| Service | 23 | 11.4 |

| Construction | 5 | 2.5 |

| Transport | 11 | 5.5 |

| Agriculture | 32 | 15.9 |

| ICT | 7 | 3.5 |

| BUSINESS INCOME | ||

| >ZMK5000 | 154 | 70.6 |

| ZMK 50001-10000 | 44 | 21.9 |

| < ZMK 10000 | 3 | 1.5 |

Loan Description

To determine CDF and CEEC Loan Compliance by Medium Small and Micro, the present study collected information in relation to loan description, which included: Loan beneficiary, Loan type, Loan Range, Loan tenure and Loan purpose and where the loan information was obtained from. According to table 3, all the participants were loan beneficiaries of either CDF or CEEC, (100%, n=201), of which CDF participants were (49.9%, n= 100) and CEEC (50.1% n=101), with the majority of the participants obtaining loans of less that ZMK 5000 (36.5%, n= 76), accompanied by loan range of 40000 and above (35.2% n=71). The loans obtained were either short or long term less than 1 year (44.8, n=90) and between 2-5 Years (53.7, n=108). Loans were obtained for various reasons but the majority obtained loans for either starting up a new business (40.8, n=82) or expanding already existing business (45.8%, n=45.8). It was also found that information on loans was obtained through various mediums. However, the majority was obtained through Radio (96, n=47.8) and social media (61, n=30.3).

Table 3

| LOAN BENEFICIARY | F(n) | % |

| Yes | 100 | 100 |

| LOAN TYPE | 16 | 8.0 |

| CDF | 100 | 49.9 |

| CEEC | 101 | 50.1 |

| LOAN RANGE | 23 | 7.7 |

| >ZMK 5000 | 76 | 36.5 |

| ZMK 5001-20000 | 29 | 14.4 |

| ZMK 20001- 40000 | 28 | 13.9 |

| <ZMK, 40000 | 71 | 35.2 |

| LOAN TENURE | 1 | 0.5 |

| Less than 1 Year | 90 | 44.8 |

| 2-5 years | 108 | 53.7 |

| LOAN PURPOSE | 23 | 11.4 |

| Starting a new business | 82 | 40.8 |

| Expanding existing business | 92 | 45.8 |

| Funding of Fixed Assets | 16 | 8.0 |

| Funding fixed asset of a new business | 11 | 5.5 |

| LOAN INFORMATION | ||

| TV | 16 | 8.0 |

| Radio | 96 | 47.8 |

| Friends | 4 | 2.0 |

| Social Media | 61 | 30.3 |

| Church Announcement | 19 | 9.5 |

| Total | 201 | 100 |

Level Of Compliance With Cdf And Ceec Loan Requirements By Micro-Entrepreneurs.

To determine Loan Compliance of CDF and CEEC loan by MSEMs, the present study collected data in relation to Level of compliance with CDF and CEEC loan requirements by Micro-Entrepreneurs, which included Compliance Loan with the terms and conditions; Maintenance of books, record-keeping, budgeting etc. Complications of Loan Repayment; and Loan Utilization for the Intended Purpose.

According to table 3, comparison of the mean mode and median with regards to Compliance Loan with the terms and conditions, the findings disagree that most loan beneficiaries do not comply with loan terms and conditions. The comparison of the mean mode and median disagree that most loan beneficiaries do not maintain of books, record keeping and budgeting. The comparison of the mean mode and median with regards to Complications of Loan Repayment disagree that there are no complications with CDF and CEEC loan Repayments. The comparison of the mean mode and median with Regular Cash flow in Businesses, finds that the majority of the businesses in Chinsali do not have regular cash flow streams. The comparison between mode, mean and median, suggest that most participants are unsure if loan utilization is done for the intended purpose.

The comparison between mode, mean and median, suggests that most participants Disagree that CDF/CEEC loans are not easily accessible.

Table 4

| Variable | Median statistic | Mode

Statistics |

Mean

Statistic |

Std. Deviation

Statistic |

Remarks |

| Adherence to loan repayments |

3.35 |

4 |

4 |

0.980 |

The median, mode mean Standard Deviation “DISAGREES” That there is no compliance to loan repayments. |

| Maintenance of books record-keeping, budgeting etc |

3.09 |

4 |

4 |

0.967 |

The median, mode mean and standard deviation “Disagree”. That there is no maintenance of books |

| Complications of Loan Repayment |

3.22 |

4 |

4 |

0.75 |

The median, mode and standard “DISAGREES” that CDF and CEEC loans are not complicated |

| Regular Cash flow in Businesses |

3 |

4 |

4 |

0.86 |

The median, mode and standard “DISAGREES” that there no regular cash flow in the business |

| Loan Utilization for the Intended Purpose |

3.01 |

2 |

3 |

0.69 |

The median, mean and standard deviation Suggests that most participants are not sure if there is utilization of loan for intended purpose |

Factors Influencing Compliance Or Non-Compliance With Loan Conditions.

To determine factors that influence compliance and non-compliance with loan conditions, the present study collected data in relation to factors that influence compliance and non-compliance with loan conditions, which included challenges in loan repayment, Loan Repayment impact on cash flow, external factors’ impact on loan Repayment, fairness of loan repayment process, attendance of capacity building workshops arranged by CDF or CEEC, and penalties in relation to penalties of non-adherence.

According to table 4, comparison of the mean mode and median with regards to challenges in Loan Repayment; the findings suggest that, the majority of the participants are having challenges in loan repayment. The comparison of the mean mode and median with regards to whether loan repayment impacts cash flow, it was found that the most participants agree that loan repayment impacts cash flow. The comparison of the mean mode and median with regards to external factors’ impact on loan repayment, it suggests that most participants indicate that external factors have an impact on loan repayment. The comparison between mode, mean and median on fairness of loan repayment process, it was found that there is fairness on loan repayment process of CDF and CEEC. The comparison between mode, mean and median, attendance of capacity building meeting finds that most participants do not attend capacity building meetings. The comparison between mode, mean and median on Penalties for non-adhering to loan repayment, finds that there are no stiff penalties that are enforced for non-Compliance.

Table 5

| Variable | Median statistic | Mode

Statistics |

Mean

Statistic |

Std. Deviation

Statistic |

Remarks |

| Challenges in Loan Repayment | 3.14

|

4 | 4 | 0.990 | The median, mode mean Standard Deviation “AGREE” That there that facing challenges in loan repayment. |

| Loan repayment impact on cash flow | 3.19 | 2 | 2 | 0.967 | The median, mode mean and standard deviation “Agree”. That Loan repayments impact cash flow. |

| External factors impact on Loan Repayment | 3.45 | 2.67 | 2.96 | 0.878 | The median, mode and standard “AGREES” that External factors impact loan repayment. |

| Fairness of Loan Repayment Process | 3.58 | 4 | 4.00 | 0.835 | The median, mode and standard “NOT SURE”. If there is fairness loan repayment process |

| Attendance of Capacity building workshops arranged by CDF or CEEC | 3.35 | 4 | 4 | 0.96 | The median, mean and standard deviation Suggests “DISAGREE” that they do not attend capacity building workshops arranged by CDF or CEEC |

| Penalties for non-adhering of loan repayment | 3.42 | 4 | 4 | 1.029 | The median, mean and standard deviation Suggests “DISAGREE” There are no penalties for non-adherence of loan repayment. |

The Economic impact of CDF and CEEC loans on the growth and sustainability of micro-enterprises.

According to table 5, comparison of the mean mode and median with regards to CDF/CEEC loan’s contribution to business progression, the findings agree that CDF/CEEC loans contribute to business progression. A comparison of the mean mode and median with regards to CDF/CEEC enhancing Job creation. The findings agree that CDF/CEEC loans contribute to Job creation. A comparison of the mean mode and median with regards to loans have a positive effect on financial stability in the short run, the findings “AGREE” that CDF/CEEC loans have a positive effect on financial stability in the short run. A comparison of the mean mode and median with regards to loans enabling the opening up branches in new markets, the mode median and Standard deviation agree that CDF/CEEC loans have enabled opening of new markets. A comparison of the mean, standard deviation suggest that CDF/CEEC loans have enabled the adoption of new technologies

Table 6 shows the Kendall Tau’s Correlation test, which tests both the Null and Alternative hypothesis from various variables as discussed below.

| Variable | Median statistic | Mode

Statistics |

Mean

Statistic |

Std. Deviation

Statistic |

Remarks |

| Contribution of Loans to Business Progression | 3.24

|

2 | 1 | 0.955 | The median, mode mean Standard Deviation Agree that CDF/CEEC loans contribute to business progression. |

| Creation of Employment because of loans | 3.25 | 2.99 | 2.10 | 0.71 | The median, mode mean and standard deviation “Agree” that CDF/CEEC loans have created employment |

| Loan’s positive effect on financial stability business in the short and long run | 3.48 | 2.65 | 2 | 0.883 | The median, mode and standard “AGREES” that CDF/CEEC loans have a positive effect on financial stability in the short run |

| Loan enabled the opening up branches in new markets | 3.62 | 4 | 4.00 | 0.796 | The median, mode and standard Disagree that CDF/CEEC have not enabled the opening if new branches. |

| Loan enabled the Adoption of new technologies or processes | 2.49 | 2 | 2 | 0.96 | The median, mean and standard deviation Suggests “Agree” That CDF/CEEC loans have enabled the adoption of new technologies. |

Kendall Tau’s Correlation Test

H1 test between compliance with CDF and CEEC loan requirements compliance and loan Range tested p-value = 0.00 < 0.001, less than the p value where the result is statistically significant at the 0.01 level. Therefore, the null hypothesis is accepted meaning that there is a significant positive relationship between Loan Range and compliance.

H2 test between level of compliance with CDF and CEEC loan requirements and loan tenure tested a p-value of 0.00 < 0.001, less than the p Value where the result is statistically significant at the 0.01 level. Therefore, null hypothesis is accepted meaning there is a positive significant relationship between loan tenure and compliance.

H3 test between compliance with CDF and CEEC loan requirements and Business Nature tested p-value = 0.624 > 0.001, more than the p Value where the result is statistically significant at the 0.01 level. Therefore, null hypothesis is rejected meaning there is no significant relationship between loan compliance and business income

H4 test between factors influencing loan compliance or non-compliance and nature of Business, 0.151 > 0.001, more than the p Value where the result is statistically significant at the 0.01 level. Therefore, null hypothesis is rejected meaning there is no significant relationship between factors influencing loan compliance or non-compliance and nature of business.

H5 test between factors influencing compliance or non-compliance with loan conditions and marital status which found a p-value of 0.256 > 0.005, greater than the p Value where the result is statistically significant at the 0.05 level. Therefore, the null hypothesis is rejected meaning there is no negative relationship between factors influencing compliance or non-compliance with loan conditions and marital status.

H6 test between factors influencing compliance or non-compliance with loan conditions and Business Income which tested a p-value of 0.05 < 0.05, equal to the p Value where the result is statistically significant at the 0.05 level. Therefore, the null hypothesis is accepted meaning there is a significant relationship between factors influencing compliance or non-compliance with loan conditions and Business Income

H7 test between factors influencing compliance or non-compliance with loan conditions and Business Size which tested a p-value= .102 > 0.005, more than the p Value where the result is statistically significant at the 0.05 level. So, the null hypothesis is rejected meaning there is no significant relationship factors influencing compliance or non-compliance with loan conditions and Business size.

H8 test between factors influencing compliance or non-compliance with loan conditions and maintaining of books for record keeping, budgeting etc. tested a p-value of 0.000 > 0.001, less than the p Value where the result is statistically significant at the 0.01 level. Thus, null the hypothesis is accepted meaning there is a significant relationship between factors influencing compliance or non-compliance with loan conditions and maintenance of books, record keeping and budgeting.

H9 test between factors influencing compliance or non-compliance with loan conditions and Business type which found a p-value of .677 > 0.005, more than the p Value where the result is statistically significant at the 0.05 level. Therefore, null hypothesis is rejected meaning there is no significant relationship factors influencing compliance or non-compliance with loan conditions and Business type

H9, test between Business Type and Loan enabled the Adoption of new technologies or processes, found a p-Value= 0.102 > 0.05, more than the p Value where the result is statistically significant at the 0.05 level. Therefore, null hypothesis is rejected meaning there is no significant relationship between, Business Type and Loan enabled the Adoption of new technologies or processes.

H10 test between penalties for non-adherence of loan repayment and compliance of loan with terms and condition, found a p-value = .010 > 0.005, more than the p Value where the result is statistically significant at the 0.05 level. Therefore, null hypothesis is rejected meaning there is no significant relationship between penalties for non-adherence of loan repayment and compliance of loan with terms and condition.

H11 test between compliance of loan with terms and condition, and Age which found a p-value = .003 < 0.005, less than the p Value where the result is statistically significant at the 0.05 level. Hence, the null hypothesis is accepted meaning there is a positive significant relationship between compliance of loan with terms and condition, and Age.

HO12– test between Compliance Loan with the terms and conditions and financial literate of Loan Beneficiaries found a p-value = .000 < 0.005, less than the p Value where the result is statistically significant at the 0.05 level. Therefore, the null hypothesis is accepted meaning there is a positive significant relationship between compliance of loan with terms and financial literacy.

HO13 test between Compliance Loan with the terms and conditions and External factors impact on Loan Repayment found a p-value = .000 < 0.005, less than the p Value where the result is statistically significant at the 0.05 level. Therefore, the null hypothesis is accepted meaning there is a positive significant relationship between compliance of loan with terms and external factor’s impact on loan repayment.

HO14– Compliance Loan with the terms and Attendance of Capacity building workshops arranged by CDF or CEEC found a P= 046 < 0.05, less than the p Value where the result is statistically significant at the 0.05 level. So, the null hypothesis is accepted meaning there is a significant relationship between compliance of loan with terms and highest level of Education.

Table 7 Pearson- Correlation Test

| Variables Correlated | Correlation Coefficient | Sig (2 Tailed) | Significate at | Comment |

| HO1 – Compliance and Loan Range | -.057 | 0.00 | 0.01 | significant accept null hypothesis. |

| HO2 – Compliance and Loan Tenure | -0.668 | 0.00 | 0.01 | Significant accept null hypothesis. |

| HO3 – Compliance and Business Income | 0.30 | 0.624 | .0 5 | Insignificant reject alternative null hypothesis. |

| HO4– Factors and Nature of Business | 0.82 | 0.151 | .05 | insignificant Reject alternative null hypothesis. |

| HO5 – Factors and Marital status | 0.67 | 0.256 | .05 | Insignificant reject alternative null hypothesis. |

| HO6- Factor and Business Income | 0.42 | 0.050 | .005 | insignificant reject alternative null hypothesis. |

| HO7– Factor and Business Size | 0.101 | .102 | 0.05 | insignificant reject alternative null hypothesis. |

| HO8– Factors and Maintenance of books record-keeping, budgeting etc | 0.721 | 0.00 | .010 | Significant accept null hypothesis. |

| HO9– Business Type and Loan enabled the Adoption of new technologies or processes | -0.027 | 0.677 | -0.05 | insignificant reject null hypothesis. |

| HO10- Penalties for non-adhering of loan repayment and Compliance Loan with the terms and conditions | -0.167 | 0.10 | 0.05 | insignificant reject null hypothesis |

| HO11– Age and Compliance to Loan with the terms and conditions | -0.187 | 0.03 | 0.05 | Significant accept null hypothesis |

| HO12– Compliance Loan with the terms and conditions and financial literate of Loan Beneficiaries | 0.2209 | 0.00 | 0.01 | Significant accept null hypothesis. |

| HO13– Compliance Loan with the terms and conditions and External factors impact on Loan Repayment | 0.413 | 0.00 | 0.01 | Significant accept null hypothesis. |

| HO14– Compliance Loan with the terms and Attendance of Capacity building workshops arranged by CDF or CEEC | -0.144 | 0.046 | 0.05 | Significant accept null hypothesis |

The study constituted of a gender balanced pool, despite males been marginally more by 2.4%. The balance in gender permitted the study to have a more diverse perspective, which had a broader range of ideas and reduced biasness. Likewise, the gender (Increased number of women) shows that the Government of the Republic of Zambia is making frantic efforts to promote and support women empowerment, as stipulated by (Citizens Economic Empowerment Commission, 2023), and (Ministry of Local Government and Rural Development, 2022).

The Study constituted of a mix of age, spanning from below the age of 21 to above 63 years. This diverse age group allowed creativity and innovation, fully informed by a rich variety of standpoints. However, the findings show that the majority of the participants in the present study were youths, suggesting that Chinsali has a number of youths full of vigor and working towards economic development. Additionally, the findings also show that most youths are empowered with capital as well, also indicating the commitment of the Government of the Republic of Zambia in promoting youth development in the MSMEs sector, a factor largely emphasized (Citizens Economic Empowerment Commission, 2023)

The study also constituted of different marital status of the participants, which included, single, married, divorced, widowed and separated, the blend in marital status is important it somewhat translates the motive of running business as seen from the results the majority are single a commonly known factor that single (unmarried) are associated with youths, thus supporting solidifying the narrative that most MSMEs in Chinsali are youths.

The results also show that the majority of MSMEs in Chinsali are, moderately educated, suggesting that most MSMEs in Chinsali may possess basic essential skills for effective business management, which allows them to have accesses to capital, and sustaining of long-term growth.

Business Profile Of Msmes

The study found that the majority of business that benefited from CDF/CEEC loans are sole traders (Single owned) a common type of business in many parts of Africa (Bango & Mugobo, 2023), (Africa Economic Outlook (AEO), 2021). The study additionally found that the majority of MSMEs beneficiaries are Micro SMEs. The findings are justifiable because CDF and CEEC aims to uplift Micro Business at all levels (Citizens Economic Empowerment Commission, 2023), (Ministry of Local Government and Rural Development, 2022) these government programs have worked successfully in reaching a large number of beneficiaries, as they are precisely designed to meet the needs of small-scale entrepreneurs, in traditional set up who find it difficult and impossible in accessing traditional financing (Ministry of Local Government and Rural Development, 2022). Chinsali as alluded, is a typical rural place so CDF and CEEC, an impression that the two program, have reached rural or marginalized, therefore enhancing economic development, and supporting the theory of Sustainable Development.

The study constituted of a number of businesses which comprised of Retail Trading business, Education, Manufacturing, Catering, Service business, Construction, Transport and Logistics, Agriculture and ICT Business, with the most been Retail Trade, these results are justifiable because the majority of business in Zambia deal in retail trade, as evidenced by (Economic Association of Zambia, 2021). Moreover, a blended nature of businesses enabled that there is a more diverse view point on CDF/ CEEC loan compliance.

The findings suggest that Chinsali is not so economically active as the majority of MSMEs generate monthly business income of less than ZMK 5000, different from studies conducted in Lusaka (Chilembo, 2021), (Hapompwe, et al., 2021) and (Likando, et al., 2023) in Kafue who the majority of MSMES have an income before tax of more than ZMK 6000. The result implies that MSMEs in Chinsali have limited income and may struggle to manage loan repayment, because of lack of liquidity desirable enough to make consistent loan payments.

Loan Description

The study found that all the MSMEs that participated in the study are loan beneficiaries, or have benefited from either CDF or CEEC loans, which is in line with the Sustainable Development Theory. The findings are justifiable because the majority of businesses in Zambia have benefited significantly from CDF and CEEC loans, (Bank of Zambia, 2022), (Citizens Economic Empowerment Commission, 2023), (Casey, et al., 2021), alluding to their affordability accessibility financing options, because of their low-interest rates, with emphasis been on local economic development, (Phiri, 2016) (Casey, et al., 2021) (Citizens Economic Empowerment Commission, 2023).

The study found that MSMEs in Chinsali have obtained CDF/CEEC loans of different amounts spanning from the range of ZMK 5000 to above ZMK 40000, consistent with the findings of (Micheal & Chanda, 2021) (Likando, et al., 2023), (Chilembo, 2021) and (Mumba, 2019), implying that CDF/CEEC loan procedure policy allows MSMEs to obtain both short- and long-term loans, which assist MSMEs with business liquidity. The study further found that MSMEs in Chinsali have obtained either short term loan payment tenure (less than a Year) and or long-term payment (2-5 Years), a sign of how flexible CDF/CEEC loans are. The loan amount and tenure are consistent with policy documents of (Ministry of Local Government and Rural Development, 2022), (Ministry of Small and Medium Enterprise Development, 2022).

The findings have highlighted that CDF/CEEC loans are been utilized in different ways which includes, starting up new businesses, expanding existing businesses, funding of fixed assets of existing businesses, and funding fixed assets of a new businesses. The findings are consistent with those of (Likando, et al., 2023), (Phiri, 2016), (Hapompwe, et al., 2021), (Mumba, 2019), (Saidi, 2024). Despite the utilization of loans, a lot is worrying because the majority participants obtain loans for business startup as opposed to investment in consistent with a study by (Musthusamy, 2022), who found an insignificant relationship between loans and business set up, implying that business that acquire loans for set up are normally not loan compliant. It was also found that there is so much sensitization on loan accessibility and utilization through different mediums such as TV, Radio, word of mouth (friends), social media, and gatherings such as church programs, showing how the government has collaborated with stakeholders to enforce CDF/CEEC loans in line with the stakeholder theory.

Compliance With Cdf And Ceec Loan Requirements By Micro-Entrepreneurs In Chinsali.

The findings through the mean have shown that the majority of CDF and CEEC do not adhere to loan repayments, an indication that they are not fully compliant with loan terms and conditions, consistent with the previous studies by (Mumba, 2019).The plausible reason behind non-adherence to loan repayments may be because of different factors such as financial literacy gaps, mismanagement of funds, economic challenges, poor institutional framework on loan recovery, lack of monitoring and political interference, which may lead to misallocation of funds or lack of enforcement of loan repayment policies, as detailed by the public choice theory.

The study further found that the majority of MSMEs in Chinsali do not maintain proper books of accounts, a situation which is prevalent not on in Chinsali but other localities as well (Likando, et al., 2023), (Phiri, 2016), (Mumba, 2019), (Bango & Mugobo, 2023) (Maunganidze, 2013). The findings are of great concern because they suggest that MSMEs in Chinsali do not adhere to globally recognized standards and principles, such as Generally accepted accounting principles (GAAP), International Financial Reporting standards (IFRS), Local Accounting Standards (ZiCA), and Tax Regulations. The implication of the findings are that MSMEs in Chinsali do not recognize measurement of financial elements such as revenue, expenses, assets, and liabilities, they do not adhere to the principal requirements of financial statement presentation and disclosures, and there is little or no emphasis on fair value and transparency, which may have a possibility of impacting loan compliance.

The findings revealed that, loans offered by CDF/CEEC are not complicated but are rather simple and flexible, which is particularly true because CDF/CEEC loans are meant to serve citizens with affordable financing options as stipulated by (Ministry of Local Government and Rural Development, 2022), (Citizens Economic Empowerment Commission, 2023), (Presidential Delivery Unit, 2024 ).

The findings have revealed that most MSMEs in Chinsali district do not have regular cash flow. The findings are inconsistent with the findings in different localities (Chilembo, 2021), (Hapompwe, et al., 2021), (Mumba, 2019) and (Dominic, 2019). The implication of the findings are that most MSMEs in Chinsali have irregular cash flow which may have negative impact to meeting business loan repayment obligations, therefore complicating financial planning, which increases the risk of loan defaults and non-compliance.

The findings have further found that MSMEs in Chinsali have not fairly used CDF and CEEC loans for the intended purpose similar to findings of (Phiri, 2016), (Mumba, 2019) and (Dominic, 2019), The implication of the findings are that , not using loan for its intended purpose or according to the business plan significantly impacts loan compliance, as the diversion of loan use for intended purpose causes financial mismanagement (Linda Tucci, 2020) which can result into loan defaults, noncompliance and impede business’s growth.

Factors Influencing Compliance With Cdf/Ceec Loan Conditions

The study found that the majority of participants are facing Challenges in Loan Repayment, a comparative analysis has shown that CDF loan beneficiaries have high levels of non-compliance as compared to CEEC, mainly be because CDF functions in a more political environment which may be marred in Political influence, preference, or poor oversight which may lead to misallocation of funds or lack of enforcement of loan repayment policies as supported by the public Choice theory. On the other hand, as noted by Institutional Theory CEEC may have a robust loan design and consistent monitoring, (Phiri, 2016).

The findings have further indicated that MSMEs are facing major challenges in loan repayments which may be alluded to literacy gaps, mismanagement of funds, economic challenges, lack of experience, poor loan utilization, poor financial management, misappreciation, seasonal income variability, external economic factors, and weak business models, which are shared findings with (Mumba, 2019).

The study also revealed that loan repayments has a bearing on cash flow, consistent with the findings of (Dominic, 2019), (James & William, 2018), (Musthusamy, 2022) and (Mumba, 2019)

these results are sensible because when a business takes out a loan, it assumes the responsibility of repaying that debt, which involves regular payments in specified period, where both loan and interest should be paid (Linda Tucci, 2020). This means that the regular cash outflows reduce the cash available for other purposes, as a consequence other MSMEs may opt not to be compliant with loan repayments.

The findings further reveal that, loan repayment are impacted by external factors such as market conditions, economic shocks, climate change etc. The findings are consistent with (Dominic, 2019), (James & William, 2018), (Musthusamy, 2022) (Mumba, 2019), and (Saidi, 2024). The findings are conceivable as loan repayments are significantly affected by external factors, which includes market conditions, economic shocks, and climate change, in Zambia particularly where the country has been predominantly hit by adverse market conditions, such as inflation spikes, and currency devaluation (Economic Association of Zambia, 2021), which has reduced customer expenditure consequently reducing revenue of MSMEs thus decreasing cash flow available to cover loan repayments, which has resulted in MSMEs finding it difficult to repay CDF/CEEC. In addition, Zambia is still experiencing adverse climate change (Detelinova, et al., 2023 ), which has affected a lot of MSMEs, considering that most business in Zambia are directly dependent on natural resources or weather patterns. Therefore, extreme weather events, shifts in seasons, and changing agricultural conditions have disrupted business operations which have caused severe economic losses, therefore incapacitating the capability of loan repayment.

Despite the study finding signs of non-adherence to loan repayments, the study has revealed that both CDF and CEEC loans have a fair loan process, as stipulated by (Ministry of Small and Medium Enterprise Development, 2022), (Ministry of Local Government and Rural Development, 2022). The fair loan process includes good tenure of loan, favorable interest rates , flexible payment schedule (Ministry of Small and Medium Enterprise Development, 2022) and (Ministry of Local Government and Rural Development, 2022).

Non adherence of loan repayment may also be attributed to non-attendance of capacity building meetings as found in the study, this implies that MSMEs in Chinsali are not equipped with proper training on loan utilization, a clear justification as to why loan beneficiaries struggle with financial management, loan repayment, and business growth. In addition, it has been found that, there are no penalties that are imposed for non-compliance, a reasonable explanation to the hesitance of loan compliance by CDF/CEEC beneficiaries.

Economic Impact Of Cdf And Ceec Loans On The Growth And Sustainability Of Micro-Enterprises In Chinsali

The study has revealed that CDF/CEEC loans has contributed to progression of MSMEs, which is necessitated by the provision of affordable access to capital, thereby assisting business expansion, and promoting financial inclusion, consistent with the findings of (Hapompwe & Zyambo, 2020), (Likando, et al., 2023) and (Phiri, 2016), which has thus directly enabled MSMEs to effectively diversify, therefore contributing to both local and national economic development (Casey, et al., 2021). As evidenced by the finding CDF/CEEC loans have enabled the creation of employment in Chinsali similar to the findings of (Micheal & Chanda, 2021). The findings are justifiable because as businesses expands more human resource is required to help manage the business operations (Kerimkulova, et al., 2021). CDF/CEEC loans have also contributed to the positive effect on financial stability and business growth in the short ran, a more common situation when new liquidity is introduced in a business (Linda Tucci, 2020), (Mumba, 2019), this is so because CDF and CEEC loans have accorded the chance for MSMEs to diversify to other sectors such as agriculture, retail, manufacturing, and services, therefore enabling financial stability.

However, the study has found that most businesses in Chinsali have not opened new branches in new markets, inconsistent with the findings of (Micheal & Chanda, 2021), and (Likando, et al., 2023). The constructive explanation that can be alluded to, is that most businesses that have benefited from CDF/CEEC loans are Micro or small with small amounts, as a result such business size in Zambia are unable to diversify, introduce new products, expand their market reach, or improve existing services, (Shah, 2012).

On the other hand, similar to Sustainable development theory, CDF/CEEC loans have enabled the adoption of new technologies or processes, similar to the study by (Citizen Economic Empowerment Commision, 2024), (Likando, et al., 2023). The findings are justifiable because loans from CDF and CEEC provide businesses with the necessary resources to invest in new technologies and innovative practices, considering the fact the government has put more emphasis on sustainable practices such as green technologies, energy efficiency, and environmentally-friendly products, (Detelinova, et al., 2023 ). This has enabled the capability of improving market appeal, attracting new customers, thus contributing to business growth and long term success.

Inferential Statistics.

Kendall’s Tau Correlation test found strong evidence to suggest that there is a significant relationship between compliance with CDF and CEEC loan requirements and loan range, this relationship refers to how the size of a loan (loan amount) might influence the ability or likelihood of the borrower to be compliant. As such, the test adequately correlates with the borrower’s behavior, repayment schedules, and the financial health of borrowers. Thus, in line with the Behavior theory, the test suggests that SME’s behavior of loan repayment is dependent on the amount obtained (Loan Range/tenure). The relationship is plausible because larger loans, normally have a higher repayment amounts and longer durations as compared to smaller loans. As a result, participants in short term loans are more complaint as opposed to participants in long term loans. Consistent with the findings of (Mumba, 2019), who alludes that loan range has a direct impact on loan compliance, where smaller loans have a habit of to correlate with higher compliance rates due to more controllable repayment requirements, while larger loans may lead to lower compliance rates because they enforce a greater financial load on the borrower. In the same line Kendall’s Tau Correlation test found a significant relationship between the level of compliance with CDF and CEEC loan requirements and loan tenure. The results are conceivable as a longer loan tenure generally results in lower monthly repayment amounts, while a shorter payment tenure has a larger repayment in a shorter period. Considering the fact that most loan beneficiaries in Chinsali are micro type of business who obtained short term loans and may be facing challenges in loan repayment due to income stability, and poor cash flow.

Kendall’s Tau correlation test finds evidence to suggest that there is a significant relationship between loan compliance and business income, the results infer that positive business performance has a bearing on loan repayment/compliance, which is in line with Modernization Theory of Economic Development, because the more the capital employed, the more the income generated, the greater the expansion in innovation and modernization . The implication of the findings is that MSMEs who have high business income are more loan compliant as opposed to those with low income, findings which are similar to those of (Dominic, 2019) and (Mumba, 2019).

Similar to the Schumpeter’s Innovation Theory of Economic Development, Kendall’s Tau correlation test finds a non-significant relationship between factors influencing loan compliance or non-compliance and nature of business. The findings imply that the nature of the business does not influence loan compliance, the argument is that the nature of a business does not matter, so long entrepreneurs create, take risks and penetrate new markets from CDF and CEEC loans, they can be loan complaint. What mainly determines loan compliance is a stable cash flow stream as opposed to the nature of the business. Loan Non-compliance is more probable to effect where the businesses do not have innovation, fail to grow, or struggle to compete in the market, on the other hand compliance progresses where entrepreneurs use loans for innovation.

There is evident through the Kendall Tau’s correlation test that suggests that, there is a negative significant relationship between factors influencing compliance or non-compliance with loan conditions and marital status. In this scenario the test suggests that, there are some factors that are related to marital status which may decrease the likelihood of loan compliance. The general assumption is that married individuals have a lot of responsibilities and may choose to spend on their families than comply with loan repayments, similar to the pecking order, some MSMEs may prioritize other financial obligations (Family Obligations) over loan repayment, thus triggering non loan compliance.

The Kendall Tau’s correlation does not find significant relationship between factors influencing compliance or non-compliance with loan conditions and business size. The findings suggests that the size of the business does not affect loan compliance, What determines loan compliance is not the size of the business but rather how modern and innovative that business is, in line with Modernization Theory of Economic Development, some business that are smaller in size,may have higher income than those bigger in size as long as they utilize the loans for the intended reason

The Kendall Tau’s relationship finds evidence that there is a significant relationship between maintenance of books record keeping and budgeting and factors influencing compliance or non-compliance with loan conditions. The results suggests that poor accounting records have an adverse impact on loan compliance similar to the principal agency theory, the test suggests that most MSMEs in Chinsali may not fully disclose their financial standing because of poor book-keeping, thus misleading the CDF/CEEC loan authorities, of their financial standing, at the time of applying for the loans this may may trigger loan non- compliance (Saidi, 2024). Additionally lack of proper book keeping may result into poor planning, for business progression as a result this may leading in poor debt management, hence triggering non loan compliance (Dominic, 2019).