Survival Prediction of Nigerian Listed Agriculture Companies: The Use of Altman Z-Score Models

Olabisi Michael Oyinlola, Oladosu Jimoh Balogun, Oyetayo Oyewale Folajin, Nafisat Toyosi Muhammed, Oladipo Oluwafolakemi Fasesin, , , ,

Department of Accountancy , Osogbo, Osun State, Nigeria

Corporate survival is a source of major worry in the business world, particularly in light of unprecedented corporate failure as no investor wants their hard-earned financial fortunes wiped out in bankruptcy. This study aims to forecast the survival status of the extant Nigerian listed agricultural companies by adapting the popular Altman (1968) Z-score and Altman (1983) Z”-score models. The study was carried out on five (5) Nigerian companies in agricultural sector listed in NGX Group and worked on ex-post facto research design, in which case panel data, otherwise called longitudinal data, on the selected companies was collected from their annual reports and accounts as published in their respective websites for the period 2019 – 2023 complemented with data from NGX Group database. Furthermore, market prices of the companies’ shares were extracted from https://doclib.ngxgroup.com/DownloadsContent/. This study adopted two models credited to Prof. Edward Altman with the use of Multiple Discriminants Analysis (MDA). Data were analyzed data using statistical techniques, such as logits to determine the corporate survival probability. Data analysis was also powered by Microsoft Excel. Though there are mixed results, findings reveal that the Altman’s Z-score model is adjudged to be stronger in predicting the financial healthiness of Nigerian agriculture industry that Altman (1983) Z”-score. The study therefore recommends that the companies’ managements should scale up their activities that will ensure improved revenue through the engagement of modern technologies and the service of research consultants.

Keywords: Corporate Survival, Prediction, Altman Models, Accrual-based Variables and Agriculture Industry.

Corporate survival as a measure of organic objective of a corporate organization is about organizing the resources of a firm in a manner that ensures that the firm successfully wades through internal and external environments, progresses and improves in all aspects of its operations and sustains success indefinitely without threat of extinction (Ufo, 2015). The survival of a business is a reflection of the company’s achievements especially in planning and control, employees’ satisfaction, customer retention, market share, technological advancement, innovation and profitability. However, whatever corporate survival strategy a company adopts must be the one that engenders cost cutting and revenue or profit boost, resulting in profitability. Profitability/earnings is a product of accrual accounting, which is an accounting system that recognizes transactions without basing on whether cash flows in or out (Ferry, 2018).

The recent extinction of small-, medium-, and large-scale companies has drawn stakeholders’ attention to the subject of corporate survival, researchers being inclusive. Examples of failed foreign companies are Enron, WorldCom, and Century 21, which went bankrupt in 2001, 2002, and 2020, respectively. In 2019, Nigerian food manufacturer Dangote Flour Mill also failed. Over the past 60 years, research has been done to forecast whether corporate entities would succeed or fail, and prediction models have been created. The pioneering works are those of Altman (1968) and Beaver (1966). However, Altman (1968) is more prominent and pivotal to other firm survival prediction models. Matturungan, Purwanto & Irwanto (2017) affirm that Altman (1968) developed Z-score using five (5) variables to predict corporate financial health and found out that the five financial ratios are significant predictors of corporate bankruptcy.

Essentially, financial healthiness has been empirically predicted by various researchers using variants of Altman models (Agarwal, 2018; Soni, 2019; Cındık & Armutlulu, 2021). Altman has developed three zeta score models applicable to different corporate conditions (Altman 1968 and 1983) models. Altman (1968) developed a five-variable model specifically for predicting corporate financial health in public companies in manufacturing industry. The target of Altman (1983) model, which also uses five (5) variables (with revised coefficients), is the survival prediction of private companies; while Altman (1983) presents a general model capable of predicting the financial well-being of all categories of companies, be it public or private, manufacturing or non-manufacturing.

The three models consciously used accrual data obtainable from Income Statements and Statements of Financial Position. It is impossible to overstate how crucial it is to employ accrual or earnings data in forecasting company survival or failure. One of the most important pieces of business financial data is earnings (Munjal, Singh & Jearth, 2021). The bias of the researchers, as well as the investors, in favour of earnings might be informed by the above propositions.

However, it is undeniable that the trustworthiness of earnings as a result of accrual accounting is hampered by a variety of flaws. The main issue is that profitability does not accurately reflect the amount of cash that a company actually creates over a specific time period, and dishonest financial manipulations exacerbate this. It sums up to say accrual-based earnings undermine the importance attached to cash and, by extension, the interest of stakeholders as it does not give priority to the amount of cash readily available at any given time. In spite of these limitations, however, the Altman’s Z-score models have adjudged to be strong in predicting the financial healthiness of corporate organizations. Altman, Iwanicz-Drozdowska, Laitinen & Suvas (2017) state that the Z-score model is still widely used as a primary or auxiliary tool for bankruptcy or financial crisis prediction and analysis in both research and practice, despite the fact that it was created more than 45 years ago and that there are many other alternative failure prediction models. It is against this backdrop that this paper aims to deploy the Altman (1983) Z” accrual-based model to predict the corporate financial health of the extant Nigerian listed companies in the agriculture industry.

Problem Statement/Justification

The uncertainties surrounding the going concern status of companies today is a source of concern in the contemporary business world. Companies which investors and other groups of users could repose confidence in are falling. In industrialized nations like the United States and the United Kingdom, the accrual models – particularly the Altman Zeta models have been extensively utilized to predict the success or failure of corporations. But the models’ applicability has not been widely tested in Nigeria. In a quest for better business survival/failure prediction model, studies in these industrialized nations have been conducted, employing the four-variable Altman (1983) Z” model. Altman, et al. (2017) claim that the Z”-score model performs admirably in an international setting; notwithstanding, the model is yet to be used to predict the survival or failure of the extant Nigerian public companies, particularly in the agriculture sector.

Objectives of the Study

The proposed study’s main goal is to develop a survival prediction model that listed agricultural companies in Nigeria can use. The specific objectives are as follows:

To adopt the accrual-based Altman’s (1968) five-variable Z score model in forecasting corporate survival of Nigerian listed agricultural companies.

To deploy the accrual-based Altman’s (1983) four-variable Z” score model in predicting corporate survival of Nigerian listed agricultural companies.

Conceptual Review

This section goes over some key ideas related to the research topic. The notion of business survival and the accrual-based Altman models are the specific topics under conceptual examination.

An Overview of Corporate Survival

The goal of corporate survival is to make the most use of the company’s resources in order to sustain operations indefintetly. One of the essential requirements for a business to survive, according to Panigrahi (2018), is that it must be sufficiently liquid and continuously profitable in order to expand and generate wealth. The going-concern theory of accounting is the foundation of the business survival idea. According to the notion, there is no plan by an entity to liquidate in the nearest future (Kaya & Uzay, 2017 and Granstedt & Aronsson, 2021).

Accrual-based Variables

The most important accruals accounting information metrics for this study are equity, liabilities, assets, and profits/earnings. In particular, profitability, efficiency, liquidity, and leverage are derivatives of the key financials. Ratios like profitability, activity/efficiency, liquidity, and leverage/solvency are computed to calculate these derivatives. Accrual accounting-based earnings are defined differently. For example, Srivastav (2023) gives the definition of profits, also known as profit, as the net income of the business after deducting all operational costs, interest, and taxes from sales revenue over a given time period. The timing of receipts and payments is one important factor that sets accruals apart from cash flow, though there are demurrals from willful data manipulation.

Tuovila (2021) defines earnings as the profit a business makes over a given time frame, typically a quarter or a year. Earnings can be measured and used to many different applications. Analysts frequently compute earnings as earnings before taxes (EBT), sometimes referred to as pre-tax income. The earnings before interest and taxes (EBIT) metric is favored by certain analysts. However, some analysts would rather see earnings as earnings before interest, taxes, depreciation, and amortization – abbreviated EBITDA – especially in sectors with a significant proportion of fixed assets.

Altman Models

In 1968, Altman in his paper applied multiple discriminant analysis (MDA) by using five ratios to assess potential failure of companies all of which were manufacturing companies. The model’s accuracy was 95% prior to a year before bankruptcy and 72% two years prior to bankruptcy. Numerous empirical investigations have been conducted utilizing the model to evaluate company survival as well as to categorize businesses into financially distressed and financially healthy ones (Azhar, Lokman, Alam & Said, 2021 and Korath & Nayak, 2022). According to Korath et al. (2022), the Z-score model is the first company survival prediction model that acquired traction and has remained relevant to this day. The model as provided by Altman (1968) is:

Z = 0.012X1 + 0.014X2 + 0.033X3 + 0.006X4 + 0.999X5

The overall index in the Z-score calculation is called corporate failure/survival surrogate (Z), and the five variables are represented by the symbols X1 through X5. The independent variables X1 through X5 represent the following, in the corresponding order: Working capital / Total assets (WC/TA), Retained earnings / Total Assets (RE/TA), Earnings before interest and taxes / Total Assets (EBIT/TA), Market value of equity / Book value of total debt (MV/TL) and Sales / Total Assets (S/TA).

There are three zones of discrimination – the Distress Zone, Grey Zone, and Safe Zone – as identified by Altman into which companies are grouped in this model (Megginson, Meles, Sampagnaro & Verdoliva, 2019). This classifications are as presented below:

Table 1: Z-Score Thresholds

| Z” Score | Discrimination |

| Z” > 2.99 | Safe Zone |

| 1.81 < Z” < 2.99 | Gray Zone |

| Z” < 1.81 | Distress Zone |

Source: Altman (1968)

The above table is interpreted as: businesses with a Z-score of less than 1.81 are probably in serious financial trouble; businesses in the “gray area” are those whose Z-score falls between 1.81 and 2.99. A Z-score of 2.99 or above denotes a Safe Zone, meaning that there is no risk of bankruptcy and the companies will likely survive.

In an attempt to develop a general prediction model that would be applicable to all categories of companies, manufacturing, non-manufacturing, public and private, Altman (1983) developed a four-variable zeta-score model (Z”). The model expunged assets turnover connoted by the 5th variable in the Altman’s 1968 model, i.e. Sales/Total Assets ratio and also substitutes Book Value of Equity/Total Liabilities for Market Value of Equity/Total Liabilities recognized in the Altman (1968) model. The general Z”-Score model developed by Altman (1983) is as stated below:

Z” = 3.25 + 6.56X1 + 3.26X2 + 6.72X3 + 1.05X4

A cursory look at the model reveals that EBIT/Total assets ratio (X3) contributed most to the corporate survival prediction, followed by Working Capital/Total Assets (X1). The coefficients of these two significant ratios are 6.72 and 6.51 respectively. The model was used by Altman, Iwanicz-Drozdowska, Laitinen & Suvas (2017) in assessing the variants of Altman’s models and their study offers evidence that the general Z-Score model works reasonably well for most countries, having approximately 0.75 prediction accuracy. The survival determinant Z” values in Altman (1983) are as given in the table below:

Table 2: Z”-Score Thresholds

| Z” Score | Discrimination |

| Z” > 2.6 | Safe Zone |

| 1.1 < Z” < 2.6 | Gray Zone |

| Z” < 1.1 | Distress Zone |

Source: Soni (2019)

Theoretical Review

This proposed research pivots on agency theory, free cash flow theory and stakeholder theory. The economic theory of agency and the institutional theory of agency, which are complementary to one another, were the brainchildren of Ross (1973) and Mitnick (1973) respectively, and the duo are credited with the development of agency theory. Three fundamental tenets that underpin agency theory are information asymmetry between parties; agent and principal are self-interested utility maximizers; and goal incongruence between parties, necessitating the separation of power (ownership) and control (Kargi & Zakariya, 2020 and Abdelkarim & Zuriqi, 2020). Agency theory essentially makes the assumption that a principal’s and an agent’s interests are not always aligned. It basically deals with disagreements that mostly come up in two important areas that have an impact on both partners in the relationship; and these are a difference in goals or a difference in risk aversion.

Free cash flow is another theory considered relevant for this proposed study. Jensen is recognized in his 1986 paper for having conceived the concept of free cash flow, which led to the development of free cash flow theory (Bhandari & Adams, 2017 and Sila, 2018). Free cash flow is understood to be money that managers can spend, distribute to shareholders, or both (Bhandari et al., 2017). The application of free cash flow implies that the agency problem raised by agency theory is raised because managers may choose not to use the excess cash to maximize shareholder wealth by paying dividends to shareholders. Alternatively, they can put it toward growing their company, which might not benefit the shareholders immediately but could have long-term benefits. One intriguing idea in the explanation of company survival is free cash flow.

According to Gutterman (2023), the term “stakeholder” was first used in reference to businesses in the 1930s. According to the stakeholder hypothesis, a company exists to serve its stakeholders – employees, suppliers, consumers, and other members of the general public – in addition to its owners. Stakeholder theory therefore postulates that an organization’s capacity to provide enough wealth, value, or satisfaction for each of its major stakeholders – rather than just shareholders – is what determines whether the organization survives or fails. This proposed study of business survival prediction is hinged on stakeholder theory because, on the one hand, a company’s ability to survive or fail depends on how well its management can establish and maintain connections with a variety of stakeholders; and on the other, the firms’ survival or failure equally bears heavily on the stakeholders put together.

Empirical Review

The Z-score model was developed by Altman (1968) based on research and analysis of five (5) financial ratios: working capital to total assets, retained earnings to total assets, earnings before interest and taxes to total assets, market value equity to par value of debt, and sales to total assets. The research sample consisted of 66 US manufacturing firms, 33 of which were failed and 33 of which were not. The study period covered by the research was 1946–1965. The outcomes indicated that the five financial ratios are significant predictors in the corporate bankruptcy prediction model.

Babatunde (2017) examines how well Altman’s z-score predicts the bankruptcy of Nigerian manufacturing enterprises that are quoted. A sample of ten manufacturing companies listed on the Nigeria Stock Exchange (NSE) for the 2015 fiscal year was used in this study. Altman’s Z-score model was used to analyze the data collected for the study. According to the research, Z-score is a crucial measure for identifying Nigerian organizations whose performance is declining.

The study by Sari (2017) aims at using the Altman Z Score model to analyze the financial health of listed agricultural sector companies in the IDX years 2013–2015. Thirteen businesses in the agricultural sector between 2013 and 2015 are the subject of this study. This study compares healthy organizations with those that will face difficulties or bankruptcy using five ratios that are aggregated based on the Altman Z score bankruptcy prediction model. Working capital to total assets, retained earnings to total assets, earnings before interest and taxes and total assets, market value of equity to book value of debt, and sales to total assets are some examples of ratios. The study’s findings indicate that, on average, the agricultural sector had 8% of companies in the healthy zone, 31% in the grey zone, and 62% in the distressed zone between the years 2013, 2014, and 2015.

In their study, Musah & Agyirakwah (2019) looked at how well the Altman Z-score model predicted which companies on the Ghana Stock Exchange would go bankrupt or experience financial difficulties. Ten listed companies were chosen as a sample, and one additional company was chosen for validation. Data from 2016 and 2017 for GOIL Ghana Limited, which represented a non-distressed company, and Aluworks, which represented a distressed company, were used in the validation process. A random sample of ten listed companies’ 2017 financial statements served as the basis for the final study. Fifty percent of the companies were accurately forecasted, according to the original prediction’s results, while the remaining companies were misclassified. This therefore implies that the Altman Z-score cannot properly identify financially distressed enterprises in Ghana but can still be effective in delivering alerts.

Sugiyarti & Murwaningsari (2020) researched to demonstrate if the Grover and Altman Z-Score models can forecast bankruptcy and whether their scores differ from one another. A total of 57 financial statement data samples were taken from the Indonesia Stock Exchange (BEI) between 2016 and 2018, and they were split into two groups: 27 financial statement data that went bankrupt (financial distress) and 30 financial statement data that are still ongoing (non-financial distress). Purposive sampling is used in the data gathering process, and logistic regression and paired sample t-test analysis are used for data analysis. The outcome demonstrates that bankruptcy may be predicted using the Grover and Altman Z-Score models. The study’s findings also indicate that the Altman Z-Score model and Grover have different scores when it comes to predicting bankruptcy. According to Sugiyarti et al. (2020), the Altman Z-Score Model is the best model for predicting bankruptcy for retail companies listed on the Indonesia Stock Exchange having attained an accuracy rate of 60%.

Srebro, Mavrenski, Bogojević Arsić, Knežević, Milašinović & Travica (2021) used Altman’s Z-score models, namely the Z-score bankruptcy probability calculation, the Z′-score model (for emerging market enterprises), and the original Z-score model (a model for manufacturing companies) on a sample of agricultural enterprises listed on the Belgrade Stock Exchange between 2015 and 2019 to predict their survival status. The results show that a certain number of companies were in danger of going bankrupt and, also, several companies displayed signals that suggested possible fraudulent financial reporting.

Omolekan et al. (2022) conducted a study on the oil and gas business in Nigeria with the explicit aim of predicting company financial hardship using a multivariate approach. The study uses a longitudinal research approach and focuses on seventeen (17) oil and gas companies, three (3) of which were unsuccessful and fourteen (14) of which were operating, that were quoted on the Nigerian Stock Exchange (NSE) (now the Nigerian Exchange Group (NGX Group) fact books between 2000 and 2018. Multiple Discriminant Analysis (MDA), a multivariate approach, was used on a sample of enterprises over the sample period. The findings indicate that Nigerian oil and gas businesses have a high failure rate, with 23.5% of them being financially weak and 11.8% being gray. Results indicate a large performance gap between organizations in trouble and those in good health.

Rohim, Sandy, Ramadhan & Hidayat (2024) investigated the Altman Z-score model’s predictive power for bankruptcy. This study’s primary focus is on retail businesses that were listed between 2021 and 2023 on the Indonesia Stock Exchange. With 93 financial statements to back them up, 31 businesses took part in the study. For the sampling procedure, the researchers employed the purposive sampling method. The study analyzes the collected data using the modified Altman Z-score method (1995). According to the analysis, 17 businesses (54.8%) fit the definition of healthy. Eleven companies (36.7%) were predicted to file for bankruptcy, while three companies (9.7%) were deemed poor.

This study was carried out on five (5) Nigerian companies in agricultural sector listed in NGX Group. The companies are Ellah Lakes PLC, FTN Cocoa Processors PLC, Livestock Feeds PLC, Okomu Oil Palm PLC and PRESCO PLC. The choice of this sector was informed by the fact that food security has been critical to the existence of mankind in societies and nations. Little wonder that it constitutes the basic necessities in Maslow’s hierarchy of need.

The study adopted ex-post facto research design, in which case panel data, otherwise called longitudinal data, on the selected companies was collected from their annual reports and accounts as published in their respective websites for the period 2019 – 2023 complemented with data from NGX Group database. Furthermore, market prices of the companies’ shares were extracted from https://doclib.ngxgroup.com/DownloadsContent/. Many studies are found to have used the research design in view of its appropriateness (Nwaobia et al., 2019 and Ezekwesili, 2022). The use of secondary data in this study is justified in view of its usability as enumerated above and the fact that the design has been used in the corporate survival or failure prediction by many previous studies from which this current study adapts (Ikpesu, 2019; Özcan, 2020).

Sample frame of agriculture/agro-allied companies listed on the Nigerian Exchange Group (NGX Group) was accessed online, which consists of five (5) firms as at 2024. Since the five (5) companies were covered in the proposed research, the implication is that the target and the study population are the same. From their annual accounts and reports, relevant data were extracted and ratios computed using Microsoft Excel. This study adopted two models credited E.I. Altman with the use of Multiple Discriminants Analysis (MDA) and the data were analyzed data using statistical techniques, such as logits to determine the corporate survival probability.

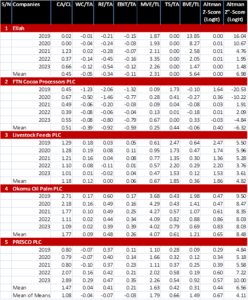

Table 3: Data Presentation and Analysis 1

Z” = 3.25 + 6.56X1 + 3.26X2 + 6.72X3 + 1.05X4

Z” = 3.25 + 6.5 (WC/TA) + 3.26 (RE/TA) + 6.72 (EBIT/TA) + 1.05 (BVE/TL)

Z” = 3.25 + 6.56X1 + 3.26X2 + 6.72X3 + 1.05X4

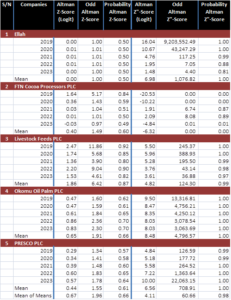

Table 4: Data Presentation and Analysis 2

Odd = e^Logit; Probability = Odd/(1+Odd)

Discussion of Findings

Recalling that with Altman (1968) Z-score model, z-score of less than 1.81 are probably in serious financial trouble; Z-score between 1.81 and 2.99 classifies the company into “gray area” while a Z-score of 2.99 or above means that the has a good financial health condition. Throughout the selected years, Ellah Lakes PLC’s Z-scores were far below the minimum threshold (0.00 – 0.01) and had low probability of survival (0.5) (see Table 2). The mean Z-score was 0.00 and the mean probability was 0.00 and this indicates that the company is not in good survival position. The reason for its poor state of financial health was that the company had little or no sales in the years under consideration because it had harvested neither its oil palms nor its cassava tubers. As a result, it had been living on both current and non-current liabilities. Altman (1983) Z”-score model classify companies with the survival determinant Z” greater than 2.6 as those in safe zone. By this classification, Ellah is a safe company for its stakeholders from 2019 till 2021. It is only in 2022 and 2023 that they fell into gray areas. The probability of its survival ranges from 0.81 to 1.00 and the mean values were 0.68 and 1 respectively for Z”-score and its corresponding probability. This therefore suggests that Ellah is a company that stakeholders can rely upon. The two models obviously provide mixed results.

Altman’s Z-score model shows that FTN Cocoa Processors PLC had weak financial health status as the Zeta scores for the selected five (5) years were below 1.81 benchmark (-0.03 – 1.64). The highest probability of survival was 0.84. Similar findings are revealed by Z”-score model as it shows negative Z”-scores in three of the selected years, thereby suggesting that the company was in distress in those years. Two other years (2021 and 2022) were observed to be in gray areas having Z”-score to be 1.91 and 2.09 respectively and survival probability being 0.87 and 0.89 in that order. In 2023 for instance, the company had neither local sales nor export sales coupled with the challenge of translation of its foreign balances to naira. The company had been producing below capacity of 5% due to lingering working capital inadequacy. This impacted on the gross margin as a result of huge fixed cost that has to be borne (FTN Annual Report 2023). The mean for the five-year period analysis shows survival probability of 0.60 (Z-score) and 0.00 (Z”-score) which suggest that the company needs immediate attention.

Livestock Feeds PLC was in gray zone in 2019 and 2022 and in high risk of distress in the other three years according to Z-score model, having the survival probability ranging from 0.8 –0.92. Its mean Z-score was 1.86 and mean probability was 0.87. This suggests that the company is in gray zone. Considering the Z”-score model, the Z”-scores of Livestock Feeds PLC were well above the upper threshold, ranging from 3.61–5.96. The probability of its survival for the five years ranged from 0.97 to 1. The Z”-score model gives an indication that all is well with the company, with the mean values of 4.82 and 0.99 for the Z”-scores and probability respectively.

With the application of Z-Score model, Okomu Oil Palm PLC was in distress zone throughout the five years as the Z-scores were from 0.47 to 0.86. The probability of the company’s survival ranges from 0.61 to 0.70. Also, the mean Z-score and mean probability were respectively 0.65 and 0.66. Whereas in the case of applying Z”-score model, Z-scores were all above 2.6 and the probability for each year considered was 1, implying that the company was far from the risk of corporate failure.

PRESCO PLC appeared to be in poor corporate health status after Ellah Lakes PLC as its highest was 0.6 and mean Z-Score was 0.44. This is when Altman (1968) Z-score model is adopted. The survival probabilities of the company for the five years under consideration ranged from 0.57 to 0.65 with the mean probability being 0.61. On the contrary, Z”-score model had findings that indicates that the company was in a safe zone throughout the five years considered and the survival probabilities ranged from 0.99 to 1. The mean values were 6.56 and 1 for Z”-score and survival probability respectively. This analysis suggests that the company is far from experiencing bankruptcy.

Limiting Factors and Government’s Responsiveness

Within the period covered in this study however, Nigerian agriculture companies faced significant challenges due to rising inflation. The increasing costs of raw materials and operating expenses eroded profit margins, leading to substantial declines in their net profits. This has the potential to bring about financial distress and eventual bankruptcy (Tyaga & Kristanti, 2020). For instance, in the third quarter of 2022, Livestock Feeds, Okomu Oil Palm and Presco Plc reported a combined profit after tax of ₦3.5 billion, marking a 39.6% decrease from ₦5.79 billion in the same period in 2021. This decline was primarily attributed to a 69.8% surge in the cost of sales, driven by factors such as currency depreciation and increased prices of inputs (nairametrics, 2022).

Also, the exchange rate fluctuations between 2019 and 2023 had a dual effect on listed Nigerian agricultural companies. While a weaker naira enhanced export revenues, it concurrently increased operational costs due to higher prices for imported inputs. Additionally, exchange rate policy changes introduced financial challenges related to foreign currency obligations. The overall impact on the profitability and survival of these companies depended on their ability to leverage export opportunities and manage increased costs effectively.

The Altman (1968) Z-score that indicates financial distress was partly due to industry-specific factors encapsulated in waiting period between planting and harvesting, seasonality, climate risks, etc. This particularly affected Ellah Lakes PLC throughout the period under consideration in this study to the extent that there was little or no turnover. Yet, all the fixed costs were met resulting in loss through the research period.

In the face of the above limitations, the Nigerian government implemented several policies to bolster the agricultural sector, especially between 2019 and 2023 covered in this study. These policies aim at ensuring the survival and growth of agribusinesses, including publicly listed companies. One of the government initiatives that are most relevant to the companies under study is Tax Incentives. In October 2022, for instance, government approved a five-year tax holiday for agricultural investors. This policy also offered tax-free agricultural loans with extended repayment periods and zero tariffs on agrochemical imports, aiming to stimulate investment and enhance productivity in the sector (Olokor, 2022).

According to Nnodim (2022), Federal Government launched National Agricultural Technology and Innovation Policy (NATIP) 2022-2027 in August 2022. This policy focuses on modernizing agriculture through technology adoption, mechanization, and value chain development. The policy seeks to create a more conducive environment for agribusinesses by addressing critical areas such as stakeholder synergy, knowledge transfer, and market development.

Not only did Government promote Public-Private Partnerships (PPPs) to attract investment in agriculture, it also made efforts to update and implement the National Agricultural Seed Policy to ensure the availability of high-quality seeds. This policy aimed to boost crop yields and enhance the competitiveness of Nigerian agribusinesses. In effect, collaborations with international organizations led to the development of sector-specific investment incentive policies, resulting in the establishment of new agribusinesses and increased local production (Adeniyi, 2023).

These policies collectively aimed to create a more favorable environment for agricultural companies, including those publicly listed, by providing financial incentives, modernizing practices, and fostering collaboration between the public and private sectors.

Managerial Implications

The above findings indicate a complex financial situation for Ellah Lakes PLC, with several implications for managerial decision-making. For instance, heavy reliance on liabilities with minimal or no revenue generation indicates inefficiencies in operational planning and this is not a good condition for the company. Essentially, instead of waiting for three or more years before harvest to the extent that little or no revenue was recorded over the period under study, Managers should diversify income streams and exploring strategic partnerships that may help mitigate financial risks. This will ensure steady growth and survival and sustain stakeholder confidence. However, it is hoped that the financial status of the company would change for better when it crop harvests begin.

The findings from Altman’s Z-score and Z”-score models indicate that FTN Cocoa Processors PLC is facing severe financial distress, with a high probability of insolvency if no corrective measures are taken. The Managerial implications of these findings are significant and demand urgent strategic actions in the areas of financial restructuring by debt restructuring, equity injection and seeking government or institutional support; improving working capital management, by optimizing inventory, improving receivables collection to enhance cash flow and negotiating better credit terms with suppliers to ease short-term liquidity constraints; revenue diversification by expanding into new export markets, strengthening domestic sales through partnerships with retailers, manufacturers, or direct consumer channels, and leveraging e-commerce and digital marketing to reach more buyers. The weak financial health of FTN Cocoa Processors PLC signals the need for stronger governance and this can be improved by strengthening internal controls, enhancing financial reporting transparency and improving board oversight and leadership effectiveness.

The Z-score model suggests that Livestock Feeds PLC was in the gray zone in 2019 and 2022 and at high risk of distress in other years and this has significant managerial implications. This implies potential financial instability, requiring management to focus on liquidity, profitability, and capital structure to avoid bankruptcy. The distress risk as shown by the Z-score model implies that Livestock Feeds PLC might have a fragile capital structure, possibly characterized by high leverage or declining asset turnover. So, Managers should assess debt levels and optimize financing strategies. Also, the low Z-score values in some years might indicate issues such as low profitability, inefficient asset utilization, or high operational costs. Management should focus on cost-cutting, process optimization, and revenue diversification to improve profitability and move out of the gray zone.

The high risk of financial distress as suggested by Altman (1968) Z-score carries important managerial implications for Okomu Oil Palm PLC in terms of financial strategy, risk management, investor relations, and operational decisions. The Z-score, in effect, signals the need to review or consider new strategies like debt reduction, cost efficiency operations, and revenue streams diversification for improved profitability. Going by the model, the company might have the challenge of gaining investor confidence and have difficulty in securing external financing. Hence, the company should engage with its credit providers by clarifying convincingly the company’s financial position so as to be able to secure loans.

The managerial implications of research findings on Presco PLC span financial strategy, risk management, investor relations, and operational efficiency. The poor Z-score (mean of 0.44) suggests that Presco PLC may be financially distressed and at risk of insolvency. This indicates the need for immediate strategic financial adjustments, such as improving liquidity, optimizing debt levels, and enhancing profitability. Most significant variable in Z-score model is efficiency (i.e. Sales/Total Assets ratio), the poor Altman Z-score implies the need for cost-cutting measures, improved asset utilization, and operational efficiencies to improve revenue generation. Because investors relying on the Altman Z-score model may view Presco PLC as a risky investment, the management must provide transparent financial disclosures and contextualize financial statements to build investor confidence. Moreover, the Altman model may negatively impact the company’s ability to secure loans or favorable credit terms, there is therefore a need for the Management to engage with its financial institutions by clarifying the company’s financial position in order to stand good chances for loan access.

Considering the five companies globally, the implication of the overall Z-score of 0.67 is that NGX-listed agricultural companies were facing a high risk of bankruptcy. Managers should therefore enhance their liquidity, reduce leverage, optimize working capital and boost operational efficiency to improve their companies’ financial status.

Given the low survival probability (0.66) from the Altman (1968) Z-score, investors in the agriculture industry may perceive the sector as risky, and this may potentially reduce the companies’ access to capital. Managers should be proactive in improving their revenue streams that will resultantly enhance their profitability in order to attract investors. They should critically evaluate their business models and explore diversification into value-added agricultural products to improve profitability and financial resilience. Moreover, the traditional Z-score that indicates financial distress was partly due to industry-specific factors encapsulated in seasonality, climate risks, etc. It is therefore imperative for managers to adopt better risk mitigation strategies, such as agricultural insurance and technology-driven solutions.

Also, the low probability score for survival suggests a need for a balanced capital structure. Companies should avoid excessive debt and focus on long-term stable financing options such as equity financing, government support, or agribusiness grants. Managers should also analyze their cost of capital to ensure that financial decisions align with long-term sustainability.

Suffice to say that Managers must take a multi-dimensional approach when assessing financial health. While the traditional Z-score indicates vulnerability, the Z”-score suggests strength. To ensure long-term sustainability, companies must balance financial risk, optimize capital structure, and improve operational efficiency while maintaining transparency with investors.

Analysis above clearly shows that the two corporate survival prediction models used in this study reveal mixed results. What specifically marks the difference in the models is the Sales-to-Total Assets ratio included in Z-score model but which is not in the Z”-score model. The poor financial healthiness of the companies bothered on the fact that their activities in generating revenue were inadequate. Because the S/TA ratio carried the greatest coefficient (0.999), a company that is able to generate reasonably high amount of revenue, all things being equal, would strongly stand on survival pedestal. The causes of Ellah Lakes PLC’s weak corporate survival status was immaturity of their farms for harvest in the period under consideration. The company’s survival status would change by the time its starts the harvest and begins to convert it to revenue. It is therefore concluded that Altman (1968) Z-score model predicts more reliably than the Altman (1983) Z”-score model. To support this argument, Altman (1983) Z”-score model classified Ellah Lakes PLC as being safe even when there were nil revenue. Whereas Altman (1968) Z-score model labeled it as having likelihood to experience bankruptcy. This is conformity with the empirical evidence by Leek (2018) and Cındık et al. (2021) that Altman (1968) has a great prediction power for corporate survival or otherwise.

In the light of the above, it is recommended that the Managements should:

Suggestion for Further Study

To enhance the value of the results obtained, future research could be carried out, especially for Ellah Lakes PLC when it begins its harvest and revenue starts to appear in its financial statements. Integrating qualitative insights from financial experts, corporate executives, or policymakers would also provide a more comprehensive understanding of the challenges of corporate survival. Furthermore, the inclusion of additional financial models or machine learning techniques could offer a more nuanced comparison of forecast accuracy.