Sustaining Cryptocurrency Investment: Does the Moderating Effect of Critical Success Factors (Csfs) Matter? Empirical Evidence

Thurga Thevi Sitivinaigan1

Cheok Mui Yee2

Woodlands Singapore

Theoretical Framework: Cryptocurrencies have a substantial economic and social impact to investors’ decision-making. This paper aims to investigate critical success factors (CSFs) from behavioural aspects and their moderating effect on cryptocurrency investment among working adults in Malaysia.

Method: A quantitative survey questionnaire approach was implemented to gather data from 533 working adults who resided in Malaysia. Structural Equation Modelling (SEM) path analysis was also used to examine the impact of critical success factors of cryptocurrency investment.

Results and Discussion: Key findings from this study reveal that usage competency, societal influence, the perceived threat of utilisation, and technology complexity are critical success factors that would either encourage or hinder the investment of cryptocurrency. Among them, working adults’ societal influence is empirically the key critical success factor in sustaining cryptocurrency investment, followed by adults’ usage competency and technology complexity.

Research Implications: This paper notes that working adults tend to utilise a great substantial of their competency to invest in cryptocurrency when the technology is highly complex. Besides, when the perceived threat of the utilisation is great, working adults greatly utilise societal influence to mitigate the threat of cryptocurrency investment.

Originality/Value: This study contributes to the understanding of the moderating effect of technology complexity and investors’ perceived threat of utilisation in the investment of cryptocurrency. It also offers an insight into the financial behaviour of working adults, as they are investors themselves, in the context of emerging digital finance while offering insightful recommendations to stakeholders in the cryptocurrency ecosystem.

Keywords: cryptocurrency investment, critical success factors (CSFs), sustainable development goals (SDGs), societal influence, working adults, Malaysia

Paper type: Research paper

The substantial surge in the adoption of cryptocurrency in recent years and the remarkable quantity of cryptocurrency users that engage in trading transactions has piqued the heightened and thereby gained the attention of scholars and practitioners (Khan & Hakami, 2022). That is why World Environment and Development Commission (WCED) urged recent scholars to sustain the economic growth for the future investors (Hussain et al., 2025). In order to align with the Sustainable Development Goals (SDGs), it is ascertained that sustaining cryptocurrency investment is considered as a long-term thinking approach while depending on technological development. Since the cryptocurrency investment involves the understanding of blockchain technology, it is argued that the adoption of technology in such investment is aligned within the context of the sustainable development approach as per the agenda of Sustainable Development Goals (SDGs) (Hussain et al., 2025). However, the empirical investigation into the utilization of cryptocurrency bitcoin remains in its early stages due to its newness and distinctiveness of technology (Chagas et al., 2024).

Over the past decades, the globe has seen significant transformations resulting in the widespread use of sophisticated technologies (Prakoso et al., 2024), such as peer-to-peer blockchain networks (Nag & Manohar, 2024). Nevertheless, the adoption of cryptocurrency is still constrained in terms of its geographical reach (Saleem et al., 2024) and it is accompanied by fluctuations in pricing (Nugrahani et al., 2024), economic structural challenges (Kayani & Hasan, 2024) and potentially illicit undertakings (Gupta, 2024).

Despite its significant implications, there is a lack of scholarly study on critical success factors (CSFs) that may affect potential investors’ inclination to invest in cryptocurrency (e.g. Almeida & Gonçalves, 2024). Although cryptocurrency has been traded in Malaysia since 2012, potential investors in Malaysia may not be aware of the likely hazards of cryptocurrency investment, such as potential fraudulent and complications in transaction processing (Toufaily et al., 2021). Hence, the purpose of the study is to, first, investigate critical success factors (CSFs) of investment in cryptocurrency among working adults in Malaysia. Secondly, it aims to examine the moderating effect of critical success factors (CSFs) that affect young working adults’ behavioural intention.

Although numerous past theories, such as Technology Acceptance Model (TAM) (e.g. Idrees et al., 2024), Technology Readiness Index (e.g. Chern, Aun et al., 2024), were adopted to investigate the intention of cryptocurrency investment, contradictory empirical findings were debated heavily in terms of personal and environmental factors and their impacts on investors’ behavioural actions (Toufaily et al., 2021). Hence, this study adopted the concept of theory of planned behaviour to investigate potential investors’ behaviour in cryptocurrency investment.

Potential investors possess a certain level of awareness about cryptocurrency investment (Panos et al., 2020). However, Shuhaiber, et al. (2023) contended that people with innovative and forward-thinking mindset are more likely to have a favourable attitude towards disruptive technology like cryptocurrencies. Possessing a solid understanding of financial knowledge and technology instruments increases the possible likelihood of employed individuals investing in cryptocurrency. People perceive cryptocurrency as an investment opportunity (Bhilawadikar & Garg, 2020) is attributed to the extent of their competency of financial information as well as technology. By doing so, people are able to have a better investment judgment if they are competent about such investment. Hence, it is posited that the higher the level of adults’ usage competency in financial knowledge, the more likely they invest in cryptocurrency.

Gil-Cordero et al. (2020) argued that social media has an indirect impact on people’s intention to use cryptocurrency. Chern et al. (2024) noted that middle- and lower-class people in Malaysia are influenced by their network’s recommendation of an optimistic viewpoint on such investment, which comes from trustworthy friends and family (Alsaghir, 2023). Cryptocurrency investment gains greater credibility among people as an investment option if positive feedback about such investment is spread on social media. Hence, it is posited that the more positive the societal influence is generated from working adults’ social circle, the more they are to invest in cryptocurrency.

While the investment of cryptocurrency relies on individuals’ attitudes towards the probable failure of technology (Redhwan Al-Amri et al., 2019), individuals perceive that the risk is dependent on confidence in one’s skills and expectation of future outcomes (Gil-Cordero et al., 2020). However, contradictory with their findings, Balapour et al. (2020) argued that there is no correlation between the perceived security risk of individuals and its investment in cryptocurrency. Similarly, Ter Ji-Xi’s et al. (2021) finding also ascertained that individuals’ perceived danger is not a significant predictor of cryptocurrency investment in Malaysia. Despite contradictory results, people who are afraid to take chances tend to be more cautious with their finances and gravitate toward safer, more conventional investing options. It is, thus, assumed that the perception of threat among people and cryptocurrency investment are invertedly related. Hence, it is posited that the greater working adults’ perceive the threat of utilisation of cryptocurrency as a form of investment, the less likely they invest in cryptocurrency.

Past studies (e.g. Gupta et al., 2024; Mnif et al., 2024) of technology complexity stated that there is a favourable influence of people’s perceived utility on the intention to utilise cryptocurrencies. The desire to utilize the digital system and cryptocurrency is greatly encouraged by people’s perception of pleasure (Nadeem et al., 2020) Still, the investment of cryptocurrency is hindered by the discomfort of technology complexity. Making sense of cryptocurrency’s utilisation may seem like a huge undertaking that calls for a lot of expertise and time (Khan & Hakami, 2022). Hence, it is posited that the greater the technology complexity of cryptocurrency investment, the less likely that they are to invest in cryptocurrency.

Shuhaiber, et al. (2023) found that people with a positive outlook and a willingness to try new things are more likely to be open to disruptive technology like cryptocurrency. Particularly, people from Asia, such as South Korea and China, are more likely to invest in cryptocurrencies, as they are creative and open to new ideas (Radic et al., 2022). Similarly, Hasan, Ayub et al. (2022) affirmed that people’s innovativeness moderates their propensity to use cryptocurrency. Senkardes & Akadur (2021) explained that working adults are less likely to express the intention to invest in cryptocurrency when they perceive this investment as more complex in technology usage because individuals may tend to lean towards investment options that they perceive as straightforward, uncomplicated, and easily comprehensible. Hence, it is posited that when technology is highly complex, working adults tend to utilise a great substantial of their usage competency to invest in cryptocurrency.

People’s decision-making behaviour is influenced by the perception of technology complexity when performing cryptocurrency investment, such as the familiarity with blockchain technology (Ullah et al., 2021) and the overall intricacy of the investment process. Although they perceive high complexity in technology, they may be positively engaged in investment activities as long as they gain societal support (Chern et al., 2024) because people’s beliefs, practices, and outlooks on cryptocurrency investment are possibly shaped by their own and yet personal social networking circles (Danforth et al., 2020). Hence, it is posited that when the perceived threat of the utilisation is great, working adults greatly utilise societal influence to mitigate the threat of cryptocurrency investment.

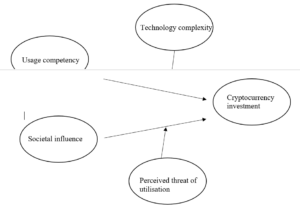

Based on the hypotheses stated above, the conceptual framework of this study is illustrated in Figure 1 below:

Figure 1: Conceptual framework

The cross-sectional quantitative questionnaire survey was adopted in this study. An online survey was used to distribute survey forms to respondents in this study. There were 116,517,000 individuals (Statista Research Department, 2023) who were categorised within the age group of 25 to 54 years as target respondents. Systematic random sampling approach was employed and the recommended sample size was 385 participants in this study. However, to bolster the study’s robustness and account for potential non-responses and data inconsistencies, data collection efforts were expanded to 533 respondents, which surpassed the minimum requirement as stated by Krejcie & Maorgan (1970).

Measurement items for perceived threat of utilisation were adapted and modified from Metzger & Fehr’s (2018) study due to its satisfactory reliability scores. An example of this instrument is that ‘The uncertainty of whether the markets will rise, or fall keeps me from investing cryptocurrency’. Measurement items for cryptocurrency investment were adopted and adapted from Sivaramakrishnan’s et al. (2017) study because it was one of the widest adopted instrument by past researchers. An example of this instrument is that ‘I expect to invest in cryptocurrency’. Measurement items for usage competency were adopted and modified from Cristofaro’s et al. (2022) study because it had satisfactory reliability score in the their studies. An example of usage competency was that ‘I invest in cryptocurrency because I am competent in investing with crypto assets’. Measurement items for societal influence were adopted and modified from Pham’s et al. (2021) study due to its satisfactory reliability score as well. An example of societal influence was that ‘Opinions of important people in my life, such as family, spouse, and close friends, influence my decision to invest in cryptocurrency investment’. Measurement items for technology complexity were adopted and adapted from Bharadwaj & Deka’s (2021) study because its Cronbach Alpha’s score was satisfactory in their studies. An example of this instrument is that ‘Learning to invest in cryptocurrency using computers would be difficult for me’.

All the questionnaire items were rated using a Likert-type scale ranging from 1 to 5, with 1 representing “Strongly Disagree” and 5 representing “Strongly Agree”. The survey form further had a set of demographic inquiries to gather information from respondents, which include their age, gender, employment status, occupation, years of experience, and monthly income.

Statistical analysis, such as demographic and statistical analysis, was analysed using the Statistical Package for the Social Sciences (SPSS) version 26 and Partial Least Square–Structural Modelling Equation (PLS-SEM).

Demographic and Statistical Analysis

The demographic composition offers pivotal insights into working adults’ profile in Malaysia. There were 324 males (60.8%) and 209 females (39.2%) and the age distribution is concentrated between 25-35 years old (40.5%) and 35-45 years old (41.0%). 396 respondents were employed (74.3%) and 137 respondents were self-employed (25.7%). 83 respondents were in Government/Public Sector (15.6%) and 67 respondents were in Finance/Banking (12.6%) sectors. 204 respondents had 10-15 years (38.3%) working experience.

Mean values observed for perceived threat in utilisation (i.e., 2.697), societal influence (i.e., 3.6223), usage competency (i.e., 2.809), and technology complexity (i.e., 2.803) suggested that respondents hold a neutral view in the cryptocurrency investment. However, the standard deviation for the perceived threat in utilisation (i.e., 1.325) and usage competency (i.e., 1.4071), highlighted a significant diversity in the attitude of respondents as well as their competency levels and thereby results in the inconsistency of past empirical results.

In terms of skewness analysis, there was a slight right skewed in the perceived threat of utilisation (i.e., 0.357) and usage competency (i.e., 0.386), which suggested that only a minority of respondents with higher than an average perception of danger and usage competency in concurrency investment.

In terms of kurtosis analysis, the less peaked distribution with lighter tails than a normal distribution is reflected in the perceived threat of utilisation (i.e., -1.300) and usage competency (i.e., -1.302).

Analysis of measurement & structural model

Cross loading showed that each factor obtained the standardised loading that are greater than 0.7, after the deletion of the item 5 of the observed variable (i.e., perceived threat of utilisation), as its loading is less than 0.7 (Chin, 1998). The composite reliability and Cronbach’ Alpha of all the variables illustrated that they were greater than 0.7 and so it is confirmed that they satisfied the internal consistency’s requirement. Average variance extracted (AVE) also showed that variables were greater than 0.5 and thus the convergent validity was met. HTMT values were correct in all cases (i.e., <0.9) (Gold, Malhotra & Segars, 2001) and the square root of the AVE was greater than the correlation among constructs, which confirmed that the discriminant validity criterion was met (Roldán & Sánchez-Franco, 2012). Refer to Table 1 and 2.

Table 1 Construct reliability and convergent validity

| Cronbach’s alpha | Composite reliability | Average variance extracted (AVE) | |

| Cryptocurrency investment | 0.934 | 0.941 | 0.835 |

| Perceived threat of utilisation | 0.971 | 0.987 | 0.919 |

| Societal influence | 0.931 | 1.078 | 0.857 |

| Technology complexity | 0.952 | 0.956 | 0.876 |

| Usage competency | 0.999 | 0.999 | 0.996 |

Table 2 Divergent validity

| CI | PTU | SI | TC | UC | |

| Cryptocurrency investment | 0.914 | 0.741 | 0.200 | 0.711 | 0.549 |

| Perceived threat of utilisation | -0.723 | 0.959 | 0.142 | 0.878 | 0.472 |

| Societal influence | 0.211 | 0.010 | 0.926 | 0.351 | 0.594 |

| Technology complexity | -0.676 | 0.852 | 0.280 | 0.936 | 0.591 |

| Usage competency | 0.542 | -0.468 | -0.538 | -0.572 | 0.998 |

| CI = cryptocurrency investment; PTU = perceived threat of utilisation; SC = Societal influence; TC = Technology complexity; UC = Usage competency. Bold data on the diagonal are the square root of the AVE. data located below the diagonal are the correlations between the contracts. Data above the diagonal are the HTMT values. | |||||

For structural model assessment, the goodness of fit of the model was high, as R square was 0.878 and so it indicated that the explanatory power of the model was high, since all the variables of the model explained 87.8 of the variance in the cryptocurrency investment. The Q square of the model was greater than zero, which showed that all the exogenous contracts had predictive relevance and the model moderately explained the cryptocurrency investment.

As shown in Table 3 and Figure 1, the findings showed that societal influence was the key factor affecting cryptocurrency investment and the with usage competency was placed second. The third critical success factor was technology complexity and then followed by the perceived threat of utilisation.

It also evidenced that the more positive the societal influence is generated from working adults’ social circle, the more they are to invest in cryptocurrency. Also, the more positive the societal influence is generated from working adults’ social circle, the more they are to invest in cryptocurrency. The greater working adults’ perceive the threat of utilisation of cryptocurrency as a form of investment, the less likely they invest in cryptocurrency. The greater the technology complexity of cryptocurrency investment, the less likely that they are to invest in cryptocurrency. When technology is highly complex, working adults tend to utilise a great substantial of their usage competency to invest in cryptocurrency. Lastly, when the perceived threat of the utilisation is great, working adults greatly utilise societal influence to mitigate the threat of cryptocurrency investment.

It is also interesting to note that the effect size was large when the perceived threat of utilisation was taken into consideration because working adults significantly relied on societal influence to reduce the threat of investing in cryptocurrency. The effect sizes for the remaining hypothesis were medium instead.

Table 3 Path analysis

| Path coefficient | t-

value |

p-value | |

| H1: Usage competency à Cryptocurrency investment | 0.307 | 10.568 | 0.000** |

| H2: Societal influence à

Cryptocurrency investment |

0.384 | 13.108 | 0.000** |

| H3: Perceived threat of utilisation à Cryptocurrency investment | -0.276 | 4.496 | 0.000** |

| H4: Technology complexity à Cryptocurrency investment | -0.381 | 6.381 | 0.000** |

| H5: Technology complexity x Usage competency à Cryptocurrency investment | 0.316 | 13.585 | 0.000** |

| H6: Perceived threat of utilisation x Societal influence à Cryptocurrency investment | 0.388 | 14.391 | 0.000** |

Significant at 0.05 level.

Figure 2: The graphical model of the path coefficient and R square

This study examined critical success factors (CSFs) of cryptocurrency investment in the context of Malaysia. This study found that societal influence from working adults was the most critical success factor in cryptocurrency investment, followed by adults’ usage competency and the technology complexity of the investment. The first notable remark is that working adults often used a significant amount of their skills to invest in cryptocurrency, despite the technology’s complexity. When the perceived threat of use was high, working adults relied heavily on societal influence to reduce the risk of cryptocurrency investment. The second notable remark is that societal influence was the primary factor in cryptocurrency investment. The more positive the societal influence from working adults’ social circle, the more likely they were to invest in cryptocurrency. This result aligns with Rouhani & Abedin (2020), indicating that a better understanding of information from news stories, online forums, and social media leads to a deeper comprehension of cryptocurrency investment. Social influencers significantly promote cryptocurrency investment to potential investors, greatly influencing their decisions through the sharing of positive experiences.

Usage competency was the second key factor in cryptocurrency investment. Higher adult financial knowledge competency increases the likelihood of investing in cryptocurrency. Technology complexity was a key factor in cryptocurrency investment. Higher technology complexity in cryptocurrency investment reduced the likelihood of individuals investing in it. This conclusion suggests that having significant technology expertise was essential for encouraging cryptocurrency investment among potential investors. The threat of utilisation was the fourth key factor in cryptocurrency investment. The more working adults perceived cryptocurrency as a risky investment, the less likely they were to invest in it. Risk-averse investors were generally less involved in cryptocurrency compared to risk-takers. This finding contradicts Ter Ji-Xi et al. (2021), which stated that perceived danger was not a significant predictor of cryptocurrency investment in Malaysia. Possible reasons include religious beliefs (Ayedh et al., 2021) and socio-cultural practices (Megat et al., 2024) in Malaysia, where most are conservative investors (Chock & Chin, 2024) in disruptive financial investments.

This study also presented two new empirical results of indirect hypotheses. When technology was complex, working adults often used a significant portion of their skills to invest in cryptocurrency. When the perceived threat of use was high, working adults relied heavily on societal influence to reduce the risks of investing in cryptocurrency. The result showed that positive referrals from social circles increased the likelihood of adults investing in cryptocurrency, despite their perception of high utilisation risks. Chern et al. (2024) noted that cryptocurrency investment might be swayed by the positive perspectives of one’s social network, stemming from reliable individuals and group discussions. Cryptocurrency investment could gain credibility among working adults as a viable option if positive feedback circulates on social media, despite its high perceived risks.

This study’s empirical findings affect legislators, financial institutions, educational institutions, and cryptocurrency investment community and peer groups. Several limitations must be considered in this study. Exclusively studying Malaysia may limit the population’s geographic reach. Future research could examine cryptocurrency investment behaviour in Indonesia, which has a similar social culture to Malaysia. Comparative research in other countries can reveal how cultural, economic, and regulatory differences affect investors’ views and investment behaviour. This cross-sectional study examined Malaysian cryptocurrency investors’ behaviour using a self-reported questionnaire. Despite its usefulness, questionnaires can cause social desirability bias (Zhu et al., 2024). Future researchers may use a qualitative approach to study cryptocurrency investors’ incentives, concerns, and decisions. The study examined cryptocurrency investment behaviour overall rather than by category because investors may accept different cryptocurrencies differently. Bitcoin is unique among cryptocurrencies due to its global acceptance. Future research could examine investor behaviour in different cryptocurrency categories (Wang et al., 2024). Investors’ interest in Ethereum, Bitcoin, and new altcoins can reveal their behaviour (Saab & El Samad, 2024).