Factors Influencing User Retention and User Experience in Malaysian Fintech

¹Mohd Fairuz Adnan*, ² Erisya Nadira Efendi, 3Muhammad Wafiy Asyraf Zamri, 4Nuremilianatasha Ridwan, 5Yusrah Yusoff

1,2,3,4,5 Faculty of Accountancy, Universiti Teknologi MARA, Cawangan Selangor, Kampus Puncak

Alam, Selangor, Malaysia.

The emergence of financial technology (Fintech) has brought about a transformative shift in consumer experiences within the financial sector, both nationally and globally, including Malaysia. Over the past decade, Malaysia has witnessed a rise in adopting Fintech services such as online banking and mobile payments, establishing Fintech as a crucial tool for businesses in the country. However, despite its widespread usage, some individuals still hesitate to embrace Fintech services for various reasons. In this highly competitive Fintech market environment, customer retention is vital in sustaining a business. To gain a competitive advantage, companies need to understand the factors influencing customer experience and retention in Fintech services from the customers’ perspective.

This conceptual study utilizes a simple Systematic Literature Review (SLR) approach to propose a conceptual framework that investigates the relationships between independent variables which are (1) personalization, (2) security, (3) efficiency and seamless transactions and customer experience and retention in Fintech through a comprehensive article review. Delving into these factors aims to enhance our understanding of how they impact customers’ desire and hesitancy in adopting fintech services. Based on these insights, recommendations can be made for the fintech sector to maintain customer retention in fintech services effectively.

Keywords: Fintech, Personalization, Security, Efficiency and Seamless Transaction, User Experience and User Retention

Fintech, short for financial technology, encompasses the utilization of new technology to enhance and automate financial services. With advancements in information technology, Fintech has rapidly expanded, offering innovative financial solutions that attract significant attention. It aims to assist businesses, company owners, and consumers in managing their financial operations and procedures effectively. Fintech relies on specialized software and algorithms implemented in computers and mobile devices.

The emergence of Fintech brings new opportunities by enhancing transparency, reducing costs, eliminating intermediaries, and providing access to financial information (Zavolokina et al., 2016). Fintech companies have expanded beyond online platforms and ventured into the mobile realm, including mobile payment services. In the digital age, Fintech plays a substantial role in our daily lives and has become a crucial tool for financial transactions. Traditional online banking services offered by conventional financial institutions also evolved to provide innovative and differentiated financial solutions through non-financial providers.

In the post-pandemic era, digital financial products and services have become essential. Consumers increasingly opt for online transactions, driven by concerns over COVID-19 and the need for social distancing (Adnan et al., 2023). While Fintech has gained significant attention, its long-term sustainability remains uncertain. Some users express skepticism about using fintech services due to perceived risks and their own experiences regarding Fintech’s efficiency, convenience, personalization, security, and safety. These factors can positively or negatively impact user experiences, consequently influencing their ongoing adoption of fintech services. Arora et al. (2023) revealed that perceived benefits and trust significantly influence the intention to use FinTech services positively, while perceived risk has a significant negative impact on adoption. Therefore, it is essential to identify the factors contributing to users’ continued usage of Fintech services and the reasons behind their reluctance to adopt such services.

The increase in digitalization of the economy in Malaysia has enabled the country to spread the growth of the digital economy across the region. Malaysian government officials are actively positioning the country as ASEAN’s digital economy hub, driven by significant investments in digital infrastructure, including data centres, 5G networks, cybersecurity, and artificial intelligence. Additionally, the government seeks to establish Malaysia as a premier destination for digital nomads in the region while accelerating digital adoption (International Trade Administration, 2024). This particularly leads to the growth of fintech uses and awareness. Malaysia’s fintech industry has grown rapidly, advancing through different stages over the years (Adnan et al., 2024). A 2023 survey revealed that 71% of Malaysians were familiar with Fintech, highlighting the country’s growing potential as a market for digital financial services in Southeast Asia. The same year, Malaysia’s fintech sector was projected to generate approximately 365 million USD in revenue from digital investments and assets (Siddharta, 2024).

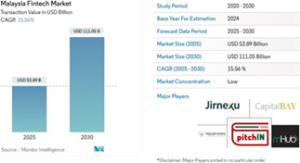

Figure 1: Growth in E-payment transactions in Malaysia

Source: Mordor Intelligence, 2024

As referred to Figure 1, Mordor Intelligence (2024) stated that the transaction value of Malaysia’s fintech market is projected to increase from USD 53.89 billion in 2025 to USD 111.05 billion by 2030, reflecting a compound annual growth rate (CAGR) of 15.56% over the forecast period. Malaysia’s fintech market is highly competitive and fragmented, as the country stands as one of the leading fintech hubs in Asia. Key industry players driving innovation and shaping the market’s growth include Jirnexu, MyCash Online, Capital Bay, PitchIN, and MHub.

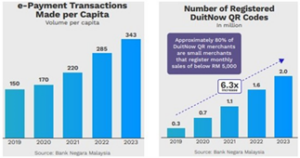

Figure 2: Growth in E-payment transactions in Malaysia

Source: Malaysia Fintech Report 2024

Furthermore, according to Malaysia Fintech Report 2024, E-payment transactions in Malaysia have seen significant growth, driven by the widespread adoption of DuitNow QR codes, which offer seamless and cashless payment solutions across various sectors. Figure 2 shows that the adoption of e-payments in Malaysia continued to rise, with transactions increasing from 9.3 billion in 2022 to 11.5 billion in 2023. According to Bank Negara Malaysia, the country remains on track to meet the 15% CAGR target for e-payment transactions outlined in the Financial Sector Blueprint. In 2023, e-payment usage grew by 20%, reaching 343 transactions per capita. As for DuitNow QR registrations, it have surged to twice the number of point-of-sale (POS) terminals in just four years, reaching 2 million compared to 875,504 POS terminals. Additionally, DuitNow QR transactions have more than doubled year-on-year, totalling 360 million transactions with a transaction value of RM14.6 billion (Fintech News Malaysia, 2024).

Fintech is an emerging industry that integrates finance and technology and has transformed how individuals and businesses conduct conventional financial transactions. Over the past few years, Malaysia has seen a positive trend in the number of Fintech users. According to a finding, over 75% of businesses in Malaysia have adopted technology in conducting business activities including those involving financial transactions (Certified Public Accountant Australia [CPA], 2020). However, like any other technology, Fintech is not free from challenges and limitations, making it harder for Malaysians to adopt it fully.

Using online networks as its primary medium, Fintech will likely be exposed to potential attacks that could lead to security breaches. Furthermore, for the users to use this technology, they must provide personal information to the service provider, putting them at risk of losing their data to cybercrimes. According to MyCERT (2024), data breach incidents in Malaysia are on the rise, increasing by nearly 44% from 117 reported cases in Q2 2024 to 168 cases in Q3 2024. This highlights the urgent need for enhanced security measures to safeguard national security and maintain public trust. Additionally, The Cyber999 Incident Response Centre received 1,623 cyber threat incidents in Q3 2024, compared to 1,481 incidents in Q2 2024. This indicates a 10% increase in incidents in Q3 2024.

The challenge faced by the Fintech industry is the lack of exposure and knowledge of Fintech systems among Malaysians. In the digital age, users expect seamless and secure experiences. Poor digital literacy can lead to frustration with digital financial tools, increasing the likelihood of users abandoning these services due to difficulties navigating or securing their accounts (Vasavi, 2025). Nalluri and Chen (2024) identified the absence of government regulations and concerns over safety and reliability as key barriers to fintech adoption. Moreover, it is important to note that the increase in digitalization could lead to financial exclusion for the less tech-savvy, which includes migrant workers, lower-income groups, and old citizens.

The Fintech Malaysia Report 2023 highlights a rise in the number of fintech companies in Malaysia, increasing from 291 to 313 in 2023. This expansion reflects the country’s notable advancements in the fintech industry, positioning it ahead of many other nations (Lee Yong Ming, 2024). Despite significant growth in total fintech investment, Malaysia still lags behind its neighbouring counterparts, Indonesia and Singapore. While Malaysia remains a key player in ASEAN’s fintech landscape with at least 549 fintech companies, it ranks third in the region, following Indonesia with 785 firms and Singapore with 1,600 (Santosdiaz, 2024). The quality of customer experience among Fintech users in Malaysia may also contribute to lower user retention rates in the Fintech industry. Banks should ensure that the customer user interface toward the online banking application is user-friendly and understandable (Al-Emadi et al., 2021). A complex and hard-to-understand Fintech platform could overwhelm the users, eventually leading to reluctance to continue using the services. Studies show that the functionality of online banking services, including usability, performance, and content, plays a crucial role in shaping customer satisfaction. A user-friendly and accessible interface significantly improves the overall user experience (Othman et al., 2023).

Given the increasing competition among fintech providers, understanding the key determinants of user retention and experience is critical for sustaining user engagement and fostering long-term adoption (Lee & Shin, 2018). Therefore, this concept paper explores the factors influencing user retention and experience in Malaysian Fintech, providing insights for industry stakeholders and policymakers to enhance fintech adoption and customer satisfaction.

Despite the huge number of research and studies exploring user retention and user experience in the fintech industry, there is a clear knowledge gap regarding the specific factors influencing user retention and user experience in developing countries like Malaysia. For example, the existing studies by Appiah and Agblewornu (2025) investigate the influence across four countries in Sub-Saharan Africa. Ryu (2018) discusses the effects of perceived benefits and risks on Fintech continuance intention among different types of users in South Korea. These studies were conducted in a specific setting and did not consider other factors which might not apply to other countries like Malaysia. Thus, this concept paper will focus on how factors like personalization, efficiency and seamless transaction, and security can influence user experience and retention in Fintech, specifically among Malaysians.

Furthermore, existing studies primarily focus on adoption factors rather than user retention and overall user experience. While factors such as trust, security, perceived risk and perceived benefits [Gupta et al., 2023 & Ali et al., 2021] have been explored in fintech adoption, limited research investigates how these factors influence long-term user engagement and satisfaction. Additionally, most studies emphasize technological and regulatory aspects [(Singh et al., 2020 & Bani Atta, 2024), overlooking behavioural and psychological determinants that impact user retention. This concept paper aims to bridge this gap by examining the key factors shaping user retention and experience in Malaysian Fintech, providing insights for industry stakeholders to enhance customer loyalty and satisfaction.

Factors Influencing User Retention and User Experience in Malaysian Fintech

Fintech, leveraging advancements in information and communication technology, is dynamic and innovative. The concept of customer experience is multifaceted and varies across industries, including Fintech. As Fintech evolves into an essential technology for user retention and user experience in financial services, companies can enhance their management practices to become more user-friendly and accessible. Fintech ultimately delivers a more engaging and satisfying user experience, resulting in higher levels of customer retention and loyalty.

Customer retention pertains to the capacity of a company or product to maintain its customer continuous usage throughout a specified duration. Continuous usage intention can be defined as the intention of a user to continue utilizing a particular product or service without interruption, as described by Hong et al. (2013). Previous research on customer retention in the fintech industry has primarily concentrated on external factors that impact customers’ ongoing usage of fintech services. However, it is crucial to shift the focus to the user’s perspective and highlight the influence of customer experience on their retention in Fintech services and the factors that affect their experience in this context.

Jain et al. (2017) explain that customer experience involves cognitive and emotional elements, resulting in unique memories shaped by customer expectations and contextual factors. Numerous studies have demonstrated a strong correlation between customer experience and customer retention in Fintech services. A positive customer experience strengthens the customer’s loyalty intention (Barbu et al., 2021). Alwi et al. (2019) conducted a survey involving 300 Malaysian Fintech users and discovered that security and privacy is the most significant factor influencing customer satisfaction with Fintech mobile payment services. This was followed by service quality, information presentation, and seamless transactions. When customers have positive experiences and develop a solid relationship with a fintech provider, they feel valued and are more likely to continue using their services. Thus, it is crucial to investigate the main potential factors that influence the user experience and retention in Malaysian Fintech, which are as follows: (1) Personalization, (2) Security and (3) Efficiency and Seamless transactions.

Personalization

According to Kargin et al. (2009), personalization emerges as the crucial factor influencing customer experience and retention in the Fintech sector. Personalization can be defined as the ability to offer customized content and services based on an individual’s preferences and behaviours (Adomavicius & Tuzhilin, 2005). Technologically, personalization involves modifying a system’s functionality, interface, information access, and content to enhance its relevance to an individual or a specific group of individuals, as Fan and Poole (2006) highlighted. Vasuki et al.’s (2025) description of a system analyzing real-time interactions suggests that adapting to user behaviour at the moment is valuable for optimizing user experience.

Personalization can influence users’ attitudes and intentions to use mobile services. Kargin et al. (2009) suggest that personalization indirectly determines a user’s attitude toward utilizing mobile services. Furthermore, Sheng et al. (2008) conducted a study exploring the impact of personalization and context on users’ intentions to adopt mobile services, concluding that personalization positively affects users’ intentions to adopt such services.Personalization plays a significant role in the financial technology sector since it enables the delivery of individualized content and services based on users’ characteristics and actions (Adomavicius & Tuzhilin, 2005). Personalization, in the context of information technology, is the process of tailoring a system’s features, interface, information access, and content to an individual user or group of users (Fan & Poole, 2006). Damrongsak (2024) and Gada (2024) found that the ability of users to customize their interfaces is a key factor in improving satisfaction and retention. They report that interfaces offering customizable features and personalized recommendations yield a 30% increase in retention rates.

Multiple studies have demonstrated the importance of customization in retaining Fintech clients. Personalized financial guidance and tailored marketing strategies enhance customer engagement and retention (Benjamin et al., 2024). Personalized interactions build trust and familiarity, increasing customer loyalty and retention rates. Users feel valued when their specific needs are addressed (BuzzBoard, 2024). Similarly, a study by Wang et al. (2020) discovered that clients who received individualized investing advice were more likely to trust and employ fintech services. Personalization involves using data to offer relevant services, recommendations, and rewards that align with customer interests. This approach makes customers feel valued and increases their engagement with the service (Wadhwa, 2023). They can also employ technologies like Artificial Intelligence and Machine Learning to provide clients with recommendations that are more tailored to their specific circumstances (Wang et al., 2020). Myagkova’s (2024) study suggests that AI can significantly enhance the personalization experience, leading to improved satisfaction and engagement. In addition, Li et al. (2023) introduce the concept of psychological ownership, suggesting that personalization strategies should consider psychological factors to enhance user experience and retention.

Fintech firms may create a more customized and relevant environment for their users if they provide personalized experiences for their consumers. This increases the possibility that their customers will continue to use the company’s products. According to Kargin et al. (2009), personalization shapes a user’s perspective on mobile services. Personalization allows mobile banking apps to offer relevant services and products, increasing user engagement and satisfaction (Ansari, 2024). Therefore, personalization is a driving force in the fintech sector, allowing businesses to offer individualized products and services to their clientele based on their specific needs and interests.

Security

Data security emerges as a paramount factor in customer retention. It is a multifaceted concept focused on protecting information from unauthorized access, modification, or destruction throughout its lifecycle (Deepa & Dhiipan, 2022). It encompasses various aspects of an organization’s IT infrastructure, including hardware, software, personnel, and policies (Gordon, 2019). This includes safeguarding against cyber threats such as data breaches, financial fraud, and other cyber-attacks that could compromise the safety and trustworthiness of fintech platforms (Rikkeisoft, 2022). Robust security features like encryption and secure authentication protocols foster trust among users, making them more likely to continue using fintech services (Chan et al., 2024). Studies show that individuals are particularly wary of sharing financial data and secure identifiers (Milne et al., 2017). Consumers seek assurance regarding the security of their Fintech operations, particularly online financial transactions (Barbu et al., 2021). Therefore, security measures can provide the necessary assurance that fosters relevant consumer experience, particularly in terms of the affective component.

Security is essential in the Fintech industry since it guarantees the confidentiality of users’ financial transactions and other information. Zhang et al. (2023) found that trust is positively influenced by data security, indicating that it is important for Fintech innovators to understand their customers’ attitude regarding transparency of data and its security. Such operational activities help customers understand the proper use of their data and ensure its secure storage. Secure platforms that are easy to use enhance the perceived benefits of fintech services, contributing to user retention by providing a seamless experience (Abdullah & Hisamudin, 2024). Customers who have confidence in their financial transactions and personal data safety are more inclined to stick with Fintech providers. Fintech platforms can reduce user anxiety about data breaches and fraud by addressing security concerns, leading to higher user retention rates (Chan et al., 2024).

Several studies have demonstrated that security breaches in the Fintech business may devastate the company’s ability to retain its customers. The rise in cyberattacks and weaknesses in information security systems undermine consumer trust and perceived safety, causing widespread reluctance to adopt Fintech services (Matos et al., 2020). Similarly, another study by Wang et al. (2020) discovered that customers’ inclination to utilize Fintech services is greatly reduced due to perceived security issues. Therefore, it is crucial to provide user-friendly protections which make fintech platforms easier to navigate, increasing users’ confidence and trust in these services (Chan et al., 2024).

In addition, they may use blockchain technology to make financial dealings more trustworthy and open (Wang et al., 2020). Innovative security technologies, such as advanced encryption and blockchain, can enhance user engagement by offering a secure and modern experience (Rikkeisoft, 2022). Fintech businesses may make their clients feel safer about making online financial and personal data transactions by using advanced security measures like multi-factor authentication, biometric authentication, and encryption technology. Strong security measures keep fintech services running smoothly, preventing disruptions and ensuring users have constant access to their financial resources, while reliable security systems protect financial data, guaranteeing accurate and secure transactions. (SGS, 2024). This demonstrates the importance of security factors in the Fintech sector, as they guarantee the privacy and integrity of consumers’ financial and personal data because safety has been demonstrated to impact repeat business substantially.

Efficiency and Seamless transactions

Gomber et al. (2018) have also identified efficiency and seamless transactions as critical factors influencing customer experience and retention in the Fintech industry. These factors can be understood as Perceived Usefulness (PU) (efficiency) and Perceived Ease of Use (PEU) (Seamless transaction) when utilizing fintech services. Usefulness pertains to the belief that using a system will enhance job performance. It includes factors such as the ease of downloading and installing applications, minimal downtime, and accessible support systems (Hurani & Abdel-Haq, 2025) while ease of use, as outlined by Davis (1989), refers to the perception of a system as effortless and easy to comprehend (Rahim et al., 2021).

Wicaksono & Maharani (2020) define indicators of PU as including making transactions easy, practical, saving time, meeting needs and increasing efficiency, while PEU indicates easy to understand, simple and easy to use, avoid distraction and easy to access, which represents Seamless transactions. PU and PEoU consistently emerge as significant positive predictors of intention to use and actual adoption across mobile banking and e-wallet platforms (Rehman & Shaikh, 2020). Similarly, PU and PEU significantly affect customers’ intention to use online applications (Wicaksono & Maharani, 2020).

Since a Fintech company’s success depends on its services’ usefulness and ease, efficiency and seamless transactions are critical factors in the Fintech business. Fintech efficiency encompasses various aspects, ranging from optimized backend operations to smooth user interactions (Nestorovic, 2023). Davis (1989) defines “ease of use” as “the degree to which a person believes that use of a particular system would be free from effort”. This means that customers will remain loyal to a fintech service as long as it meets their needs and is easy to use.

Several studies have demonstrated that efficiency and seamless transactions substantially impact client retention in the fintech business. Amnas et al. (2023) suggest trust and perceived usefulness emerge as critical determinants of fintech adoption. When users find fintech services beneficial, their satisfaction with these services increases. The advantages of Fintech include enhanced efficiency, time savings, cost reductions, improved user experience, and fostered long-term engagement (Alshathry & Almeshal, 2022). Another study by Sheng et al. (2008) concluded that customization and context significantly impacted consumers’ propensity to embrace mobile services. Gomber et al. (2018) further suggest that ease of use increases the motivation to adopt fintech services, especially among consumers with low technological readiness. Similarly, the research by Souiden and Rani (2015) highlights that less tech-savvy consumers can be motivated to adopt Fintech due to the ease-of-use factor and their favourable experiences with Fintech, ultimately leading to increased loyalty among these consumers. Easy-to-use fintech applications increase user adoption rates by making it more straightforward for new users to start using the services (Tahar et al., 2020). In the context of e-money applications like Go-Pay, PU and PEU positively impact user attitudes, with PEU having a more substantial effect on actual usage through attitude than directly (Gusni et al., 2020).

Fintech businesses may deliver individualized services to boost client retention via streamlined operations and satisfied consumers (Sheng et al., 2008). In the financial sector, AI and Machine Learning are being employed to analyze vast amounts of transaction data, detect fraudulent activities, identify potential attacks, and uncover valuable insights that human intelligence alone cannot achieve (Parne,2021). Fintech organizations may make their services more user-friendly by employing machine learning and artificial intelligence technology to streamline and expedite financial operations. Fintech in Malaysia relies heavily on efficiency and flawless transactions to provide more rapid and convenient online money transfers. Understanding these factors is crucial for fintech providers to improve user retention and mitigate risks associated with fintech adoption (Hutapea & Andista, 2021). This proves that if Malaysia wants to guarantee the practicality and convenience of Fintech services, efficiency and frictionless transactions are essential.

This study employs a simple Systematic Literature Review (SLR) approach to evaluate user experience and retention within Malaysia’s fintech sector. The SLR method systematically compiles and synthesizes existing research on the topic, providing valuable insights for primary studies, serving as an independent academic contribution, and offering a comprehensive perspective on the subject (Kabir et al., 2023). The study relies on secondary data sources, including peer-reviewed journals, industry reports, regulatory frameworks, and case studies from both Malaysian and global contexts. The methodology consists of the following key components:

Literature Review: An analysis of existing studies to identify key factors influencing user experience and retention in Fintech. The review emphasizes three primary aspects: (1) Personalization, (2) Security, and (3) Efficiency and Seamless transactions. This involves an in-depth examination of academic literature and industry insights. The selection of literature follows a structured process to ensure relevance, quality, and credibility. The following inclusion and exclusion criteria guide the selection process:

Inclusion Criteria:

Exclusion Criteria:

The search process involves using academic databases such as Scopus, Web of Science and Google Scholar. Keywords such as “Fintech user experience,” “Fintech retention,” “Malaysia Fintech adoption,” and “Personalization, Security and Efficiency in Fintech” guide the literature search.

Research Design: Developing a conceptual framework that maps and identifies the critical determinants shaping user experience and retention in Malaysia’s fintech industry.

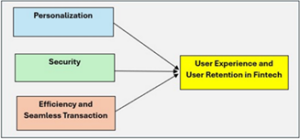

Figure 3: The Proposed Conceptual Framework for Factors Influencing the User Experience and User Retention of Fintech in Malaysia.

Figure 3 illustrates the key factors influencing Malaysia’s fintech user experience and retention. The conceptual framework for this study is grounded in prior research, which establishes the relationship between various determinants and user satisfaction. This framework identifies personalization, security, efficiency, and seamless transactions as critical variables that enhance user experience and foster long-term retention in the fintech sector.

By integrating these factors, the conceptual framework provides a structured approach to understanding how FinTech firms in Malaysia can optimize user experience and improve retention. This model serves as a foundation for further empirical research and strategic decision-making within the industry.

This study identifies three primary factors influencing user retention and user experience in Malaysia’s fintech sector: Personalization, security, efficiency and seamless transactions. These findings highlight the significance of tailored services, robust security frameworks, and operational efficiency in enhancing customer satisfaction and long-term engagement with FinTech platforms.

Personalization and Its Impact on User Retention

Personalization emerges as a key driver of user engagement and satisfaction, ultimately leading to higher retention rates in fintech services. The ability to offer customized experiences—such as tailored financial recommendations, personalized dashboards, and adaptive user interfaces—enhances customer trust and perceived value (Adomavicius & Tuzhilin, 2005; Fan & Poole, 2006). Studies indicate that personalized interfaces and recommendations increase retention by up to 30% (Damrongsak, 2024; Gada, 2024).

Furthermore, Artificial Intelligence (AI) and Machine Learning (ML) play a pivotal role in refining personalization by analyzing real-time user interactions (Vasuki et al., 2025; Myagkova, 2024). Personalized financial guidance, targeted marketing strategies, and AI-driven recommendations foster a sense of psychological ownership, making users more likely to remain loyal to fintech platforms (Wang et al., 2020; Li et al., 2023).

The literature also underscores the role of personalization in mobile banking, where individualized services significantly enhance customer satisfaction and long-term usage (Kargin et al., 2009; Ansari, 2024). This suggests that fintech providers who leverage customization strategies are more likely to achieve higher user retention rates.

Security as a Foundational Factor in Fintech Adoption

Security remains a fundamental determinant of user trust and fintech adoption. The increasing frequency of cyberattacks and financial fraud has made security concerns a significant barrier to fintech acceptance (Rikkeisoft, 2022). Consumers demand robust security protocols, including encryption, multi-factor authentication, and fraud detection systems, to protect their financial data (Chan et al., 2024; Abdullah & Hisamudin, 2024).

Studies show that perceived security directly influences user retention, as customers are more likely to disengage from platforms, they deem vulnerable to data breaches (Matos et al., 2020; Wang et al., 2020). Fintech providers that implement advanced security measures, such as blockchain technology, biometric authentication, and AI-driven fraud detection, can enhance user confidence and sustain long-term engagement (Zhang et al., 2023; SGS, 2024).

Furthermore, secure platforms prioritizing user-friendly security measures (such as seamless authentication without excessive complexity) improve user experience, reducing transaction friction while ensuring data protection (Barbu et al., 2021). Addressing security concerns mitigates risks and enhances the perceived reliability of fintech services, reinforcing customer loyalty (Chan et al., 2024).

Efficiency and Seamless Transactions as Drivers of Fintech Loyalty

Efficiency and seamless transactions significantly contribute to fintech adoption and sustained usage. The ease of accessing services, processing transactions, and navigating financial applications influences customer satisfaction and loyalty (Gomber et al., 2018). Studies suggest that Perceived Usefulness (PU) and Perceived Ease of Use (PEU) are strong predictors of fintech adoption, where users prefer platforms that are intuitive, fast, and hassle-free (Davis, 1989; Wicaksono & Maharani, 2020).

Efficient fintech platforms minimize transaction delays, service downtimes, and system errors, providing users with a smooth and reliable experience (Hurani & Abdel-Haq, 2025). Research shows that fintech firms leveraging AI and automation to optimize backend processes enhance operational efficiency, strengthening user retention (Parne, 2021; Nestorovic, 2023).

Moreover, fintech solutions that offer fast and frictionless payment experiences, such as one-click transactions and real-time fund transfers, appeal to users with lower technological readiness, widening fintech adoption across different demographic segments (Souiden & Rani, 2015; Tahar et al., 2020). Given these insights, fintech providers must prioritize seamless service delivery by incorporating AI-driven automation, intuitive interfaces, and enhanced transaction speeds to maintain high levels of user engagement and retention (Alshathry & Almeshal, 2022; Hutapea & Andista, 2021).

Therefore, by addressing these three factors, fintech providers can enhance customer satisfaction, build long-term trust, and drive sustainable user retention in Malaysia’s competitive financial technology landscape.

The development of Fintech has created diverse possibilities for the financial sector. Fintech, or financial technology, has transformed the way businesses work in the modern world. It provides a variety of solutions that can greatly help the growth of organizations. This study explores the key factors influencing user retention and experience in the Malaysian Fintech sector, highlighting personalization, security, efficiency and seamless transactions as critical determinants. The findings suggest that personalized services enhance user engagement by catering to individual preferences, while robust security measures and operational efficiency build trust and reliability. Additionally, seamless transactions contribute to a frictionless experience, fostering long-term user satisfaction and retention.

Personalization encompasses features such as personalized suggestions, targeted offers, and personalized financial information. Fintech firms that prioritize speed, simplicity, and seamless user interfaces enable consumers to conduct financial transactions quickly and comfortably. Fintech deals with highly sensitive financial data, including users’ personal and financial details. When users have faith in the platform’s security, it encourages trust and reassurance. Furthermore, this research aims to provide organizations with the information and resources they need to successfully utilize technology and fulfil customers’ growing expectations, resulting in enhanced user satisfaction, loyalty, and retention.

Competition in the developing Fintech business is prominent in this rapidly growing globe. Organizations that provide better user experience than their rivals may attract and keep more customers, resulting in business growth and market success. Increased engagement helps users while also contributing to revenue development for Fintech firms. In another way, fintech businesses that demonstrate a dedication to user-centricity and compliance may traverse regulatory barriers more successfully, guaranteeing sustainable development and minimizing regulatory risks. However, this study influences other parties in Malaysia, such as the government and society. Governments may use this information to develop or modify current legislation that protects consumer interests, prevents fraud or misbehavior, and guarantees equitable treatment of fintech users. To enhance user confidence and trust in fintech services, initiatives such as data protection laws, transparent practices, and effective dispute resolution mechanisms can be introduced. Moreover, the expansion of the fintech sector has the potential to contribute to economic development and job creation. As the industry grows, new job possibilities emerge in technological development, customer service, data analysis and regulatory compliance. This can lead to wider economic growth and help reduce unemployment.

This study highlights the significant impact of personalization, security, efficiency and seamless transactions on the user experience and user retention of Fintech services in Malaysia. The findings provide valuable insights for improving the effectiveness of Fintech strategies and facilitating global economies of scale for Fintech businesses. Furthermore, the study suggests that Malaysia Digital Economy Corporation (MDEC) could leverage these insights to promote fintech adoption in Malaysia. One recommendation for sectors utilizing Fintech, particularly in the financial industry, is to offer 24/7 customer support via email to ensure prompt and effective consumer assistance. Emphasizing relevant and meaningful financial advice and ensuring a seamless and convenient customer journey are essential aspects of this service.

The study also emphasizes the importance of securing user data by integrating multi-factor authentication, biometric authentication, and encryption technologies. Adhering to key data protection regulations like Malaysia’s Personal Data Protection Act (PDPA) is crucial for the continued development of Fintech in Malaysia. Implementing multi-factor authentication (MFA) can provide additional protection against unauthorized access. Fintech companies should actively engage with regulatory agencies such as Bank Negara Malaysia to stay updated on regulatory standards and explore ways to expedite compliance processes. Seeking advice on streamlining transaction procedures and reducing paperwork within the regulatory framework is recommended. Collaborating with relevant government authorities and financial organizations can also enable seamless data retrieval. Ultimately, delivering high-quality customer service will help foster customer trust and loyalty, nurture strong customer relationships, and enhance overall customer satisfaction.

The authors would like to convey their appreciation to the Faculty of Accountancy, Universiti Teknologi MARA, Malaysia, for supporting and enabling this research project.